Scale Your Rental Portfolio with DSCR Loans

Scaling a rental portfolio often feels like a race against your own tax returns. For many investors in states like Florida, California, and Illinois, the traditional mortgage process becomes a bottleneck once you own more than a few properties. Traditional lenders focus on your personal Debt-to-Income (DTI) ratio, which can quickly become lopsided as you add more mortgages to your credit report.

DSCR Investor Loans offer a different path. These loans focus on the cash flow of the property rather than your personal salary or employment history. This shift in perspective allows real estate investors to scale their portfolios based on the strength of their assets, not the limitations of their day jobs.

Understanding the DSCR Framework

To scale effectively, you must first understand the primary metric lenders use to evaluate these deals. The Debt Service Coverage Ratio (DSCR) is a simple but powerful calculation that measures a property's ability to pay for itself.

Debt Service Coverage Ratio (DSCR): A financial metric used by lenders to measure the available cash flow of a property to cover its monthly debt obligations. Practical Application: This ratio tells a lender if the rental income from a property is enough to pay the mortgage, taxes, insurance, and HOA fees.

Net Operating Income (NOI): The total income generated by a property after all operating expenses have been deducted, but before taxes and interest are paid. Practical Application: NOI represents the pure profit potential of a rental unit, which is the foundation of the DSCR calculation.

How to Calculate Your Scaling Potential

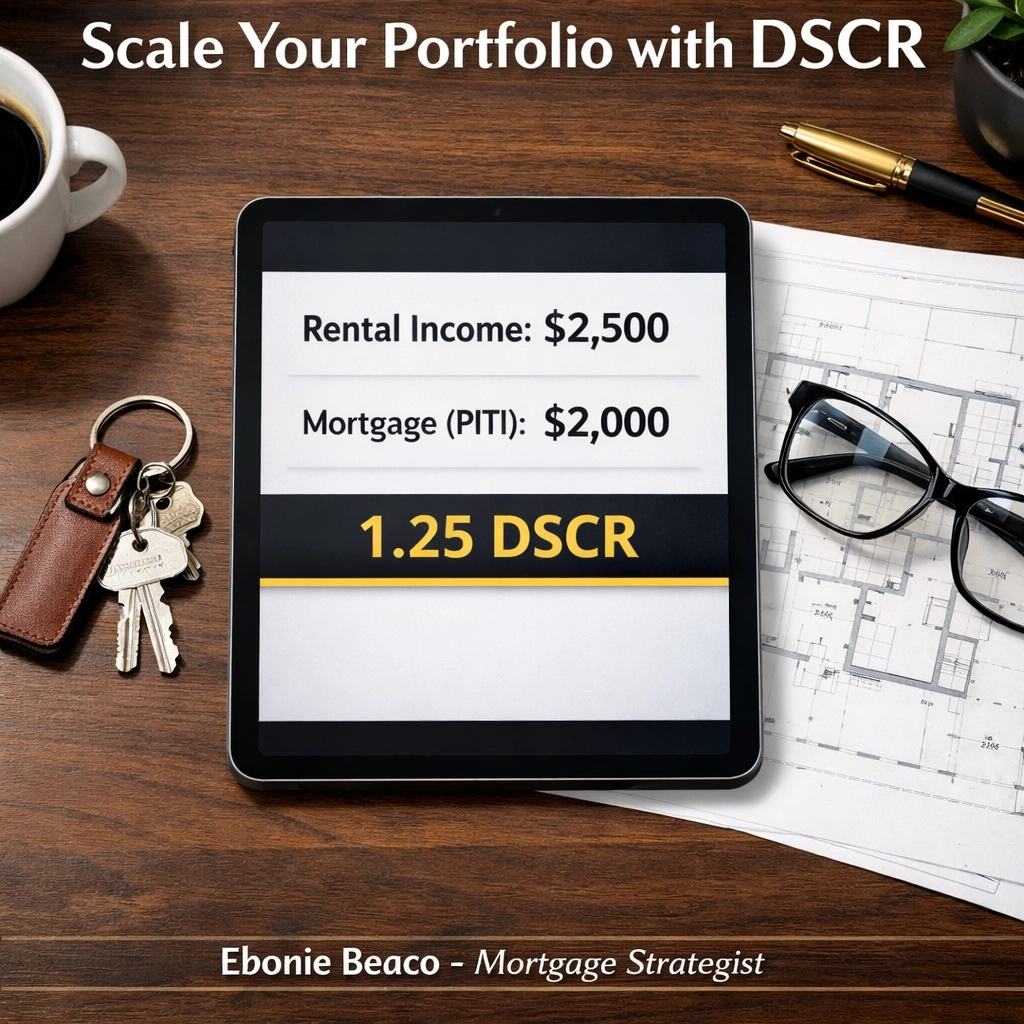

Lenders typically look for a DSCR of 1.0 or higher. A 1.0 ratio means the property "breaks even," where the rent exactly covers the debt. Most aggressive scaling strategies target a ratio of 1.2 or 1.25 to ensure there is a cushion for maintenance and vacancies.

