No Income Verification Investor Loans

Traditional mortgage lending often feels like a deep dive into your personal history that never seems to end. For the average homebuyer, providing two years of tax returns and W2s is a standard part of the process. However, for real estate investors in markets like Chicago, Miami, or Atlanta, these requirements often create massive roadblocks.

No Income Verification Investor Loans are designed to bypass the hurdles of personal income documentation. Instead of looking at what you earn at a job, lenders look at what the property earns in rent. This strategy allows investors to scale their portfolios without the constraints of debt-to-income ratios based on personal tax filings.

At Home Loans Network, we focus on transparency. We want you to understand exactly how these programs function so you can determine if they fit your current investment strategy. Whether you are looking at a fix and flip in Virginia or a long-term rental in Michigan, this financing path offers a streamlined alternative to traditional banking.

What is a No Income Verification Investor Loan?

No Income Verification Investor Loan: A mortgage product that qualifies a borrower based on the cash flow of the subject property rather than personal income documents like tax returns or pay stubs.

This means you do not have to provide W2s or proof of employment. The lender is primarily concerned with the property’s ability to pay for itself. In the industry, we often refer to these as DSCR loans.

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments by comparing its annual net operating income to its annual debt service.

If the rental income exceeds the mortgage payment, the property is considered a strong candidate for financing. This shift in focus from the person to the asset is a game-changer for entrepreneurs and full-time investors.

Why Investors Choose No Income Verification Options

Many of the most successful investors in Florida and California do not have a "standard" income. Their wealth is tied up in assets, or their tax returns show heavy deductions that make their taxable income look lower than it actually is.

If you are self-employed, your tax professional likely works hard to minimize your tax liability. While this is great for your bank account in April, it can be a nightmare when applying for a conventional loan. Traditional underwriters look at the "bottom line" on your tax returns, which might not reflect your true buying power.

By using a No Income Verification Investor Loan, you can ignore those tax return figures entirely. You can explore our loan programs to see how these fit into a broader acquisition strategy. This flexibility is why these loans are a staple for those building large rental portfolios in high-growth areas like Georgia or Indiana.

The Power of the DSCR Calculation

The heart of this loan program is the calculation. Lenders want to see a specific ratio to feel confident in the loan. Usually, a ratio of 1.0 or higher is the target. This means the gross rent equals the monthly debt (principal, interest, taxes, insurance, and HOA fees).

Let’s look at a practical example. Imagine you are eyeing a duplex in Indianapolis.

Example Scenario: The Indy Duplex

- Purchase Price: $350,000

- Down Payment (20%): $70,000

- Loan Amount: $280,000

- Estimated Monthly Payment (PITI): $2,100

- Gross Monthly Rent: $2,800

- DSCR Calculation: $2,800 / $2,100 = 1.33

In this case, the ratio is 1.33. Since the income covers the debt with a healthy cushion, the loan is highly likely to be approved without a single glance at your personal paycheck.

Image Description: A clean financial breakdown graphic showing the "Indy Duplex" scenario. It displays the Gross Rent of $2,800 divided by the Debt Service of $2,100, resulting in a DSCR of 1.33. The title "DSCR Calculation Example" is visible at the top. Footer: Ebonie Beaco - Mortgage Strategist.

Eligibility and Requirements

While you do not need to show income, you still need to meet certain criteria. Lenders are taking on risk by not verifying your personal earnings, so they balance that risk in other areas.

Credit Score Thresholds

Most programs require a minimum credit score. Typically, you want to see a score of 660 or higher to get the best terms. Some specialized programs might go lower, but 700+ is the sweet spot for lower interest rates.

Down Payment Standards

You should expect to put more skin in the game. While a primary residence might only require 3% or 5% down, investor loans usually require 20% to 25% down. This equity protects the lender if the market shifts.

Property Type Flexibility

These loans are versatile. You can use them for:

- Single-family homes

- 2-4 unit residential properties

- Condos and townhomes

- Short-term rentals (Airbnb or VRBO)

If you are looking at larger projects, you might want to look into commercial real estate loans for 5+ unit buildings.

Speed and Efficiency in Competitive Markets

In fast-moving markets like Northern Virginia or the suburbs of Chicago, speed is everything. Sellers often prefer offers with quick closing timelines. Because No Income Verification loans skip the tedious process of auditing tax returns and employment history, they often close faster than conventional loans.

The loan process becomes much more predictable. Once the appraisal is back and the rent schedule is confirmed, the path to the closing table is usually clear. This transparency helps you build a reputation with realtors as an investor who can actually perform.

Scaling with the BRRRR Strategy

The BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) relies on the ability to pull equity out of a property once it is renovated and rented. No Income Verification loans are perfect for the "Refinance" step of this cycle.

Once you have a tenant in place and a lease signed, that lease becomes the documentation used to qualify for the new loan. You can use a cash-out refinance to recoup your initial investment and moving onto the next property.

This cycle is how investors in Alabama and Arkansas are rapidly expanding their holdings. They are not limited by their personal income; they are only limited by the number of cash-flowing deals they can find.

Short-Term Rental Potential

If you are investing in vacation hubs in Florida or Kentucky, you might be looking at short-term rentals. Many No Income Verification programs now allow the use of "AirDNA" data or historical short-term rental income to qualify.

This is a massive advantage. Often, a property functions much better as a vacation rental than a long-term rental. If the lender recognizes that higher income potential, your DSCR ratio improves, and your financing options expand. You can learn more about these specifics in our mortgage basics section.

