Qualify for a Mortgage with 1099 Income

For many self-employed professionals, independent contractors, and gig economy workers, the path to homeownership often feels like a series of closed doors. You might have a thriving business in Chicago or a successful consulting firm in Florida, but traditional banks often look at your tax returns and see a different story.

Because traditional mortgage underwriting focuses on net income after deductions, the very write-offs that help your business succeed can actually hinder your ability to get a loan. However, 1099 mortgage programs are designed specifically to bridge this gap. These programs allow you to qualify based on your gross 1099 earnings rather than the net income shown on your tax returns.

What is a 1099 Mortgage?

1099 Mortgage: A specialized home loan program designed for self-employed individuals who receive IRS Form 1099 rather than W-2s. Practical Application: This allows a contractor or freelancer to use their total earnings as listed on their 1099 forms to qualify for a mortgage, bypasses the restrictive "net income" calculations found in conventional financing.

These loans fall under the category of Non-QM Mortgage Loans. Non-QM stands for Non-Qualified Mortgage. These are loans that do not fit the rigid criteria set by government-sponsored entities like Fannie Mae or Freddie Mac. Instead of focusing solely on tax returns, these programs prioritize your actual cash flow and ability to repay the debt.

Why Traditional Financing is Difficult for 1099 Workers

If you are a real estate investor in Alabama or a specialized consultant in California, you likely work with a CPA to maximize your business deductions. This is smart business. You might earn $150,000 in gross income, but after deducting equipment, travel, and home office expenses, your taxable income might only show as $60,000.

A traditional lender looks at that $60,000. They then apply a Debt-to-Income (DTI) calculation to that lower number.

Debt-to-Income (DTI) Ratio: A percentage that reflects how much of your monthly gross income goes toward paying your monthly debt obligations. Practical Application: Lenders use this to ensure you aren't overextended and have enough cushion to handle a new mortgage payment along with existing car loans or credit cards.

With a 1099 loan, we can often ignore those heavy tax deductions. We look at the $150,000. This significantly lowers your DTI and increases your purchasing power.

Key Requirements for a 1099 Mortgage

Qualifying for these programs is straightforward, but it does require specific documentation and financial health.

1. Credit Score Standards

While requirements vary by lender, most 1099 programs look for a credit score between 620 and 700. Generally, a score above 700 will secure the most competitive interest rates and lower down payment requirements. If you are looking to buy in competitive markets like Virginia or Georgia, having a higher score provides more leverage during the loan process.

2. Down Payment

Because these loans carry slightly more risk for the lender, you should expect to put down at least 10% to 20%. For real estate investors using this for a rental property, a 20% down payment is standard.

3. Income Documentation

Instead of the standard two years of full tax returns, a 1099 loan usually requires:

- Your 1099 forms from the last one to two years.

- A year-to-date (YTD) profit and loss (P&L) statement prepared by you or your bookkeeper.

- Proof of business license or a letter from a CPA verifying you have been in business for at least two years.

4. Employment History

Lenders generally want to see that you have been working in the same industry for at least two years. This demonstrates stability. If you recently transitioned from a W-2 job to a 1099 role in the same field, some lenders may consider that as continuous employment.

How the Calculation Works

Understanding the math is crucial for any investor or homeowner. Let's look at how a 1099 mortgage calculation differs from a traditional one.

