Refinance Rates Peak at 3-Month Highs

It has been a whirlwind week in the mortgage industry. If you have been watching the ticker or checking your notifications, you probably noticed the shift. Refinance rates have officially hit their highest point in three months.

I am Ebonie Beaco, your Mortgage Strategist, and I want to walk you through exactly what is happening in the market right now. From geopolitical shifts affecting bond yields to how investors in Chicago, Florida, and Virginia are pivoting their strategies, we have a lot to cover.

Here are the seven most critical updates from the last 48 hours and today.

1. Wednesday, March 18, 2026: 30-Year Refinance Rates Hit a 3-Month Peak

The average 30-year fixed refinance rate has climbed to 6.44% today. This follows a steady upward crawl from earlier in the month when we saw rates hovering closer to 6.2%. For homeowners in states like Michigan and Indiana who were waiting for a dip to tap into their equity, this surge represents a significant change in the monthly payment landscape.

According to recent reports, the 15-year refinance rate has also moved up to 5.47%. While these rates are still more attractive than the highs we saw a few years ago, the sudden jump has many homeowners hitting the pause button on traditional rate-and-term refinances.

2. Tuesday, March 17, 2026: Geopolitical Tensions Drive Bond Yields Upward

Market volatility is often a reflection of global events. Over the last 24 hours, increased geopolitical tensions have sent investors scurrying for safety, which paradoxically pushed bond yields higher. Since mortgage rates typically follow the 10-year Treasury yield, we saw an immediate reaction in the lending space.

You can find a detailed breakdown of these specific market movements in this reference article: Mortgage Refinance Rates Today. When uncertainty enters the global stage, the domestic mortgage market usually feels the ripple effect within hours.

3. Tuesday, March 17, 2026: Federal Reserve Holds Steady on Interest Rates

The Federal Reserve opted to keep the federal funds rate unchanged during their latest session. While the Fed does not set mortgage rates directly, their stance on inflation and the economy dictates the "vibe" of the lending market.

Because there has not been a rate cut since December, the downward pressure many expected for the spring market has not materialized. This has led to a surge in Non-QM Mortgage Loans: financing options that don't follow traditional government-backed guidelines: as borrowers look for more flexible ways to structure their debt.

4. Monday, March 16, 2026: Inventory Shortages in Florida and Georgia Impact Lending

New data released on Monday shows that housing inventory in major hubs like Atlanta, Miami, and Orlando remains tight. For real estate investors, this means the competition for "fix and flip" properties is high.

With refinance rates peaking, we are seeing more investors shift toward Bridge Loans. A bridge loan is a short-term financing tool used to "bridge" the gap between the purchase of a new property and the sale or permanent financing of another. Investors are using these to secure properties quickly in high-demand markets without waiting for a traditional 30-day refinance window.

5. Monday, March 16, 2026: HELOC Applications Rise in High-Equity Markets

As 30-year refinance rates climb, homeowners in California and Virginia are choosing to keep their low primary mortgage rates and instead use a HELOC (Home Equity Line of Credit).

A HELOC is a revolving line of credit that allows you to borrow against the equity in your home. Instead of replacing your entire mortgage (and losing a 3% or 4% rate), you simply add a second lien. This is becoming the preferred strategy for Chicago homeowners looking to renovate kitchens or consolidate high-interest credit card debt without touching their primary mortgage.

Visual Description: A chart showing a comparison between a full Cash-Out Refinance and a HELOC strategy for a $500,000 home. The image includes the title 'Refinance Rates Peak at 3-Month Highs' and 'Ebonie Beaco - Mortgage Strategist' at the bottom. No currency symbols or money items are shown.

Visual Description: A chart showing a comparison between a full Cash-Out Refinance and a HELOC strategy for a $500,000 home. The image includes the title 'Refinance Rates Peak at 3-Month Highs' and 'Ebonie Beaco - Mortgage Strategist' at the bottom. No currency symbols or money items are shown.

6. Sunday, March 15, 2026: DSCR Loans Gain Popularity Among Landlords

Over the weekend, industry data highlighted a significant uptick in DSCR Investor Loans. DSCR (Debt Service Coverage Ratio): A loan program where qualification is based on the cash flow of the property rather than the borrower’s personal income.

