Pending Sales: A Small Bump in a Stagnant Market

Editorial by Ebonie Beaco – Mortgage Strategist March 17, 2026

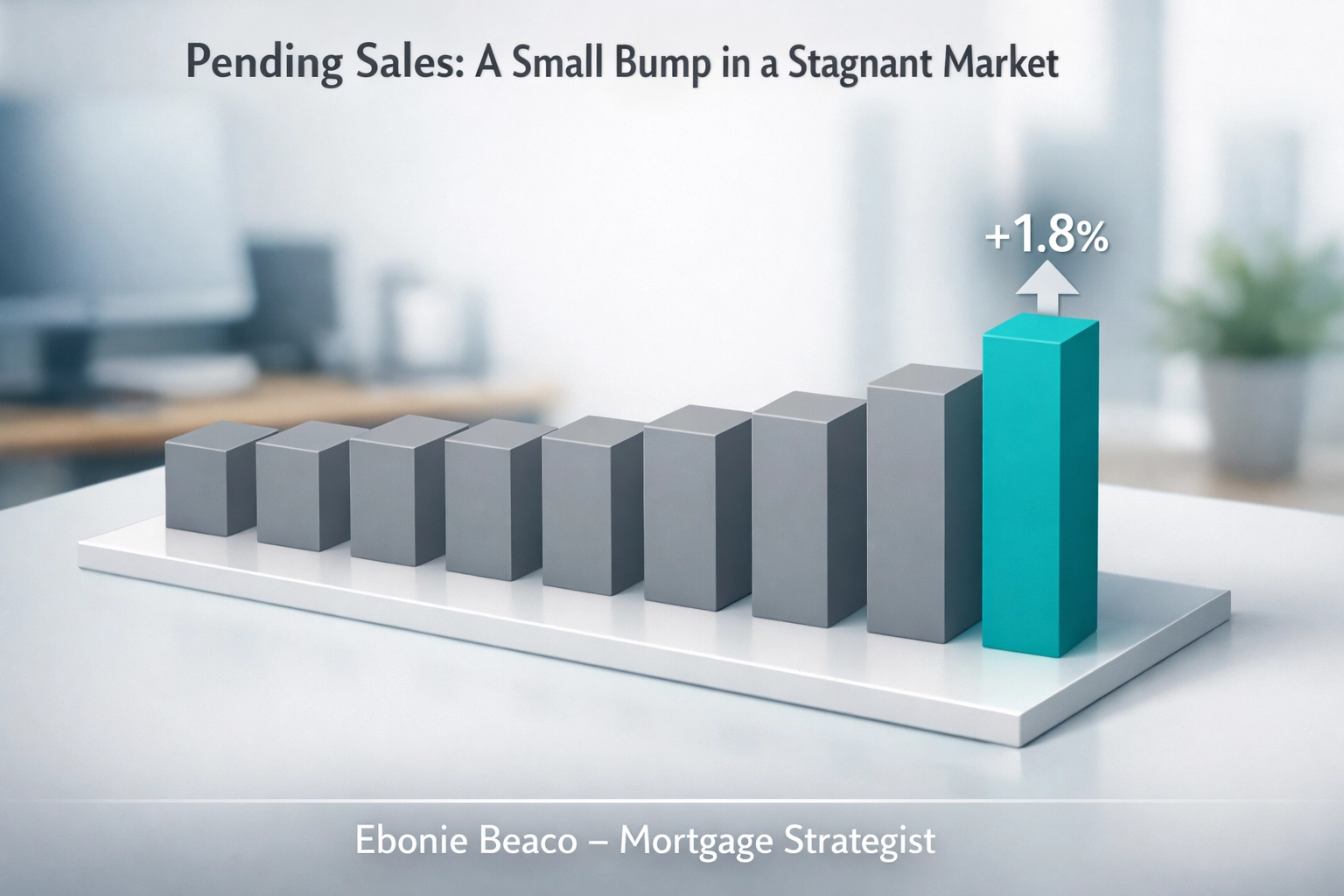

The housing market just gave us a little bit of a surprise, but before we break out the confetti, we should look at the full picture. According to the latest data, pending home sales across the United States saw a modest increase of 1.8% in February. On the surface, growth is always a welcome sign. However, when you zoom out, the market is still hovering near record lows, and recent shifts in mortgage rates are already creating new headwinds for the spring buying season.

