Navigating Today’s Rate Volatility: How to Protect Your Buying Power Before Tomorrow

The mortgage landscape in early June 2026 continues to present a dynamic environment for homebuyers and seasoned investors alike. As of this week, the average 30-year fixed mortgage rate is hovering in the mid-6% range, specifically between 6.3% and 6.6% according to recent market indices. This stability, while a welcome departure from the extreme peaks of previous years, still carries a level of daily volatility that can shift your monthly budget within a single afternoon. Understanding these movements is essential for anyone looking to secure a property in high-demand regions like Florida, Georgia, or California. By staying informed on the underlying economic drivers, you can position yourself to act decisively before the next upward tick in financing costs.

Defining Key Financial Terms

Interest Rate Volatility: The frequency and magnitude of changes in interest rates over a short period. In today's market, volatility is often triggered by inflation reports, Federal Reserve commentary, or shifts in the 10-year Treasury yield.

Buying Power: The total amount of home you can afford based on your income, down payment, and current interest rates. When rates rise, your buying power decreases because a larger portion of your monthly payment is dedicated to interest rather than the principal balance.

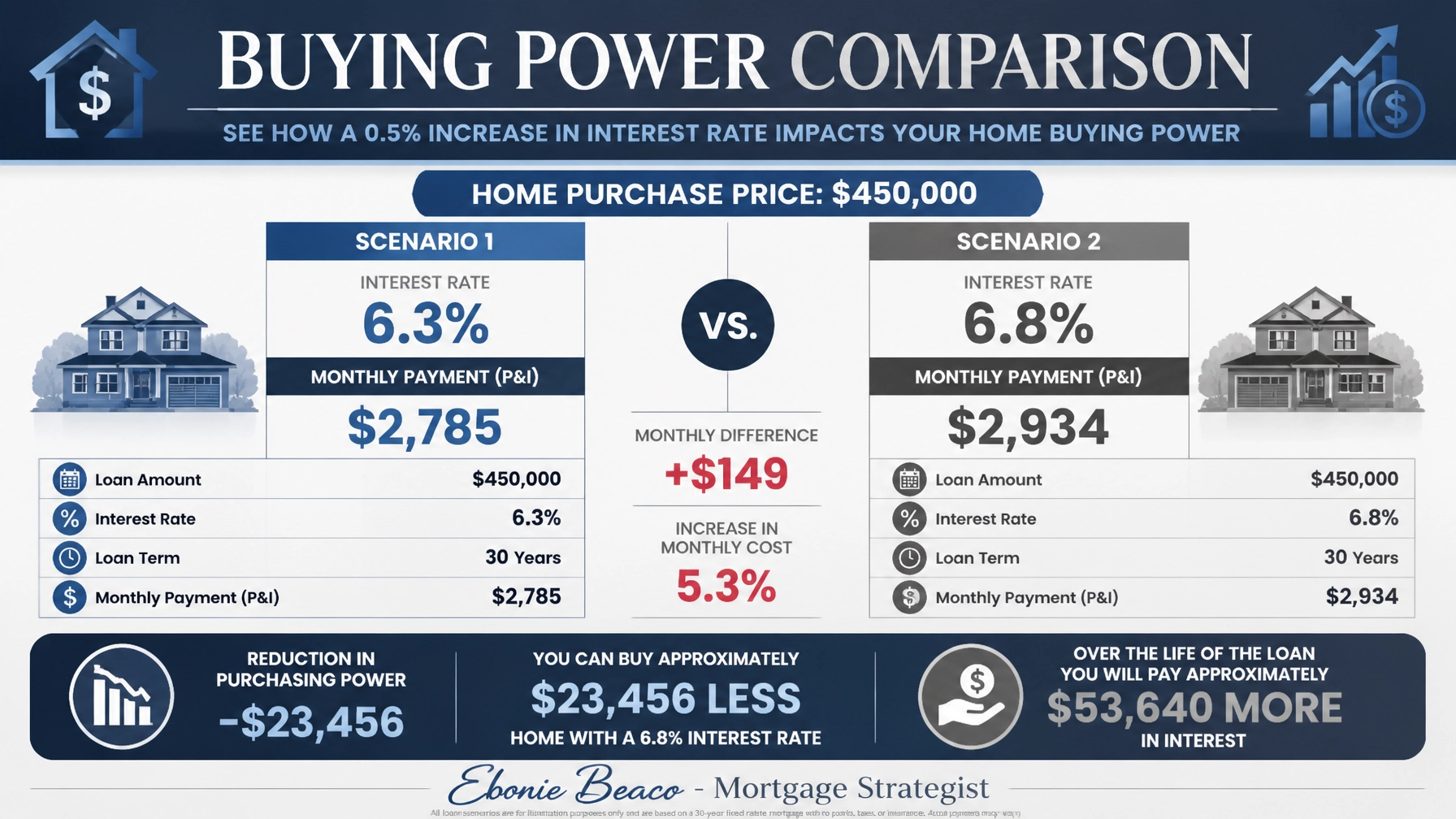

The Impact of a Half-Point Shift on Your Budget

Even a seemingly minor change of 0.5% in your interest rate can have a profound effect on your long-term financial obligations. For instance, consider a homebuyer in the Chicago suburbs or Northern Virginia looking at a $450,000 property with a 20% down payment. At a 6.3% interest rate, the principal and interest payment sits at approximately $2,228 per month. However, if the market experiences a sudden shift and that rate climbs to 6.8%, the payment jumps to $2,347. This $119 monthly difference adds up to over $42,000 in additional interest costs over the life of a 30-year loan, effectively reducing the price point you can comfortably target today.

