Pre-Qualified vs. Pre-Approved: Why One is Way Stronger Than the Other

Starting your home search is a rush. You are browsing listings in Chicago or checking out beachfront condos in Florida, and you want to jump in. Before you fall in love with a property, you need to understand your budget. Most people start by asking about a pre-qualification or a pre-approval. While they sound similar, they carry different weights in the real estate world.

Defining the Basics

Pre-qualification A preliminary evaluation of a borrower's creditworthiness based on self-reported data. Practical application: This serves as a quick starting point to see if you are in the ballpark for a loan.

Pre-approval A formal commitment from a lender to provide a specific loan amount based on verified financial documentation. Practical benefit: This document shows sellers in competitive markets like Virginia or Georgia that you have the financial backing to close.

The Power of Verification

A pre-qualification is essentially a conversation. You tell a lender how much you make and what your debts look like. They do a soft credit pull and give you a ballpark figure. It is fast, but it is not a guarantee.

A pre-approval is a deep dive. We look at your tax returns, pay stubs, and bank statements. We verify your employment and your assets. Because we have seen the paperwork, we can issue a letter that holds real value.

Explore the mortgage basics to see how these initial steps set the foundation for your entire purchase.

Why Sellers Prefer Pre-Approval

Imagine you are a seller in a hot market like Austin or Indianapolis. You receive two offers. One buyer has a pre-qualification letter that says they "should" be able to afford the home. The other buyer has a pre-approval letter stating the lender has already verified their income and assets.

The pre-approved buyer wins almost every time. Sellers want certainty. They do not want a deal to fall through three weeks into escrow because the buyer’s income couldn't be verified.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image displays a comparison chart highlighting that Pre-Approval involves verified documentation while Pre-Qualification is based on self-reported data.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image displays a comparison chart highlighting that Pre-Approval involves verified documentation while Pre-Qualification is based on self-reported data.

The Financial Impact of the Deep Dive

When we perform a full pre-approval, we often find things that the borrower forgot to mention. Maybe there is an old student loan or a car payment that impacts your Debt-to-Income (DTI) ratio. Discovering this early allows us to fix it before you make an offer.

If you rely on a pre-qualification, you might find out halfway through the loan process that you actually qualify for less than you thought. That is a heartbreaking way to lose a house.

