Private Mortgage Insurance (PMI): How to Avoid It on Rentals

If you are looking to build a rental portfolio, cash flow is the name of the game. Every dollar that leaves your pocket reduces your return on investment. One of the most common expenses that eats into monthly profits for newer investors is Private Mortgage Insurance, commonly known as PMI.

For many homeowners in markets like Chicago, Illinois, or the fast-growing suburbs of Atlanta, Georgia, PMI is seen as an unavoidable cost of entry when putting down a small down payment. However, when you transition into the world of real estate investing, PMI functions a bit differently.

Understanding how to navigate these insurance requirements can be the difference between a property that "cashes out" and one that just breaks even.

What is Private Mortgage Insurance (PMI)?

Private Mortgage Insurance (PMI): A risk-mitigation policy required by lenders when a borrower has less than 20% equity in a property. It protects the lender: not the borrower: in the event of a default.

In practical terms, PMI allows you to purchase a property with a smaller down payment, but you pay a monthly premium for that privilege. On a primary residence, this is standard. On a rental property, it can be a significant hurdle to achieving your desired Debt Service Coverage Ratio (DSCR).

Explore more about the fundamentals of these terms at Mortgage Basics.

The Reality of PMI on Investment Properties

Most conventional lenders actually require a minimum of 15% to 25% down for investment properties. Because the down payment requirement for rentals is naturally higher than for a primary residence, many investors accidentally avoid PMI simply by meeting the minimum loan requirements.

However, if you are using a conventional loan to buy a single-family rental with only 15% down, PMI will likely be part of your monthly payment. This added cost can stay with the loan until you reach 20% or 22% equity through principal paydown or market appreciation.

Strategies to Avoid PMI on Your Rentals

1. The 20% Down Payment Strategy

The most direct way to bypass PMI is to ensure your Loan-to-Value (LTV) ratio is 80% or lower at the time of purchase.

Loan-to-Value (LTV): A financial term used by lenders to express the ratio of a loan to the value of an asset purchased. It is calculated by dividing the loan amount by the appraised property value.

When you put 20% down, the lender views the investment as lower risk. You gain immediate equity, lower monthly payments, and a cleaner path to profitability.