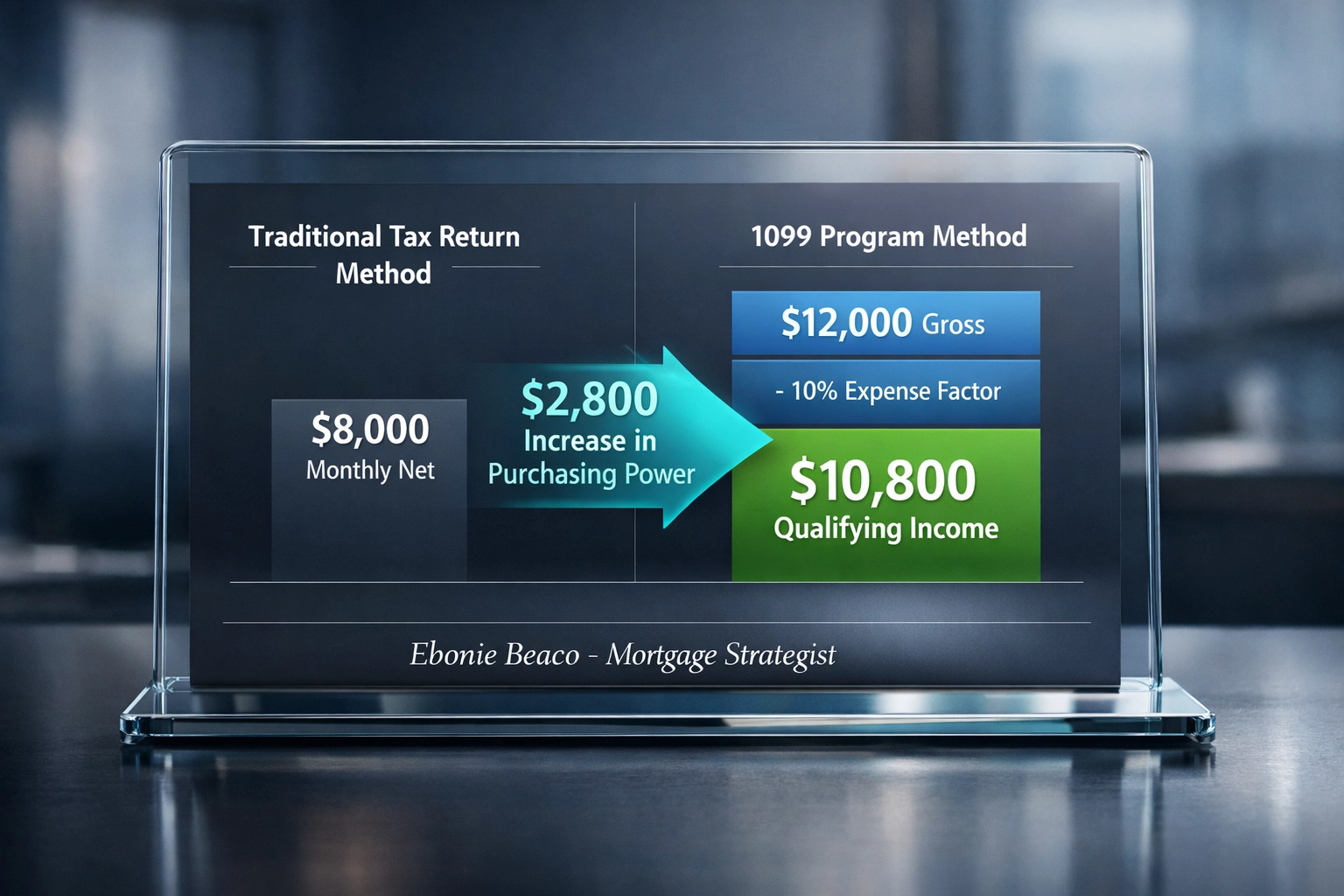

Imagine a freelance software developer in Michigan.

- Gross 1099 Income: $12,000 per month ($144,000/year).

- Tax Deductions: $4,000 per month in business expenses.

- Net Taxable Income: $8,000 per month ($96,000/year).

A traditional lender uses the $8,000. A 1099 lender uses the $12,000 and applies a standard expense factor (often 10%).

Calculation Example:

- $12,000 (Gross) x 0.90 (90% multiplier) = $10,800 Qualifying Monthly Income.

By using the 1099 method, this borrower has $2,800 more in monthly income to use for qualification. This could be the difference between qualifying for a $400,000 home versus a $650,000 home.