As a mortgage strategist, I spend my days looking past the headlines to see how these numbers actually impact your ability to buy, sell, or invest in real estate. Whether you are looking for a primary residence in Chicago or building a rental portfolio in Florida, understanding the underlying mechanics of this stagnant market is essential for making your next move.

Breaking Down the February Numbers

A 1.8% month over month increase sounds like a recovery in the making. In reality, this "bump" is more of a minor correction from the lows we saw in January. If we compare where we are now to where we were this time last year, pending sales are actually down about 0.8%.

The primary driver for this February activity was a brief window where mortgage rates dipped, offering a sliver of affordability to buyers who had been waiting on the sidelines. According to industry reports, this gain was largely fueled by those temporary improvements in financing costs. You can find a deeper dive into these specific trends in this detailed report from Wolf Street, which highlights how the recent rate spike back over 6.3% is already threatening to stall this momentum.

Description: A chart showing the modest 1.8% uptick in pending home sales for February 2026 compared to the overall downward trend over the previous twelve months. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Description: A chart showing the modest 1.8% uptick in pending home sales for February 2026 compared to the overall downward trend over the previous twelve months. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Regional Performance: A Tale of Two Coasts

One of the most interesting parts of the current data is how fragmented the market has become. Real estate is rarely a singular national story; it is a collection of local stories.

In the Northeast, pending sales took a hit, declining by 3.6% in February. This region is struggling with a combination of high property values and a persistent lack of inventory. If you are looking at markets in Virginia or Michigan, you might see similar patterns where the volume of transactions is capped simply because there aren't enough homes for sale.

Conversely, the Midwest, South, and West all saw month over month growth. In places like San Diego, Jacksonville, and San Jose, we are seeing double digit annual gains in some sectors. For investors in states like Alabama, Georgia, and Indiana, this suggests that demand is still present, provided the financing structure makes sense for the property.

The Mortgage Rate Impact

The 1.8% gain in pending sales happened when rates were slightly lower. As we hit the middle of March 2026, those rates have spiked back over 6.3%. This volatility is the single largest factor keeping the market in a state of stagnation.

When rates jump, the "lock-in effect" intensifies. Homeowners who currently have a 3% or 4% mortgage rate are incredibly reluctant to sell their homes and trade up for a 6.3% rate. This keeps inventory levels low, which in turn keeps prices high. It is a cycle that requires a specific strategy to break.

For my clients, I often suggest looking at Non-QM Mortgage Loans or Bank Statement Loans. If you are self employed and the traditional "rate chase" is frustrating you, these programs allow us to qualify you based on your actual cash flow rather than just your tax returns.

Description: An infographic comparing mortgage rate volatility from January to March 2026, showing the impact on monthly purchasing power for a $400,000 loan. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Description: An infographic comparing mortgage rate volatility from January to March 2026, showing the impact on monthly purchasing power for a $400,000 loan. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Investment Strategies for a Tight Market

If you are a real estate investor, a stagnant market is actually a time of opportunity, provided you aren't relying on traditional retail financing. The "small bump" in sales shows that there is still life in the market, but the competition is less fierce than it was a few years ago.

DSCR Rental Property Loans

DSCR (Debt Service Coverage Ratio): A loan qualification method that uses the rental income of the property rather than the borrower’s personal income. Practical Application: Investors use this to scale their portfolios quickly without hitting debt-to-income (DTI) limits.

If you are looking at a multi-unit property in Chicago or a short-term rental in Florida, a DSCR loan is often the path of least resistance. We look at the property’s ability to pay for itself. If the rent covers the mortgage, taxes, and insurance, you are often good to go.

