Prepayment Penalties on Investment Loans: What to Know

When you are deep in the trenches of real estate investing, whether you are scouring the Chicago suburbs for a multi-unit or looking at vacation rentals in sunny Florida, you probably spend a lot of time obsessing over interest rates and down payments.

However, there is one clause tucked away in your loan documents that can drastically change your exit strategy: the prepayment penalty.

If you have ever wondered why a lender would "punish" you for paying back a loan early, you are not alone. It sounds counterintuitive. But in the world of investment financing, understanding these fees is a critical part of protecting your cash flow and your long-term equity.

What is a Prepayment Penalty?

A prepayment penalty is a fee charged by a lender if you pay off your mortgage or a significant portion of it before a specific date.

Lenders aren't just being difficult; they are protecting their investment. When a bank or private lender issues a loan, they expect to earn a certain amount of interest over a set period. If you pay that loan off in year two instead of year thirty, they lose out on years of anticipated profit. The penalty helps bridge that financial gap.

Explore more foundational concepts at our Mortgage Basics page to see how these terms fit into the bigger picture.

Why Do Investment Loans Have These Fees?

If you are buying a primary residence with a conventional loan, prepayment penalties are rare due to strict regulations. But for investment properties, especially those using DSCR (Debt Service Coverage Ratio) or Hard Money, the rules are different.

Investment loans are often sold to private investors on the secondary market. These investors want a "yield maintenance," which is just a fancy way of saying they want to guarantee they make their money.

In high-activity markets like California, Georgia, or Virginia, where investors often use the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), these penalties can catch you off guard if you plan to refinance quickly.

How the Math Works: Calculating the Penalty

Lenders don't just pull these numbers out of thin air. They typically use one of four common methods to calculate what you owe if you exit the deal early.

1. Percentage of the Remaining Balance

This is the most straightforward method. The lender charges a flat percentage, usually between 1% and 5%, of your outstanding principal at the time of payoff.

Example Calculation:

- Remaining Loan Balance: $400,000

- Penalty Rate: 3%

- Total Penalty Fee: $12,000

2. Number of Months of Interest

Some lenders charge a set number of months of interest. Usually, this is six months.

Example Calculation:

