Rate Sheets 101: Understanding Mortgage Pricing Like a Pro

Walking into the world of real estate investing or even just buying your first home in Chicago or Miami can feel like learning a second language. One of the most misunderstood tools in the entire mortgage industry is the rate sheet. If you have ever asked a loan officer, "What is the rate today?" and received a complicated answer that started with "It depends," you were likely hearing the byproduct of a mortgage rate sheet.

At Home Loans Network, we believe in radical transparency. Understanding how these sheets function allows you to move from being a passive borrower to a strategic investor. Whether you are looking at mortgage basics or you are a seasoned landlord in Alabama looking for a DSCR loan, knowing how your price is built is the first step to financial clarity.

What Exactly is a Mortgage Rate Sheet?

A mortgage rate sheet is a daily updated grid that serves as the "menu" for a mortgage lender. It lists various interest rates and the corresponding "price" for those rates across different loan programs.

Think of it like a wholesale catalog. The prices on the sheet change every single morning based on the bond market and the 10-year Treasury note. If the market is volatile, these sheets might even update two or three times in a single day.

For a transparent look at how this impacts your specific scenario, you can always explore our FAQ for quick answers on daily movements.

Decoding the Language of "Par Pricing"

When you look at a rate sheet, you will see a column for the interest rate (like 6.5%) and a column for the price (often expressed as a number like 100.00, 99.50, or 101.25).

Par Pricing A benchmark interest rate where the loan costs the borrower zero extra dollars in "points" and provides no "credits" toward closing costs. Practical Application: Finding the par rate is your baseline for comparing different loan offers without the noise of upfront costs.

Basis Points (BPS) A unit of measure used in finance to describe the percentage change in the value of financial instruments. One basis point is equal to 0.01%. Practical Application: If a rate sheet adjustment says "25 bps," it means a 0.25% change in the price of the loan.

If a rate is listed at a price of 100.00, that is "Par." If a rate is listed at 99.00, it means that rate costs 1 point (or 1% of the loan amount) to obtain. If a rate is listed at 101.00, it means that rate provides a 1% credit to help cover your closing costs.

Buying Down the Rate: The Discount Points Calculation

For many investors in high-growth areas like Virginia or Georgia, "buying down the rate" is a common strategy. This is especially true for landlords who plan to hold a property for 10 or 20 years. By paying a "discount point" upfront, you secure a lower monthly payment for the life of the loan.

Let's look at how this calculation works in a real-world scenario for a home purchase in Michigan or Indiana.

Discount Points Calculation Example

- Loan Amount: $300,000

- Base Rate (Par): 7.0%

- Target Rate: 6.75%

- Cost to get Target Rate: 1.000 Discount Point

- Calculation: $300,000 x 0.01 = $3,000

In this case, the investor pays $3,000 at closing to lower their interest rate by 0.25%. To see how this affects your long-term savings, you can use our mortgage calculators to run the numbers for your specific loan amount.

Image Instructions: Create a professional financial graphic titled "Reading Rate Sheets". Show the calculation: Loan Amount $300,000 x 1.000% Discount Point = $3,000 Cost. Show a side-by-side comparison of 7.0% vs 6.75%. At the bottom, include "Ebonie Beaco - Mortgage Loan Officer". No money or cash images.

Image Instructions: Create a professional financial graphic titled "Reading Rate Sheets". Show the calculation: Loan Amount $300,000 x 1.000% Discount Point = $3,000 Cost. Show a side-by-side comparison of 7.0% vs 6.75%. At the bottom, include "Ebonie Beaco - Mortgage Loan Officer". No money or cash images.