Cash-Out Refinance and HELOCs

Many homeowners in California and Virginia are sitting on record amounts of equity but don't want to sell. A HELOC (Home Equity Line of Credit) or a Cash-Out Refinance allows you to tap into that equity to fund your next investment.

Example Scenario: Imagine you own a home in Virginia valued at $600,000 with a current mortgage balance of $300,000.

- Property Value: $600,000

- Max LTV (80%): $480,000

- Existing Mortgage: $300,000

- Accessible Equity: $180,000

With $180,000 in hand, you could potentially put a 20% down payment on two or three more properties using DSCR financing.

Description: A deal breakdown graphic showing how a homeowner with $300,000 in equity can use a HELOC to secure down payments for multiple investment properties. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Description: A deal breakdown graphic showing how a homeowner with $300,000 in equity can use a HELOC to secure down payments for multiple investment properties. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Fix and Flip vs. Buy and Hold

In a stagnant market, the Fix and Flip model requires a very sharp pencil. Because pending sales are moving slowly, your "holding costs" (the interest you pay while the house is being renovated and listed) can eat into your profits.

For investors in Arkansas or Michigan, I am seeing more success with the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat). By focusing on the rental side, you aren't at the mercy of a slow retail buyer market. You can stabilize the property with a tenant and then move into a long-term Landlord Loan.

Financing the Short-Term Rental Market

Despite the stagnation in traditional home sales, the Airbnb and short-term rental market remains a focal point in Florida and Georgia. Financing these properties requires an understanding of "AirDNA" data and projected income. We offer specialized Airbnb and Short-Term Rental Financing that accounts for the unique income streams these properties generate.