Common Myths About Investor Loans

Some people believe that "No Income Verification" means "No Credit Check" or "No Assets Required." That is not the case. You still need to show that you have the funds for the down payment and some reserves (usually 3 to 6 months of payments) in the bank.

Another myth is that these loans carry astronomical interest rates. While the rates are slightly higher than a traditional owner-occupied loan, they are very competitive when you consider the tax benefits and the ability to scale. Transparency in pricing is something we prioritize so you can accurately calculate your ROI.

Working with an Expert Strategist

Navigating the world of Non-QM and investor lending requires a specific set of tools. It is not just about finding a loan; it is about finding the right structure for your business. Whether you are closing in your personal name or through an LLC, the way you frame the deal matters.

If you have questions about a specific property in Missouri or any of our service states, it helps to see the numbers laid out clearly. You can check our FAQ for quick answers to common lending hurdles.

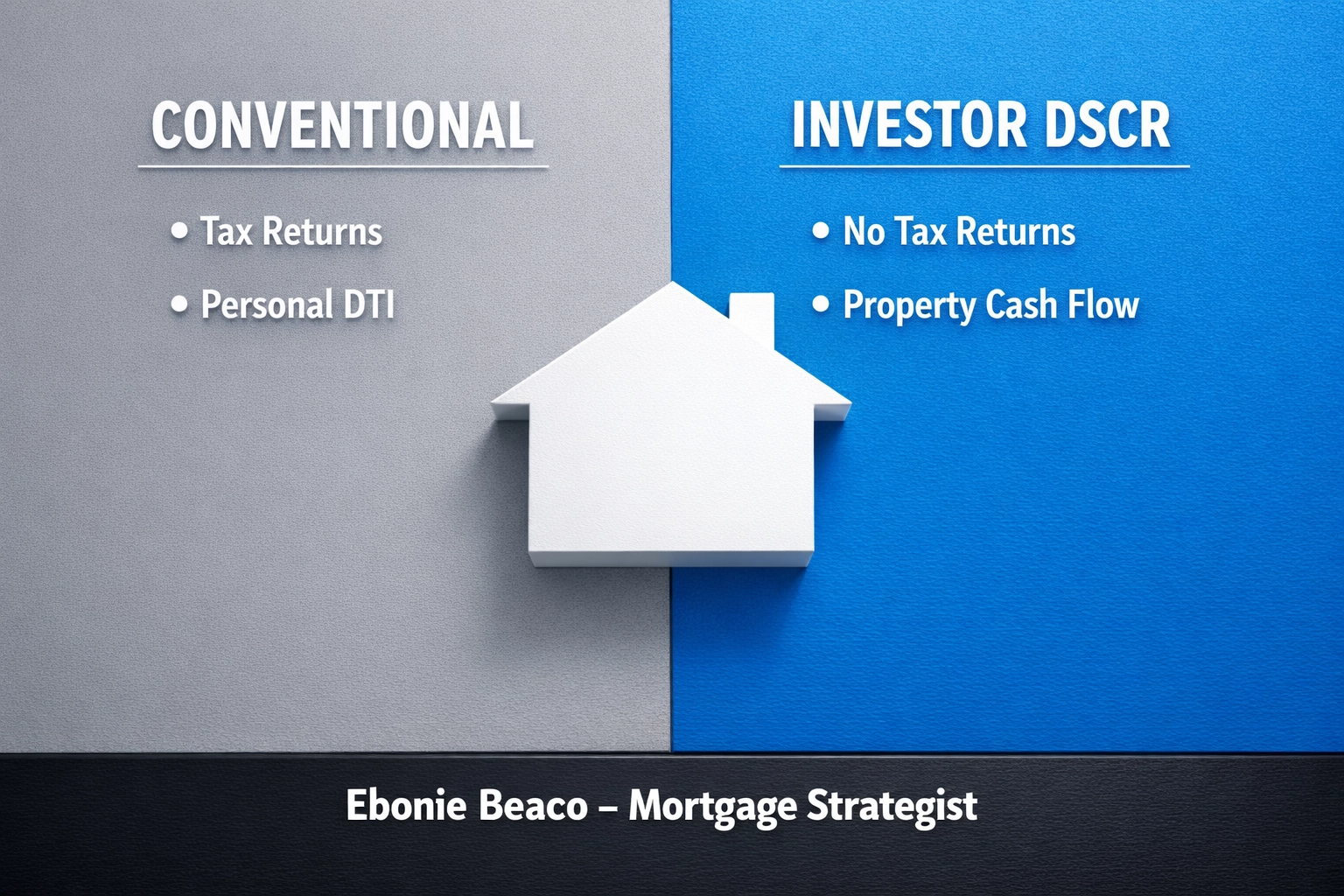

Image Description: A professional comparison chart titled "Conventional vs. Investor DSCR Loans." It compares columns for Documentation, Qualification Basis, and Speed. Under Conventional, it lists "Tax Returns/W2s" and "Personal DTI." Under Investor DSCR, it lists "No Tax Returns" and "Property Cash Flow." Footer: Ebonie Beaco - Mortgage Strategist.

Taking the Next Step in Your Investment Journey

The housing market is constantly changing, but the need for creative financing remains constant. No Income Verification Investor Loans provide the bridge between where you are and where you want your portfolio to be.

Don't let a complex tax return stop you from acquiring your next rental property. Focus on the asset, run the numbers, and use the leverage available to you. If you are ready to see what a DSCR loan can do for your specific scenario, we are here to provide the guidance you need.

Explore your options and get a clear picture of your buying power today. Use our mortgage calculators to run your own preliminary numbers and see how a potential property stacks up.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664