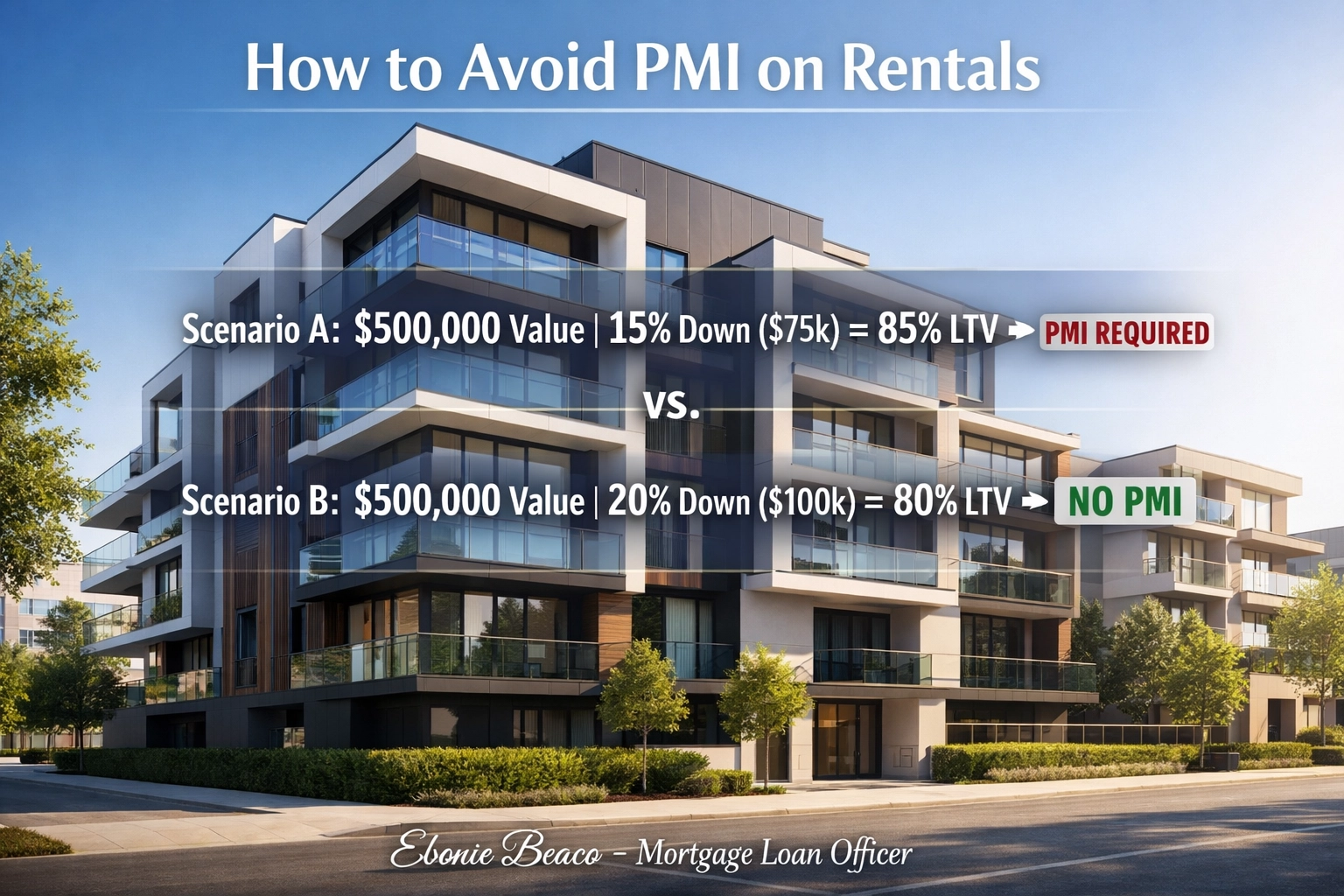

Visual Breakdown: How LTV Affects PMI

Calculation: Property Value $500,000 | 15% Down ($75k) = $425k Loan (85% LTV) -> PMI REQUIRED

Calculation: Property Value $500,000 | 20% Down ($100k) = $400k Loan (80% LTV) -> NO PMI

Title: How to Avoid PMI on Rentals | Ebonie Beaco - Mortgage Loan Officer

Visual Breakdown: How LTV Affects PMI

Calculation: Property Value $500,000 | 15% Down ($75k) = $425k Loan (85% LTV) -> PMI REQUIRED

Calculation: Property Value $500,000 | 20% Down ($100k) = $400k Loan (80% LTV) -> NO PMI

Title: How to Avoid PMI on Rentals | Ebonie Beaco - Mortgage Loan Officer

2. Lender-Paid Mortgage Insurance (LPMI)

Lender-Paid Mortgage Insurance is a strategy where the lender "pays" the PMI premium in exchange for a slightly higher interest rate on the loan.

Lender-Paid Mortgage Insurance (LPMI): A mortgage insurance arrangement where the lender covers the cost of the premium, usually resulting in a higher interest rate for the borrower over the life of the loan.

Jump in and compare this to monthly PMI. While the interest rate is higher, the total monthly payment might actually be lower than a standard loan with a separate PMI line item. This is particularly useful for investors who plan to hold the property for a shorter period or who need to maximize monthly cash flow to qualify for the loan.

3. Piggyback Loans (The 80/10/10 Structure)

A "piggyback" loan involves taking out two loans simultaneously to avoid the 20% down payment requirement while still avoiding PMI.

The structure usually looks like this:

- 80% First Mortgage: The primary loan.

- 10% Second Mortgage: Often a HELOC or a fixed-rate second lien.

- 10% Down Payment: Your cash contribution.

Because the first mortgage is at exactly 80% LTV, no PMI is required. This strategy is popular in high-priced markets like Los Angeles, California, or Miami, Florida, where coming up with a full 20% down payment on a multi-unit property can be a massive capital hurdle.

Transitioning from Primary to Rental (The BRRRR Method)

Many investors in Alabama and Arkansas use the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) to scale.