If you are a landlord in Alabama or Arkansas, your personal debt-to-income ratio (DTI) might be high, but if your rental property brings in $2,500 a month and the mortgage payment is $1,800, you have a strong DSCR. Investors are using these loans to scale their portfolios even while rates are higher because the property itself carries the weight of the debt.

7. Sunday, March 15, 2026: Rise of Short-Term Rental Financing in Vacation Hubs

Airbnb and short-term rental investors are increasingly looking at Bank Statement Loans. These are designed for self-employed borrowers who have significant cash flow but may show lower taxable income on their tax returns due to business write-offs.

In coastal cities and vacation spots across Virginia and Florida, these specialized programs are allowing investors to acquire properties that traditional banks might turn down. It is all about looking at the actual bank deposits to prove the ability to repay the loan.

Understanding the Strategy: HELOC vs. Cash-Out Refinance

With rates hitting a 3-month high, I get asked daily: "Should I refinance or get a HELOC?"

Let's look at a real-world scenario. Imagine you own a home in Chicago valued at $500,000. Your current mortgage balance is $280,000 at a 3.25% interest rate. You want to access $100,000 for a new investment property in Florida.

If you do a Cash-Out Refinance, you would take out a new loan for $380,000. At today’s rate of 6.44%, your monthly payment would skyrocket because you are applying that new, higher rate to the entire $380,000.

Instead, many of my clients are choosing a HELOC. You keep your $280,000 loan at 3.25%. You take a separate line of credit for $100,000. You only pay the higher interest rate on the $100,000 you actually use.

This strategy saves thousands in interest over the long run. Explore your options at Home Loans Network Mortgage Basics to see which fits your profile.

Visual Description: A financial breakdown graphic showing the "HELOC Advantage." It compares the interest cost of a $380,000 loan at 6.44% versus a split loan strategy. The image includes the title 'Refinance Rates Peak at 3-Month Highs' and 'Ebonie Beaco - Mortgage Strategist' at the bottom.

Visual Description: A financial breakdown graphic showing the "HELOC Advantage." It compares the interest cost of a $380,000 loan at 6.44% versus a split loan strategy. The image includes the title 'Refinance Rates Peak at 3-Month Highs' and 'Ebonie Beaco - Mortgage Strategist' at the bottom.

The Investor’s Edge: DSCR and Fix & Flip Financing

Real estate investors in markets like Missouri and Kentucky aren't necessarily scared by 6.4% rates. Why? Because they focus on the deal's margins.

Fix and Flip Loans: Short-term financing used to purchase and renovate a property with the intent to sell it quickly for profit. For a flipper, the interest rate is a line item in the budget, not a 30-year commitment. If the "After Repair Value" (ARV) is high enough, a slightly higher rate won't break the deal.

For the buy-and-hold crowd, Landlord Loans via the DSCR method are the gold standard. Compare the traditional bank route (which requires years of tax returns) to a DSCR loan (which requires a signed lease agreement). In a fast-moving market like Georgia, the speed of a DSCR loan can be the difference between winning a bid and losing it.

Jump in and see how these programs work for your specific property at Home Loans Network Investor Loans.

Navigating the Shift

The peak in refinance rates is a reminder that the market is always in motion. Whether you are a homeowner in Illinois or a commercial investor in California, the key is transparency. You need to know the numbers before you make the move.

The recent rise in rates shouldn't stop your progress; it should just change your tactics. If you are looking to acquire a multi-unit apartment building or perhaps a duplex in Michigan, looking into Non-QM Mortgage Loans or Interest-Only options might be the way to keep your cash flow positive while we wait for the next market cycle.

Explore our FAQ for more insights on how these programs differ and how you can qualify.

