Private Money vs. Hard Money: Which is Right for You?

Navigating the world of real estate investing requires more than just finding a great property in Chicago or a flip-ready bungalow in Florida. It requires capital. When traditional banks say "no" because of your debt-to-income ratio or the condition of the property, you generally turn to two main sources: hard money and private money.

While people often use these terms interchangeably, they represent two different approaches to financing. Understanding the nuances between them influences your profit margins and how quickly you can scale your portfolio.

Defining the Terms

Hard Money Definition: A short-term, asset-based loan issued by professional lending companies, secured by the value of the real estate rather than the creditworthiness of the borrower. Practical Application: Use this when you need to close a deal in days, not weeks, and the property needs significant repairs that a traditional bank won't touch.

Private Money Definition: Capital provided by individual investors or small private groups, often based on personal relationships and flexible, negotiated terms. Practical Application: Use this when you want to build a long-term partnership with a lender who values your track record and is willing to structure creative repayment schedules.

The Hard Money Landscape

Hard money lenders are professional organizations. They have set criteria, specific application processes, and a clear fee structure. In markets like Atlanta, Georgia, or Richmond, Virginia, hard money is the engine behind many fix-and-flip operations.

These lenders focus primarily on the After Repair Value (ARV). They want to know that if you fail to finish the project, the property itself holds enough value to cover the debt. Because they take on higher risk by lending on distressed properties, they charge higher interest rates: often ranging from 8% to 15%.

Accessing hard money is usually faster than a traditional mortgage. You can find more details on how these timelines work at our loan process page. If you are looking to secure a property in a competitive market like Los Angeles or Miami, speed is your greatest asset. Hard money provides that speed.

The Private Money Advantage

Private money is more about the "who" than just the "what." This capital comes from people you might know: doctors, lawyers, or even other successful real estate investors who want a passive return on their cash.

Because private money is not coming from a corporate entity, the rules are less rigid. You can negotiate things like interest-only payments, deferred points, or even profit-sharing arrangements. For a BRRRR investor (Buy, Rehab, Rent, Refinance, Repeat) in Birmingham, Alabama, or Little Rock, Arkansas, private money can be the bridge that allows for a seamless transition into a long-term DSCR rental property loan.

One of the standout benefits of private money is the flexibility regarding your personal financials. While a hard money lender might still want to see a credit score, a private individual might care more about your exit strategy and your local market knowledge.

Image Instructions: Title "Private Lending Guide" centered at the top. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. The central graphic should be a professional comparison chart showing "Hard Money: Speed & Professionalism" vs "Private Money: Flexibility & Relationships." No money or cash icons.

Image Instructions: Title "Private Lending Guide" centered at the top. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. The central graphic should be a professional comparison chart showing "Hard Money: Speed & Professionalism" vs "Private Money: Flexibility & Relationships." No money or cash icons.

Understanding the Cost: Points and Interest

Both hard money and private money come with costs that exceed traditional mortgage rates. You must account for "points" and "interest" when calculating your potential ROI.

Points are up-front fees paid to the lender at closing. One point equals 1% of the loan amount. Interest is the ongoing cost of borrowing the money, usually expressed as an annual percentage rate (APR) but often calculated monthly.