If you purchase a distressed property with a hard money loan or bridge loan, you aren't dealing with PMI initially. Once the renovation is complete and the property is appraised at a higher value, you can perform a Cash-Out Refinance.

If your new appraised value is high enough that your new loan represents 80% or less of the value, you have effectively acquired a rental property with no PMI and potentially very little of your own "out-of-pocket" cash left in the deal.

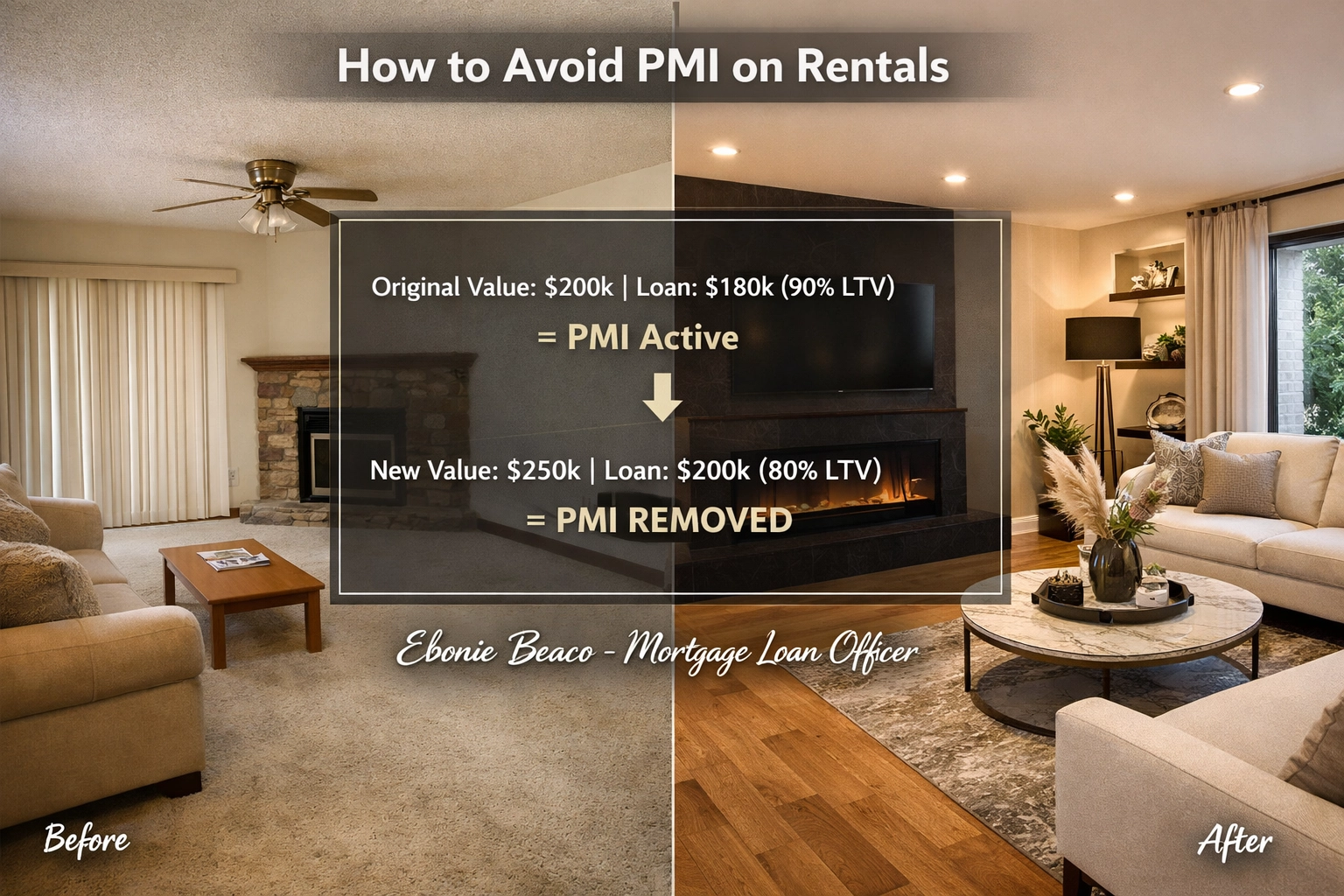

Visual Breakdown: Using a Cash-Out Refinance to Remove PMI

Scenario: Original Value $200k | Current Loan $180k (90% LTV) -> Paying PMI

New Appraised Value after Reno: $250k | New Loan $200k (80% LTV) -> PMI REMOVED

Title: How to Avoid PMI on Rentals | Ebonie Beaco - Mortgage Loan Officer

Visual Breakdown: Using a Cash-Out Refinance to Remove PMI

Scenario: Original Value $200k | Current Loan $180k (90% LTV) -> Paying PMI

New Appraised Value after Reno: $250k | New Loan $200k (80% LTV) -> PMI REMOVED

Title: How to Avoid PMI on Rentals | Ebonie Beaco - Mortgage Loan Officer

DSCR Loans: The Investor Alternative

For many professional landlords, traditional conventional loans with PMI requirements are too restrictive. This is where DSCR (Debt Service Coverage Ratio) Loans come into play.

DSCR Loan: A type of "Non-QM" loan that qualifies a borrower based on the rental income of the property rather than personal income or debt-to-income ratios.

DSCR loans typically do not have a separate "PMI" line item. Instead, the risk is baked into the interest rate and the LTV requirements. Most DSCR lenders require at least 20% down (80% LTV) anyway, which naturally eliminates the concept of PMI.