- Loan Balance: $300,000

- Interest Rate: 7%

- Annual Interest: $21,000

- Six Months of Interest Penalty: $10,500

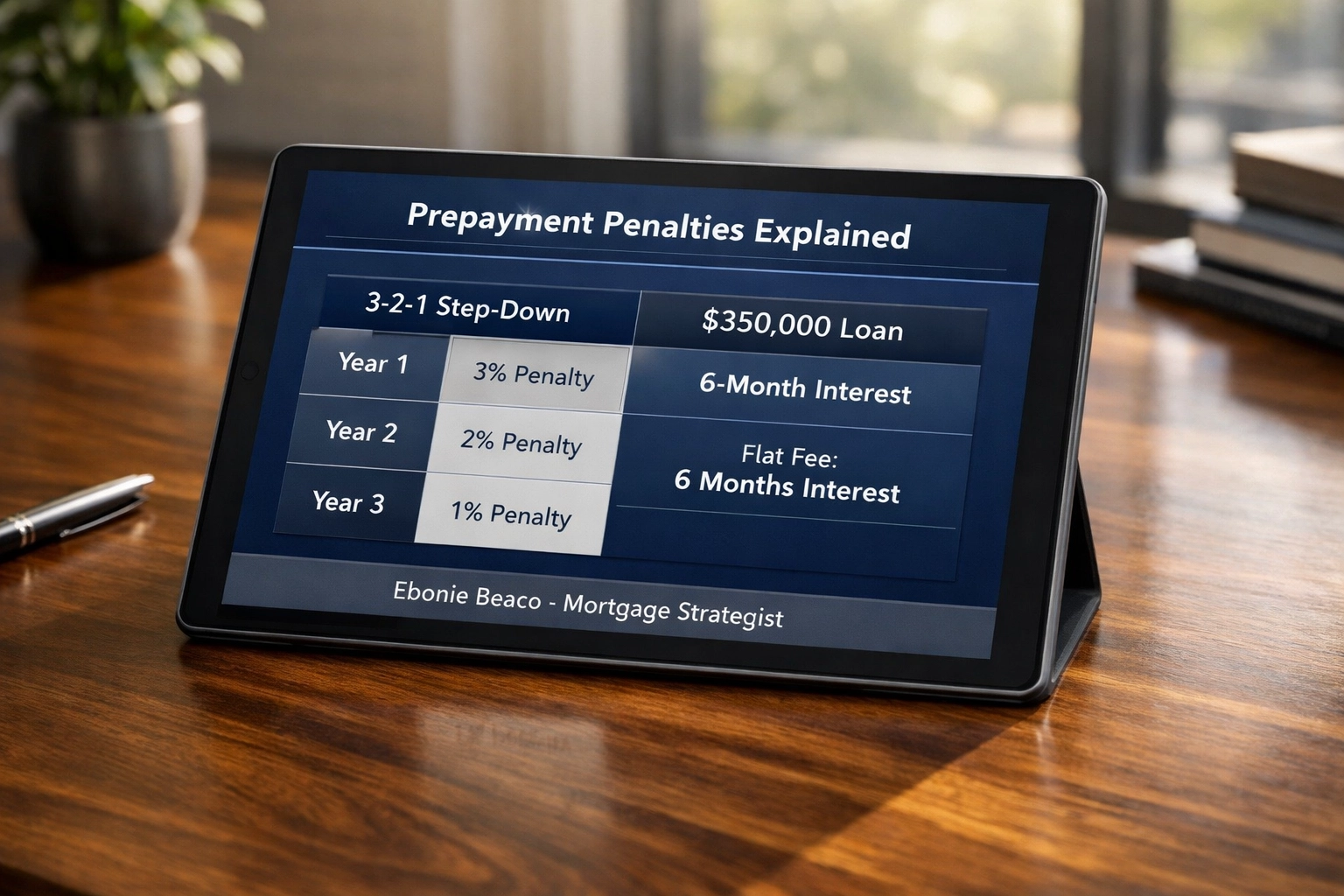

3. Sliding Scale (Step-Down)

This is very common in the Non-QM and DSCR world. The penalty decreases every year you hold the loan. A common structure is the "3-2-1" penalty.

- Year 1: 3% penalty

- Year 2: 2% penalty

- Year 3: 1% penalty

- Year 4+: 0% penalty

4. Yield Maintenance

This is the most complex version, often found in commercial real estate. It involves a formula that compares your current interest rate to the current market rates to ensure the lender gets the same "yield" they would have if you hadn't paid early.

(Image Instruction: Title 'Prepayment Penalties Explained' on the image. Show a clear comparison table of the 3-2-1 sliding scale vs a flat 6-month interest penalty on a $350,000 loan. Include labels for 'Year 1', 'Year 2', and 'Penalty Amount'. 'Ebonie Beaco - Mortgage Loan Officer' at the bottom. No money or cash icons.)

(Image Instruction: Title 'Prepayment Penalties Explained' on the image. Show a clear comparison table of the 3-2-1 sliding scale vs a flat 6-month interest penalty on a $350,000 loan. Include labels for 'Year 1', 'Year 2', and 'Penalty Amount'. 'Ebonie Beaco - Mortgage Loan Officer' at the bottom. No money or cash icons.)

Conventional Loans vs. DSCR Loans

It is important to distinguish between the types of financing you are using.

Conventional Mortgages: Under the Dodd-Frank Act, prepayment penalties on qualified mortgages (your standard 30-year fixed for a primary home) are heavily restricted. They can generally only be charged during the first three years and are capped at 2% for the first two years and 1% for the third.

DSCR and Investor Loans: Because these are business-purpose loans, they are not governed by the same consumer protection laws. It is common to see penalty periods of five years in states like Alabama, Michigan, or Indiana. If you are looking to build a portfolio, you need to Compare Loan Options carefully to ensure the penalty period aligns with your intended hold time.

The Cost-Benefit Analysis: Should You Pay the Fee?

Sometimes, paying the penalty actually makes financial sense. This usually happens when interest rates drop significantly or when you have a massive opportunity to sell for a profit.

Let’s look at a scenario for an investor in Atlanta, Georgia:

- Current Loan: $500,000 at 8.5% interest.

- New Rate Available: 6.0% interest.

- Prepayment Penalty: $15,000 (3% of balance).

- Monthly Savings by Refinancing: ~$800.

In this case, it would take about 19 months ($15,000 / $800) to break even on the penalty. If you plan to hold that property for another ten years, paying that $15,000 upfront is a smart move because you will save tens of thousands in interest over the long haul.

You can run your own numbers using our Mortgage Calculators to see how an early payoff affects your bottom line.

Can You Buy Down a Prepayment Penalty?

Yes, many investor programs allow you to "buy down" the penalty.

If you know you are doing a fix-and-flip in a high-demand area like Northern Virginia or parts of Arkansas, you don't want a 5-year penalty. You can often choose a "0-0-0" option (no penalty) in exchange for a slightly higher interest rate.

- Standard Option: 7.5% rate with a 3-year penalty.

- Buy-Down Option: 7.875% rate with no penalty.

For a short-term hold, the higher rate is almost always better than a five-figure exit fee. Jump in and review our FAQ for more details on how to structure these deals.

Impact on Different Investor Types

- Buy and Hold Landlords: If you are planning to keep a rental property in Missouri or Kentucky for 20 years, a prepayment penalty barely impacts you. You can take the lower interest rate that usually comes with a longer penalty period.

- Fix and Flip Investors: You should almost always avoid prepayment penalties. Your goal is to exit the loan in 6–12 months.

- Airbnb/Short-Term Rental Hosts: Since STR markets can be volatile, having a shorter penalty period (1 or 2 years) provides a safety net if you need to sell the property quickly.

Transparency in Lending

The key to navigating these fees is transparency. Your lender is required to disclose prepayment penalties on the Loan Estimate and the Closing Disclosure.

Never sign your closing docs without looking for the section that asks, "Does this loan have a prepayment penalty?" If the answer is yes, you need to know exactly how much and for how long.

If you are feeling uncertain about your current loan terms or need a second pair of eyes on a deal in California or Florida, you can Contact Ebonie Beaco to check your loan terms or discuss mentoring for your next investment.

Final Thoughts for Investors

Prepayment penalties are a tool, not a trap. They allow lenders to offer better rates to long-term investors by guaranteeing a certain level of return. Your job as an investor is to match the penalty period to your business plan.

If you are building a portfolio in the current market, whether it's in the heart of Chicago or across the state of Virginia, understanding the fine print is what separates the hobbyists from the professionals.

Access our About Us page to learn more about how we help investors strategize for long-term growth.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664