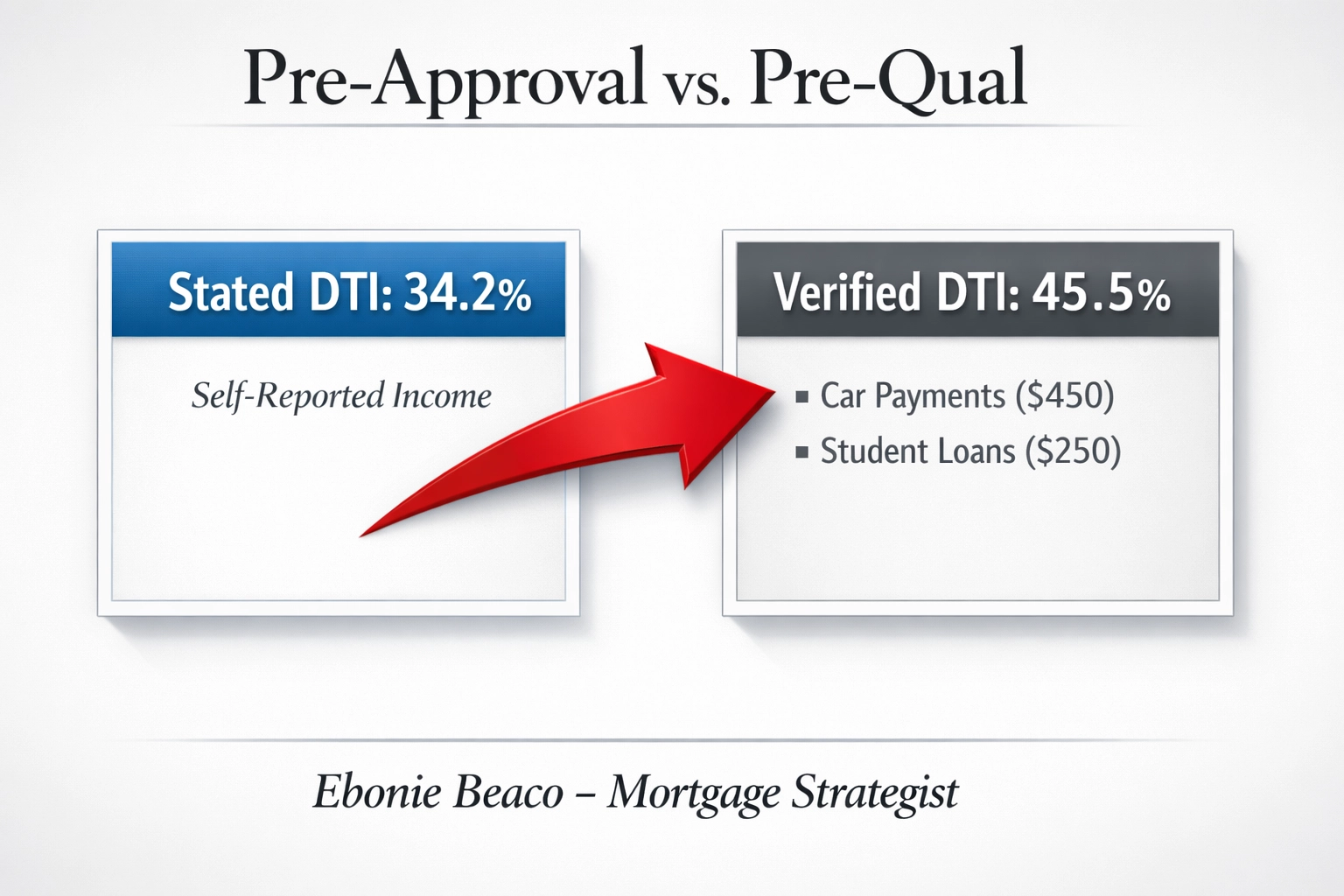

Real-World Calculation: The DTI Difference

Let’s look at how verification changes the numbers. In this scenario, a buyer is looking at a home in a suburb of Chicago.

The Scenario:

- Gross Monthly Income: $7,000

- Estimated Monthly Mortgage: $2,100

- Borrower's stated debts: $300 (just a credit card)

Pre-Qualification View:

- Stated DTI: 34.2% ($2,400 / $7,000)

- Result: "You look great! Go shop for that $350k home."

Pre-Approval View (After Verification):

- Verified Monthly Income: $6,800 (averaging overtime/bonuses)

- Verified Debts found on Credit Report: $300 credit card + $450 car payment + $250 student loan = $1,000 total debt.

- Total Monthly Obligations: $3,100 ($2,100 mortgage + $1,000 debt)

- Actual DTI: 45.5% ($3,100 / $6,800)

- Result: The buyer might need to look at a lower price point or pay off the car loan to qualify comfortably.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image shows the calculation: Stated DTI 34.2% vs. Verified DTI 45.5%. Includes labels for Income, Car Payments, and Student Loans.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image shows the calculation: Stated DTI 34.2% vs. Verified DTI 45.5%. Includes labels for Income, Car Payments, and Student Loans.

Investors and the Pre-Approval Advantage

If you are a real estate investor looking at rental properties in Alabama or Arkansas, pre-approval is your best friend. Investors often juggle multiple properties and complex tax returns. A simple pre-qualification is almost useless for a landlord with a growing portfolio.

For those using DSCR Investor Loans (Debt Service Coverage Ratio), the focus is on the property's income rather than personal income. Even then, getting pre-approved for the program parameters is vital. It shows wholesalers and commercial brokers that you are a serious player ready to execute a deal.

Access our mortgage calculators to run your own preliminary numbers before we start the formal verification.

Documentation Needed for a Strong Pre-Approval

To move from a "maybe" to a "yes," you will need to gather your paperwork. Being organized speeds up the timeline significantly. Generally, you should have these ready:

- Income Proof: W-2s from the last two years and your most recent pay stubs.

- Asset Statements: Two months of bank statements for all accounts.

- Tax Returns: The last two years of personal (and business, if applicable) tax returns.

- Credit History: We will pull a formal credit report to see your scores and existing debt obligations.

- Identification: Your driver's license and social security card.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image features a checklist of documents: W-2s, Pay Stubs, Bank Statements, and Tax Returns.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image features a checklist of documents: W-2s, Pay Stubs, Bank Statements, and Tax Returns.

Timing Your Pre-Approval

A pre-approval letter usually lasts for 60 to 90 days. If you are just starting to think about buying a year from now, a pre-qualification is fine for a rough estimate. However, if you plan to visit houses next weekend, you need that pre-approval in hand.

In high-demand areas like Northern Virginia or parts of California, homes sell in days. You cannot wait until Monday morning to ask for a letter when the offer deadline is Sunday night.

Moving Fast with Confidence

The ultimate benefit of a pre-approval is confidence. When you walk into a home, you know exactly what your monthly payment will be. You know exactly how much cash you need for the down payment and closing costs.

This transparency reduces stress. Buying a home is a big emotional and financial commitment. Knowing that a mortgage strategist has already vetted your numbers allows you to focus on the property itself rather than worrying about the financing falling through.

Jump in and review our FAQ page for more answers to common home-buying questions.

The Role of Your Loan Officer

Your loan officer is your guide through this maze. We don't just run numbers; we strategize. If your DTI is a little high for the home you want, we can look at options like a Cash-Out Refinance on another property to consolidate debt, or perhaps a Non-QM Mortgage Loan if your situation is unique.

We serve homeowners and investors across multiple states including Michigan, Kentucky, and Missouri. Each market has its own nuances, but the need for a solid financial foundation is universal.

Transitioning to the Offer Stage

Once you are pre-approved, you are a "cash-like" buyer in the eyes of many sellers. Your offer is seen as lower risk. In a bidding war, having a pre-approval from a reputable lender like Home Loans Network can be the tie-breaker that gets your offer accepted.

Compare your options carefully. Don't settle for a "quick" online pre-qualification that hasn't been verified by a human expert. It could cost you your dream home.

Image Title: Pre-Approval vs. Pre-Qual. Bottom: Ebonie Beaco - Mortgage Loan Officer. Image shows a "Winning Offer" stamp next to a Pre-Approval letter graphic.

Get a solid pre-approval today. Contact Ebonie Beaco to start your home search.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664