Image Title: 1099 Income Mortgages

Calculation shown: Gross Income $12,000 - 10% Expense Factor = $10,800 Qualifying Income. Traditional Net Income: $8,000. Difference: +$2,800/mo.

Bottom text: Ebonie Beaco - Mortgage Loan Officer

Image Title: 1099 Income Mortgages

Calculation shown: Gross Income $12,000 - 10% Expense Factor = $10,800 Qualifying Income. Traditional Net Income: $8,000. Difference: +$2,800/mo.

Bottom text: Ebonie Beaco - Mortgage Loan Officer

Strategic Use for Real Estate Investors

If you are a landlord or a real estate investor in markets like Indiana or Kentucky, you know that scaling a portfolio requires flexibility. Many investors utilize DSCR Investor Loans for their rentals, but when it comes to their primary residence, they often find themselves "trapped" by their tax returns.

DSCR (Debt Service Coverage Ratio): A metric used to qualify a property based on its ability to cover the mortgage payment with its own rental income. Practical Application: Investors use this to buy properties without using personal income, focusing instead on whether the "rent covers the note."

However, if you are an investor looking to buy a new primary home or perform a cash-out refinance on your personal residence to fund a new deal, 1099 loans are a powerful tool. You can access mortgage basics to see how these fit into your overall wealth-building strategy.

Steps to Prepare Your Application

If you are planning to apply for a 1099 mortgage in the next six months, there are specific steps you should take now to ensure a smooth approval.

- Organize Your 1099s: Ensure you have copies of every 1099 form issued to you. If you worked for multiple clients, you need the full picture.

- Separate Your Finances: If you haven't already, ensure your business expenses are paid out of a business account and personal expenses from a personal account. This "clean" accounting makes lenders much more comfortable.

- Monitor Your Credit: Avoid opening new lines of credit or making large purchases like a new car before applying. Use mortgage calculators to see how your current debts impact your buying power.

- Prepare a P&L: You don't always need a professional accountant for this, but your year-to-date profit and loss statement must be accurate and reflect the income shown on your bank statements.

1099 Mortgages vs. Bank Statement Loans

It is common to confuse these two programs. While both are Non-QM Mortgage Loans, they function differently.

Bank Statement Loan: A loan where the lender reviews 12 to 24 months of bank statements to calculate an average monthly deposit amount as income. Practical Application: This is ideal for business owners with many employees or high overhead where 1099 forms don't tell the whole story.

1099 Loan: Specifically uses the 1099 forms issued by your clients. Practical Application: This is often faster and requires less paperwork than a full bank statement review, making it perfect for independent contractors, Realtors, and consultants.

Explore the FAQ section to compare which of these might fit your specific business structure better.

Exploring the Market: From Chicago to Florida

The beauty of these programs is their availability across diverse markets. In high-cost areas like California or parts of Florida, traditional jumbo loan requirements are incredibly strict for the self-employed. 1099 programs provide a viable alternative for luxury home buyers who have the income but lack the "traditional" paperwork.

In cities like Chicago or throughout Virginia, where the real estate market remains active, being "pre-approved" with a 1099 program allows you to compete with W-2 buyers. Sellers don't care where your income comes from; they care that your financing is solid.

The Importance of Transparency

In the world of real estate finance, transparency is everything. Many borrowers are told "no" by big-box banks because their tax returns show a loss. We believe in looking at the reality of your bank account and the success of your business.

Whether you are a fix-and-flip investor in Missouri or a homeowner in Arkansas looking for a home refinance, there are options that reward your entrepreneurial spirit rather than punishing it.

Jump in and look at your earnings from a different perspective. If you have been told you don't qualify because of your 1099 status, it is time to look at a Non-QM solution.

Access our resources to learn more about how we help self-employed individuals navigate the complexities of the mortgage market. We are here to guide you clearly and confidently through every step of the process.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664