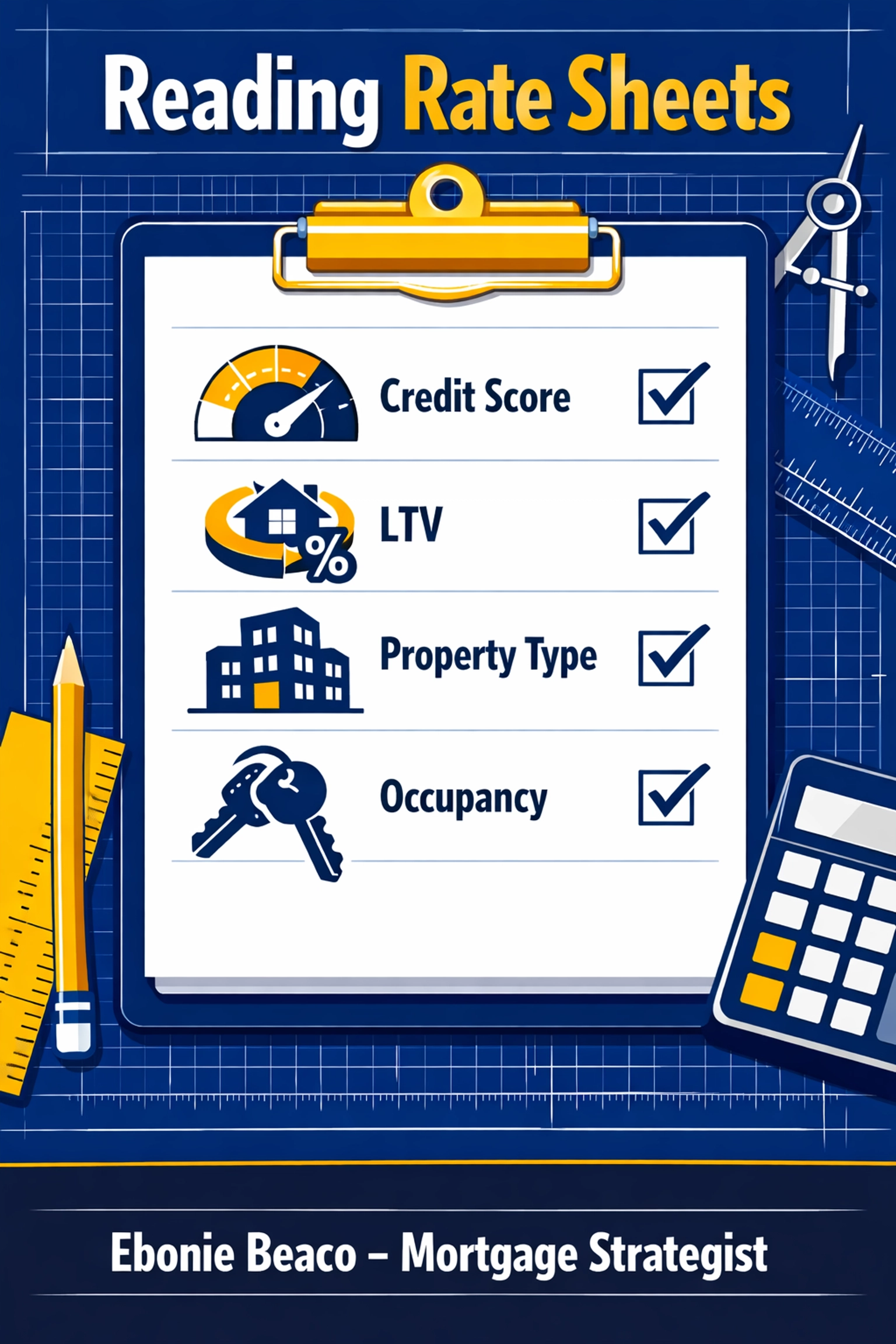

The "It Depends" Factor: Loan-Level Price Adjustments (LLPAs)

This is the section of the rate sheet that usually surprises people. You might see a "headline rate" on the news, but when you get your specific quote, it is different. This is due to LLPAs.

Loan-Level Price Adjustments (LLPAs) Risk-based pricing adjustments applied to a mortgage based on the specific characteristics of the borrower and the property. Practical Application: Understanding LLPAs helps you see why a higher credit score or a larger down payment directly lowers your monthly interest rate.

Here are the primary factors that trigger adjustments on a rate sheet:

1. Credit Score Tiers

Lenders view credit scores in brackets (e.g., 740-759, 720-739). The higher your score, the lower the "hit" to the price. For example, a borrower with a 660 score buying a home in California will likely pay more in points or have a higher rate than a borrower with a 780 score.

2. Loan-to-Value (LTV) Ratio

The more equity you have, the less risk the lender takes. An 80% LTV (20% down) typically has better pricing than a 95% LTV (5% down). However, there are unique brackets where pricing is actually better at 85% LTV because of Private Mortgage Insurance (PMI) coverage. You can read more about these nuances on our about us page.