If you are looking at multi-unit apartment buildings or short-term rentals in vacation spots like Virginia Beach or the Florida Keys, DSCR loans often provide a more streamlined path to funding without the headaches of private mortgage insurance.

Access more details on these programs at Home Purchase.

How PMI Impacts Different Markets

The strategy you choose often depends on where you are buying.

- Midwest Markets (Michigan, Indiana, Kentucky): In these regions, property values are often lower. It may be easier to save the full 20% down payment to avoid PMI and secure the best possible cash flow.

- High-Appreciation Markets (California, Florida): In these states, prices can rise rapidly. An investor might choose to pay PMI temporarily with a 15% down payment, betting that equity growth will allow them to refinance or request PMI removal within 12 to 24 months.

- Urban Centers (Chicago): Investors looking at 2-4 unit buildings often find that the rental income easily covers the PMI, making it a viable "cost of doing business" to keep more cash in their reserves for future renovations.

Removing PMI from an Existing Rental

If you already have a rental property and you are currently paying PMI, you don't necessarily have to wait until the loan balance hits 78% of the original price.

- Request a New Appraisal: If the market in your area (like Northern Virginia or parts of Missouri) has seen significant growth, your current LTV might already be below 80%.

- Substantial Improvements: If you have renovated the kitchen, added a bedroom, or updated the mechanicals, you can often request PMI removal based on the increased value.

- Refinance: Sometimes the simplest way to drop PMI is to move into a new loan product entirely, especially if interest rates have dropped or if you want to move from a conventional loan into a DSCR loan.

Check your potential savings using our Mortgage Calculators.