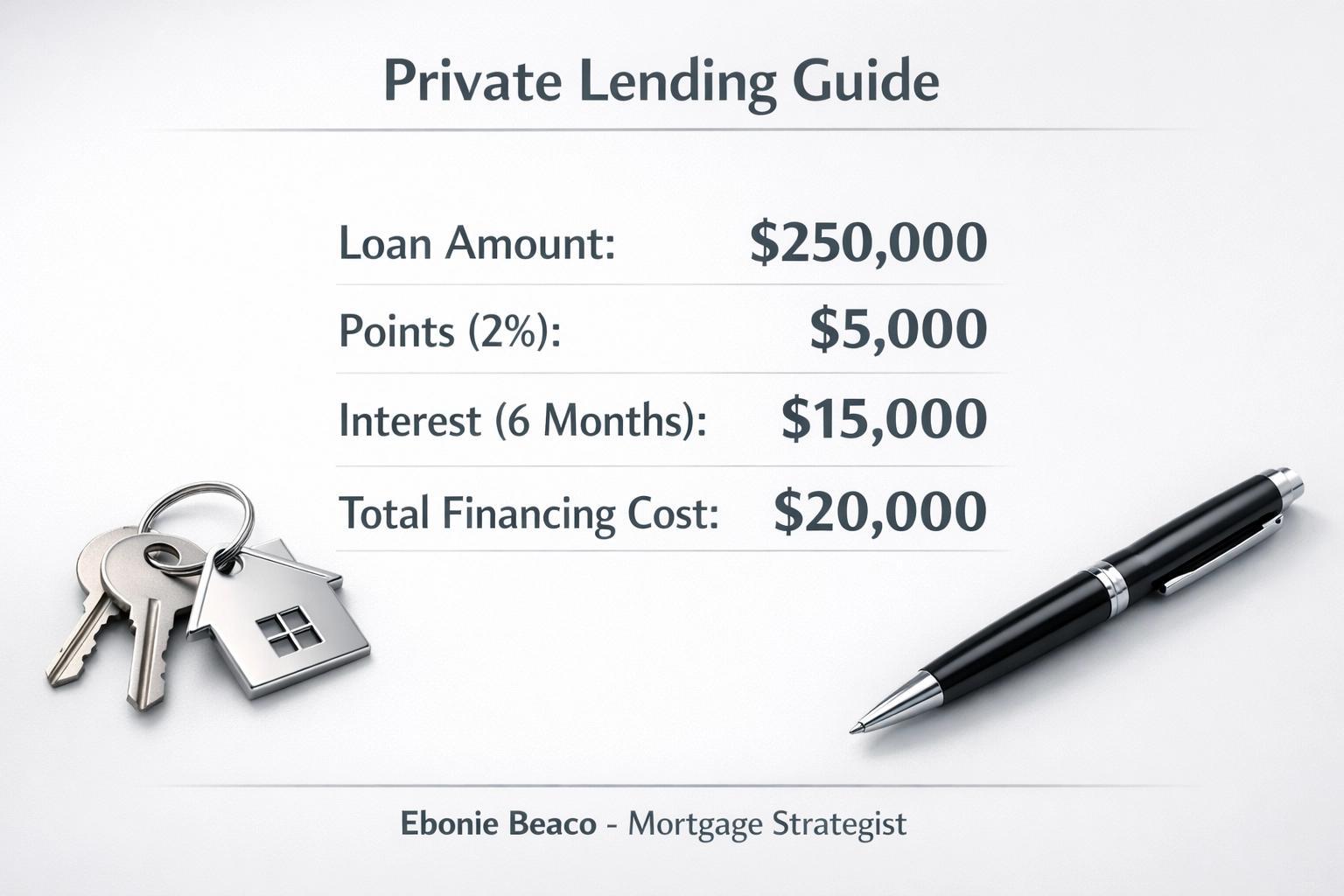

Let’s look at a practical calculation for an investor purchasing a property in Indianapolis, Indiana.

The Scenario:

- Loan Amount: $250,000

- Points: 2 ($5,000)

- Interest Rate: 12% annually (1% per month)

- Loan Term: 6 months

The Calculation:

- Points Cost: $250,000 x 0.02 = $5,000

- Monthly Interest: ($250,000 x 0.12) / 12 = $2,500 per month

- Total Interest (6 months): $2,500 x 6 = $15,000

- Total Cost of Capital: $5,000 (points) + $15,000 (interest) = $20,000

Image Instructions: Title "Private Lending Guide" at the top. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Create a visual deal breakdown graphic using the following numbers: Loan Amount $250,000, 2 Points = $5,000, 12% Interest (6 Months) = $15,000, Total Financing Cost = $20,000. Use a clean, professional layout. No money or cash.

Image Instructions: Title "Private Lending Guide" at the top. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Create a visual deal breakdown graphic using the following numbers: Loan Amount $250,000, 2 Points = $5,000, 12% Interest (6 Months) = $15,000, Total Financing Cost = $20,000. Use a clean, professional layout. No money or cash.

Comparing Key Factors

When deciding which path to take, you should evaluate your project based on these specific categories. You can also explore our FAQ for more insight into common investor hurdles.

1. Speed of Funding

Hard money lenders are built for speed. If you are at a foreclosure auction in Chicago or trying to beat out a cash buyer in Virginia Beach, a hard money lender can often fund in 3 to 7 days. Private money depends entirely on the individual. If their funds are tied up in another investment, you might have to wait.

2. Underwriting Requirements

Hard money lenders will require an appraisal (often an ARV appraisal), a title search, and proof of insurance. Private lenders may skip the formal appraisal if they trust your "comps" (comparable sales). This lack of red tape can be a massive benefit for experienced investors who have built a reputation for accuracy.

3. Loan Terms and Length

Hard money is almost exclusively short-term, usually 6 to 18 months. If your project runs over schedule, extending a hard money loan can be expensive. Private money terms are negotiable. You might be able to secure a 2-year or 3-year term, which is helpful if you are waiting for market conditions to shift before selling or refinancing into a home purchase loan.

4. The Relationship Dynamic

Hard money is a transaction. Private money is a partnership. A hard money lender might not care if your contractor quit, but a private lender might work with you to find a solution because they are invested in your success.

When to Pivot to Traditional Financing

Both hard money and private money are "bridge" solutions. They get you from point A (acquisition and renovation) to point B (sale or long-term hold). Once the property is stabilized and renovated, many investors in states like Michigan or Missouri choose to refinance.

This is where a Cash-Out Refinance or a DSCR (Debt Service Coverage Ratio) Loan becomes vital. These programs allow you to pay off your high-interest private or hard money loan and lock in a lower, long-term rate based on the property's rental income. You can learn more about these strategies on our home refinance page.

Strategic Choices for Different Investors

For the New Investor: If you are just starting out in places like St. Louis or Louisville, hard money might be easier to access. Professional lenders have the infrastructure to guide you through the process, even if they charge a premium. It serves as a "sanity check" on your numbers; if a hard money lender won't fund the deal, it might not be a good deal.

For the Scaling Landlord: If you already own several units in California or Florida, building a network of private lenders is a game-changer. It allows you to move faster without the constant "hard credit pulls" associated with professional lending institutions.

Final Considerations for Your Next Deal

Choosing between these options impacts your bottom line and your stress levels. Hard money offers reliability and speed. Private money offers flexibility and lower costs if you have the right connections.

If you are looking to scale your portfolio in 2026, you need a strategy that encompasses both acquisition and the eventual exit into long-term financing. Whether you are looking for fix-and-flip funds or a way to move your equity into a new project, understanding the landscape is the first step.

Explore our mortgage calculators to run your own numbers and see how different interest rates affect your monthly cash flow.

Image Instructions: Title "Private Lending Guide" at the top. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Use a professional graphic showing a map of the United States with highlights on IL, FL, GA, and CA to represent the markets discussed. No money or cash.

Image Instructions: Title "Private Lending Guide" at the top. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Use a professional graphic showing a map of the United States with highlights on IL, FL, GA, and CA to represent the markets discussed. No money or cash.

Real estate investing is a marathon, not a sprint. The way you finance your deals today dictates the opportunities you can take advantage of tomorrow. By leveraging the right mix of hard and private money, you can keep your capital moving and your portfolio growing.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664