3. Property Type

Are you buying a single-family home in a quiet suburb of Arkansas or a 4-unit building in Chicago? Multi-family properties (2-4 units) carry a pricing "hit" because they are seen as higher risk than single-family residences.

4. Occupancy

This is huge for our investor community. A primary residence gets the best pricing. A second home (vacation home) has different pricing, and an investment property (rental) has the most significant adjustments. For those looking at home purchase options, occupancy is a major driver of your final rate.

Lock Periods: Why Time is Money

When you look at a rate sheet, you will notice different columns for 15-day, 30-day, 45-day, and 60-day locks.

Rate Lock A guarantee from a lender that they will hold a specific interest rate and cost for a borrower for a set period. Practical Application: Locking your rate protects you from market spikes while your loan is being processed.

A 60-day lock is almost always more expensive than a 15-day lock. This is because the lender is taking on more "market risk" by promising you a rate further into the future. If you are close to closing on a property in Florida, a shorter lock might save you money, but if you are dealing with a complex renovation or a fix and flip, a longer lock provides peace of mind.

Investor-Specific Pricing: DSCR and Landlord Loans

For real estate investors focusing on DSCR (Debt Service Coverage Ratio) loans, the rate sheet looks a bit different. Instead of focusing heavily on your personal income or DTI (Debt-to-Income), the adjustments are focused on:

- The DSCR Ratio: Is the rent covering the mortgage? (e.g., 1.0x coverage vs 1.25x coverage).

- Prepayment Penalties: Investors often trade a lower interest rate for a longer prepayment penalty period (e.g., a 3-year or 5-year prepay).

- Short-Term Rental vs Long-Term Rental: Some lenders have specific adjustments for Airbnb or VRBO properties.

If you are a landlord in Kentucky or Missouri, understanding these specific "hits" on the DSCR rate sheet is the key factor in determining if a deal "pencils out." You can learn more about these specialized programs in our loan process guide.

Image Instructions: A clean infographic titled "Reading Rate Sheets" showing a checklist of rate influencers: Credit Score, LTV, Property Type (Single Family vs Multi-Unit), and Occupancy (Primary vs Investment). At the bottom, include "Ebonie Beaco - Mortgage Loan Officer". No money or cash images.

Image Instructions: A clean infographic titled "Reading Rate Sheets" showing a checklist of rate influencers: Credit Score, LTV, Property Type (Single Family vs Multi-Unit), and Occupancy (Primary vs Investment). At the bottom, include "Ebonie Beaco - Mortgage Loan Officer". No money or cash images.

The Role of the 10-Year Treasury

Why do rates move every day? Most mortgage rates are tied to the performance of Mortgage-Backed Securities (MBS), which closely track the 10-year Treasury note. When investors are worried about the economy, they buy bonds, which usually helps keep rates lower. When the economy is "heating up" or inflation is high, rates tend to climb.

As a mortgage strategist, I watch these movements so you don't have to. We aim to be a resource for you, much like a site map guides you through a website, we guide you through the complexities of the secondary market.

How to Compare Offers Like a Pro

Now that you know how a rate sheet is built, here is how you should compare offers:

- Ask for the "Par" Rate: This tells you the baseline without extra costs.

- Look at the Total Loan Costs: A lower rate might look good until you realize the lender is charging 2 points in "origination" or "discount" fees.

- Check the Lock Duration: Ensure both quotes are for the same number of days (e.g., both 30-day locks).

- Confirm the Program: Make sure you aren't comparing a Conventional loan quote to an FHA quote.

If you ever feel overwhelmed by the numbers, our testimonials show how we've helped others navigate these exact waters with total transparency.

Putting It All Together

Understanding rate sheets isn't about memorizing the numbers: it is about knowing which levers are being pulled behind the scenes. Your credit score, your down payment, the property type, and the market all dance together to create that final number on your Closing Disclosure.

Whether you are scaling a rental portfolio in Illinois or buying a retirement home in Virginia, having a strategist who will show you the "why" behind the "what" is the ultimate advantage.

Want the best rate? Contact Ebonie Beaco for a transparent look at today's mortgage rates.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664