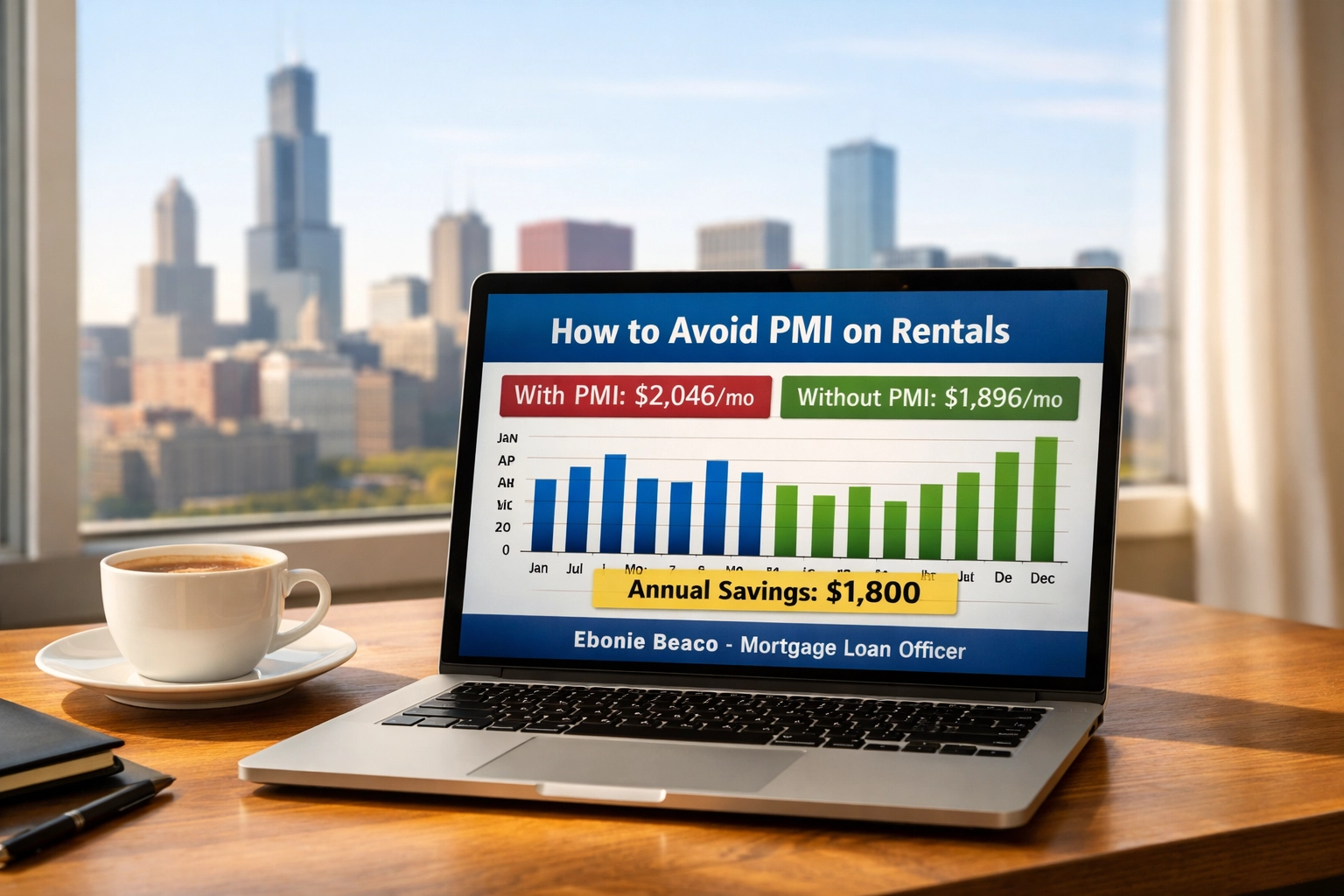

Visual Breakdown: Monthly Savings Comparison

Loan Amount: $300,000 | Interest Rate: 6.5%

With PMI ($150/mo): Total Payment $2,046

Without PMI ($0/mo): Total Payment $1,896

Annual Savings: $1,800

Title: How to Avoid PMI on Rentals | Ebonie Beaco - Mortgage Loan Officer

Visual Breakdown: Monthly Savings Comparison

Loan Amount: $300,000 | Interest Rate: 6.5%

With PMI ($150/mo): Total Payment $2,046

Without PMI ($0/mo): Total Payment $1,896

Annual Savings: $1,800

Title: How to Avoid PMI on Rentals | Ebonie Beaco - Mortgage Loan Officer

Summary for the Smart Investor

Avoiding PMI on rentals isn't just about saving a few dollars; it's about optimizing your portfolio for long-term stability. Whether you choose to put 20% down, utilize a piggyback loan, or leverage the power of a DSCR loan, the goal is to keep your expenses low and your equity high.

Every investment scenario is unique. A strategy that works for a fix-and-flip in Detroit might not be the best fit for a long-term Airbnb in Orlando.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

For more information on mortgage options or mentoring, contact Ebonie Beaco at www.homeloansnetwork.com.