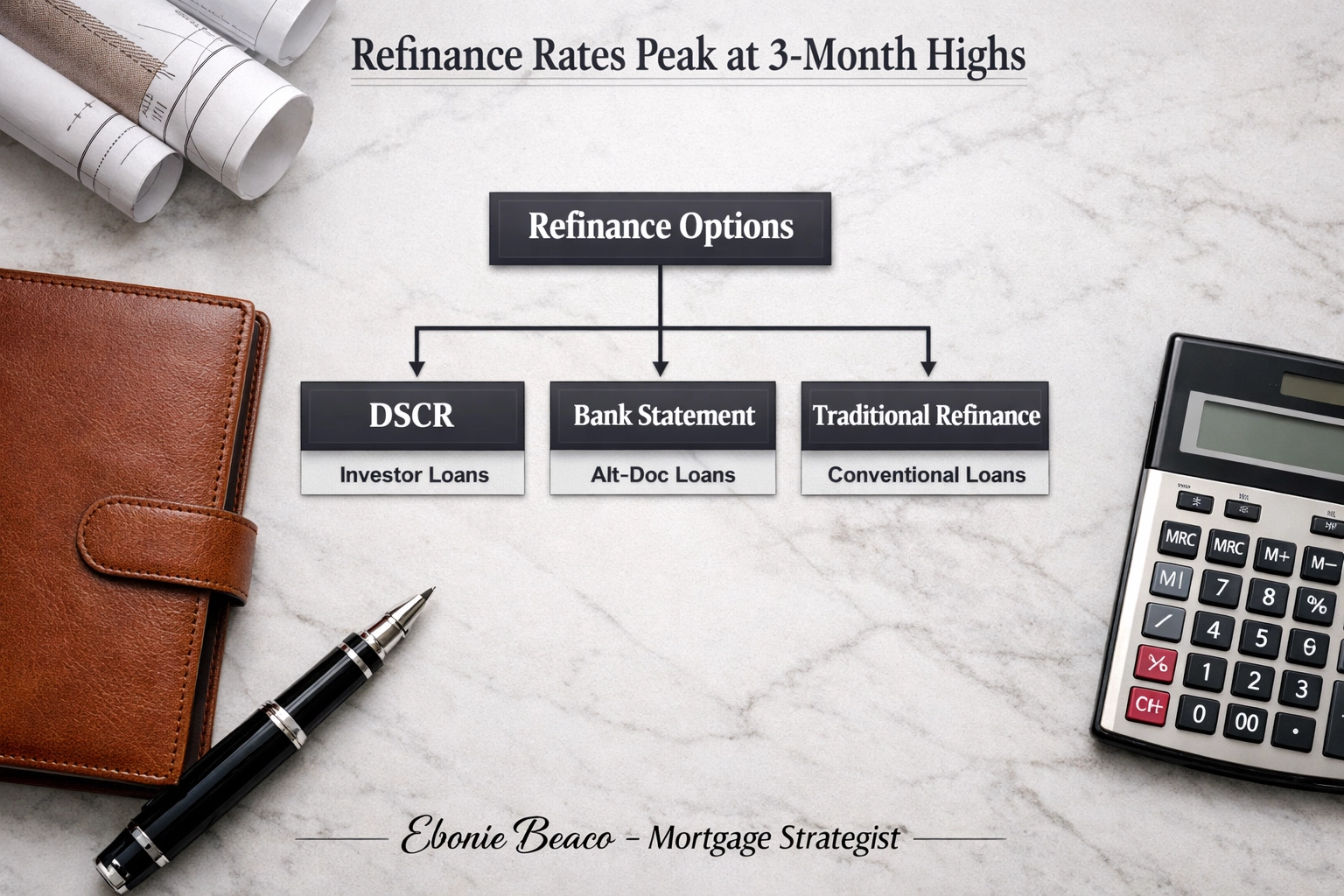

Visual Description: A structured flowchart helping a reader choose between a DSCR loan, a Bank Statement loan, or a traditional Refinance based on their goals. The image includes the title 'Refinance Rates Peak at 3-Month Highs' and 'Ebonie Beaco - Mortgage Strategist' at the bottom.

Visual Description: A structured flowchart helping a reader choose between a DSCR loan, a Bank Statement loan, or a traditional Refinance based on their goals. The image includes the title 'Refinance Rates Peak at 3-Month Highs' and 'Ebonie Beaco - Mortgage Strategist' at the bottom.

Access the guidance you need to make an informed decision.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664