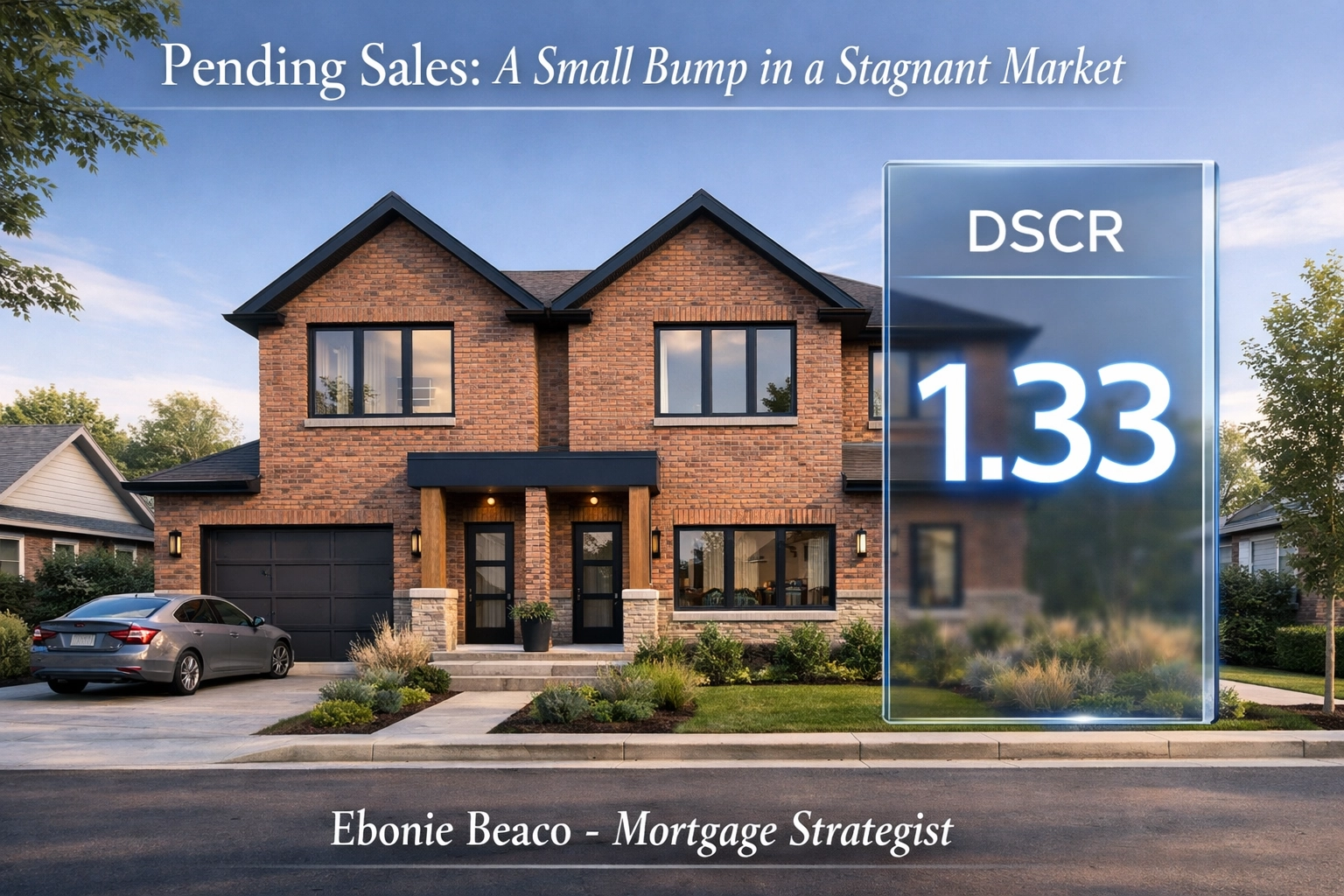

Understanding the DSCR Calculation

For those new to investing, let’s look at a quick calculation. If you are eyeing a duplex in Indiana:

- Monthly Rent (Unit 1 + Unit 2): $2,800

- Monthly Mortgage Payment (Principal, Interest, Taxes, Insurance, Association): $2,100

- Calculation: $2,800 / $2,100 = 1.33 DSCR

A DSCR of 1.33 is typically considered very strong. Most lenders look for a ratio of 1.20 or higher. This means the property generates 20% more income than the cost to carry the debt.

Description: A professional financial chart displaying a DSCR calculation for a $350,000 duplex with a 1.33 ratio. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Description: A professional financial chart displaying a DSCR calculation for a $350,000 duplex with a 1.33 ratio. Title: Pending Sales: A Small Bump in a Stagnant Market. Bottom text: Ebonie Beaco - Mortgage Strategist.

Why Transparency is the Key

At Home Loans Network, we believe in being transparent about the challenges of the current market. A 1.8% rise in pending sales is better than a 1.8% drop, but we aren't out of the woods yet. The importance of having a clear strategy cannot be overstated.

When inventory is low and rates are volatile, your financing needs to be "bulletproof" before you ever make an offer. This means having your documents ready, understanding your PMI (Private Mortgage Insurance) implications if you are putting down less than 20%, and knowing your DTI (Debt-to-Income) limits.

How to Navigate the Stagnation

If you are a buyer or an investor, don't let the "stagnant" label discourage you. A stagnant market often means less competition from emotional buyers and more room for professional negotiation.

Jump in and explore your options today. Whether it is a Bridge Loan to help you buy before you sell, or an ITIN Mortgage Loan for those with unique residency status, there is almost always a path forward.

Compare the costs of waiting versus the costs of acting now. With rates hovering above 6.3%, waiting for a "crash" that may never come due to low inventory could cost you more in the long run.

Access the equity you’ve built over the last few years. If you’ve seen your home value skyrocket in Florida or Illinois, that equity is a tool waiting to be used.

The housing market is currently in a tug-of-war between low inventory and high rates. The February bump shows that buyers are ready to move as soon as they see a window of opportunity. My job is to help you find that window and give you the financial tools to climb through it.

Explore our mortgage basics or book an appointment to discuss your specific scenario.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664