Strategic Solutions for Current Homeowners

For those who already own property in states like Michigan, Indiana, or Missouri, the current market offers unique opportunities to leverage existing equity. Despite the broader rate environment, many homeowners have seen significant appreciation in their property values over the last several years. Accessing this wealth through a Cash-Out Refinance or a HELOC (Home Equity Line of Credit) can provide the capital needed for home renovations or secondary investments. These strategies allow you to consolidate higher-interest debt or fund new ventures without waiting for rates to return to historic lows. It is often more advantageous to secure a fixed-rate solution now than to risk being subject to further volatility later in the year.

Mortgage Solution Definitions

HELOC (Home Equity Line of Credit): A revolving line of credit that allows homeowners to borrow against the equity in their home as needed. This is a versatile tool for funding home improvements or managing large expenses while keeping your primary mortgage intact.

Cash-Out Refinance: Replacing your existing mortgage with a new, larger loan and taking the difference in cash. This strategy is frequently used by investors to pull capital out of one property to fund the purchase of another.

Empowering Real Estate Investors with DSCR Loans

Real estate investors active in the Florida or Atlanta markets are increasingly turning to specialized financing to scale their portfolios. DSCR (Debt Service Coverage Ratio) Loans remain a cornerstone for landlords because they focus on the property's income potential rather than the borrower’s personal income. In a mid-6% rate environment, calculating the profitability of a rental unit becomes even more critical for long-term success. You can explore how these loans facilitate the acquisition of single-family rentals or small multi-unit buildings without the intensive documentation required by traditional banks. This focus on property performance allows you to maintain momentum in your investment journey regardless of personal tax returns or debt-to-income ratios.

Professional Investor Terminology

DSCR (Debt Service Coverage Ratio): A metric used by lenders to determine if a property’s rental income can cover its debt obligations. A ratio above 1.0 indicates that the property generates enough cash flow to pay its own mortgage, making it an attractive prospect for specialized investor financing.

Non-QM (Non-Qualified Mortgage): A loan that does not meet the standard criteria of government-backed agencies. These programs are designed for self-employed individuals, ITIN borrowers, and those with complex financial profiles who need flexible qualification pathways.

Leveraging Home Equity for Portfolio Growth

The concept of "equity mining" is becoming a standard practice for sophisticated investors in Alabama, Arkansas, and Kentucky. By analyzing your current real estate holdings, you can identify underutilized equity that could be deployed into high-yield opportunities like short-term rentals or fix-and-flip projects. Utilizing Bridge Loans or Hard Money Loans provides the speed necessary to compete in markets where inventory remains tight. These short-term financing options bridge the gap between acquisition and permanent financing, giving you the flexibility to renovate and increase property value. Taking action today ensures you have the liquid capital ready to seize deals that appear as the market moves toward a more balanced state.

Advanced Financing Concepts

Bridge Loan: A short-term loan intended to provide immediate cash flow while permanent financing is being arranged. It is an essential tool for investors who need to close quickly on a property before selling another asset.

Fix-and-Flip Financing: Short-term funding specifically designed for purchasing and renovating distressed properties for a quick resale. This type of loan typically covers both the purchase price and the cost of repairs.

Looking Ahead: Market Forecasts and Your Next Move

Economic experts from organizations like Bankrate and Fannie Mae suggest that while rates may dip slightly toward the end of 2026, the current mid-6% range is likely to persist through the summer. Waiting for a significant drop in rates often means competing with a larger pool of buyers, which can drive home prices higher and negate any potential savings. In states like Virginia and California, where price growth remains steady, entering the market now allows you to start building equity immediately. You should focus on finding a property that fits your long-term goals and a financing structure that protects your monthly cash flow. Comparing different loan products, from conventional options to bank statement loans, ensures you are not leaving money on the table.

Navigating the complexities of today's mortgage market requires a proactive and strategic approach. Whether you are a first-time homebuyer or a seasoned landlord, the right financing can turn a fluctuating market into a period of significant growth. Explore your options clearly and confidently to ensure your purchasing power remains protected. If you are ready to evaluate a specific scenario or need guidance on which program fits your profile, reach out for a personalized consultation. Jump in today to secure your financial future in the ever-evolving real estate landscape.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664