Visual breakdown: Rental Income: $2,500 | Mortgage (PITI): $2,000 | Calculation: $2,500 / $2,000 = 1.25 DSCR. Title: Scale Your Portfolio with DSCR | Ebonie Beaco - Mortgage Loan Officer

Visual breakdown: Rental Income: $2,500 | Mortgage (PITI): $2,000 | Calculation: $2,500 / $2,000 = 1.25 DSCR. Title: Scale Your Portfolio with DSCR | Ebonie Beaco - Mortgage Loan Officer

When you maintain a healthy ratio across your portfolio, you demonstrate to lenders that your business model is sustainable. You can explore how these numbers impact your specific goals by using our mortgage calculators.

The Velocity of Money: Scaling Through Refinancing

One of the most effective ways to grow a portfolio in markets like Chicago or various cities in Georgia is through the Cash-Out Refinance strategy. This is often referred to as the "BRRRR" method (Buy, Rehab, Rent, Refinance, Repeat).

- Acquire: Purchase a distressed or undervalued property using a Bridge Loan or Hard Money Loan.

- Renovate: Improve the property to increase its market value and potential rental income.

- Rent: Secure a tenant to establish the property's cash flow.

- Refinance: Use a DSCR Loan to pay off the short-term debt and pull out your initial capital.

- Repeat: Take the "cashed-out" equity and use it as a down payment for your next acquisition.

By using DSCR Investor Loans for the final refinance step, you avoid the DTI hurdles that often stop investors from completing the cycle. You can learn more about this transition in our loan process guide.

Removing the 10-Property Cap

Traditional Fannie Mae and Freddie Mac guidelines often limit individual investors to 10 financed properties. For someone looking to build a massive footprint in Alabama, Arkansas, or Michigan, this cap is a major hurdle.

DSCR Loans do not typically have these same limitations. Because the loan is underwritten based on the property’s performance, many lenders allow you to own an unlimited number of financed properties. This is a game-changer for investors who have hit the "conventional wall" and want to continue expanding into multifamily units or short-term rentals.

Scaling with Short-Term Rentals (Airbnb and VRBO)

The rise of the short-term rental market in vacation hubs throughout Florida and California has created new opportunities for scaling. Airbnb and Short-Term Rental Financing through DSCR programs often allows you to use projected "AirDNA" data or historical short-term rental income to qualify.

Short-Term Rental (STR) Income: Revenue generated from properties rented on a nightly or weekly basis rather than through 12-month leases. Practical Application: Using STR income for a DSCR loan can often result in a higher ratio because short-term nightly rates typically exceed monthly long-term rents.

Why DSCR is the Preferred Tool for Portfolio Growth

- No Employment Verification: You do not need to provide W2s or pay stubs, making this ideal for self-employed investors or those who have recently transitioned into full-time real estate.

- Fast Closing Times: Without the need for extensive personal financial audits, the home purchase process can move much faster.

- Entity Lending: You can close the loan in the name of an LLC, which provides asset protection and allows for easier partnership structures.

- Focus on Credit Score: While personal income isn't the focus, your credit score still plays a role in determining your interest rate and required down payment.

Market Strategies: Where to Scale

Investors currently look at different regions for different goals. In the Midwest, including cities like Chicago or markets in Missouri and Kentucky, the focus is often on high-yield cash flow where properties easily meet high DSCR requirements.

In higher-priced markets like California or Virginia, the strategy might lean toward long-term appreciation. In these cases, even a DSCR of 1.0 is acceptable because the investor is betting on the property value increasing significantly over time.

Visual comparison: High Cash Flow Market (1.5 DSCR) vs. High Appreciation Market (1.0 DSCR). Title: Scale Your Portfolio with DSCR | Ebonie Beaco - Mortgage Loan Officer

Visual comparison: High Cash Flow Market (1.5 DSCR) vs. High Appreciation Market (1.0 DSCR). Title: Scale Your Portfolio with DSCR | Ebonie Beaco - Mortgage Loan Officer

Common Pitfalls to Avoid When Scaling

Scaling quickly requires discipline. A common mistake is over-leveraging. Just because a lender will allow a 1.0 DSCR doesn't mean you should settle for it on every property. Maintaining a "cushion" ensures that if one property has an extended vacancy, the rest of your portfolio can carry the weight.

Another hurdle is the "Prepayment Penalty." Many DSCR Investor Loans come with a penalty if you refinance or sell within the first 3 to 5 years. If your goal is to flip the property quickly, a Bridge Loan might be a better fit. If you plan to hold long-term, the DSCR loan is usually the superior choice. You can find answers to more specific questions in our FAQ section.

Taking the Next Step in Your Investment Journey

Building a rental empire is about strategy and access to capital. If you feel stuck at your current number of doors, it might be time to move away from traditional financing and embrace the flexibility of asset-based lending.

Whether you are looking to purchase your first duplex in Indiana or your tenth apartment building in Florida, understanding how to leverage the property’s own income is the key to unlimited growth.

Jump in and evaluate your current portfolio to see where equity might be hiding. Explore the various programs available for Non-QM Mortgage Loans and Landlord Loans.

For a personalized strategy session on how to scale your specific portfolio or for professional mentoring in the real estate space, reach out to an expert who understands the nuances of investor financing.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Contact Ebonie Beaco for portfolio scaling strategies or mentoring at www.homeloansnetwork.com.