Navigating Today’s Rate Volatility: How Federal Updates Influence Florida and Georgia Investment Strategies

The mortgage landscape in June 2026 presents a complex environment for homeowners and real estate investors alike. As the Federal Reserve maintains a cautious stance on monetary policy, market participants in high-growth states like Florida and Georgia are closely monitoring how these decisions influence borrowing costs. Understanding the interplay between federal interest rate benchmarks and local property values is essential for making informed acquisition or refinancing decisions. Current data suggests a period of relative stability in policy rates, yet mortgage market volatility remains a persistent factor for those looking to lock in financing.

Exploring the nuances of the current economy requires a clear view of the Federal Open Market Committee (FOMC) actions and their ripple effects throughout the lending industry. While the central bank does not directly set mortgage rates, its influence over the 10-year Treasury yield and investor sentiment often dictates the direction of conforming and non-QM loan pricing. For individuals navigating the competitive markets of the Sun Belt, staying ahead of these shifts is the first step toward securing a sustainable financial future in real estate.

Understanding Recent Federal Reserve Communications

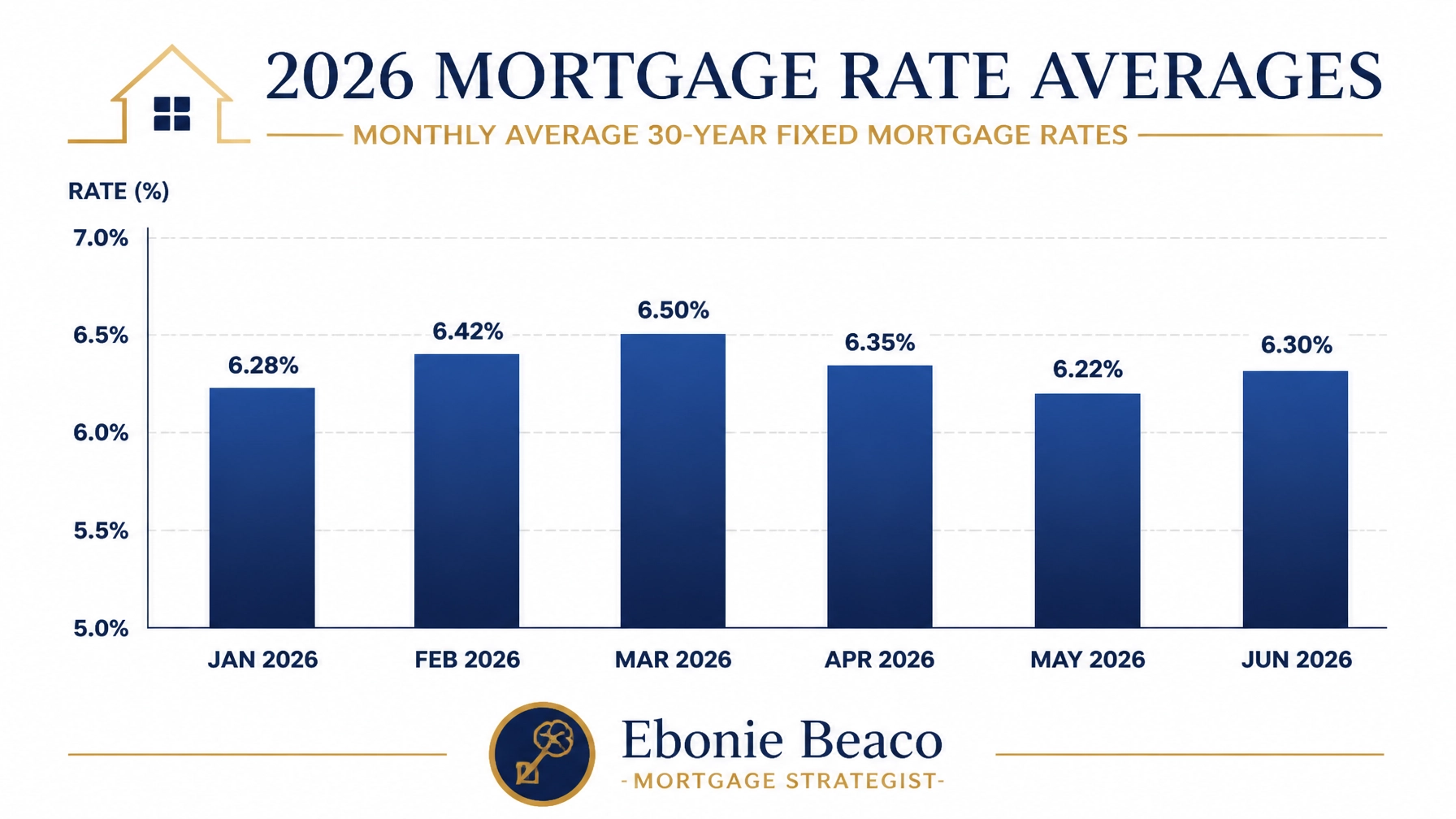

The Federal Reserve has recently opted to maintain the federal funds target range at 3.50% to 3.75%, signaling a period of observation rather than aggressive movement. This "pause" follows several adjustments aimed at balancing inflation control with economic growth across the United States. Investors and lenders interpret these signals to gauge the long-term outlook for liquidity and credit availability. As of early June 2026, the consensus among financial analysts is that rates may remain at these elevated levels for the foreseeable future, making current quotes more representative of the new "normal" in mortgage lending.

Federal Reserve Policy: The strategic management of the nation's money supply and interest rates by the central bank to achieve maximum employment and stable prices. In practical terms, these policies determine how expensive it is for you to borrow money for a home purchase or a commercial property acquisition.

Jump in and evaluate how these federal shifts impact your specific portfolio. When the Fed holds steady, it often leads to a "wait and see" approach from both buyers and sellers, which can lead to increased inventory in certain submarkets. However, for those with ready capital or specialized financing needs, this environment can also reveal opportunities to negotiate better terms with sellers who are eager to close before any further volatility occurs. You can review more about how these processes work on our loan process page.

The Impact on Florida’s Real Estate Market

Florida continues to be a primary destination for both primary residents and seasoned real estate investors due to its favorable climate and lack of state income tax. However, the current rate environment, combined with rising homeowners' insurance premiums, has shifted the traditional investment calculus in regions like Miami, Tampa, and Orlando. High mortgage rates increase the monthly debt service, which means property appreciation and rental income must work harder to provide a positive return on investment.

Despite these challenges, demand remains resilient in Florida’s coastal hubs and rapidly growing inland cities. You will find that many investors are moving away from traditional conventional loans and exploring more flexible options that account for the unique market conditions in the state. Short-term rentals and high-end condo developments continue to attract capital, particularly from buyers who can leverage equity from properties in higher-priced markets like California or Virginia.

Florida Real Estate Investment: The act of purchasing property in Florida for the purpose of generating income or realizing capital gains. For you, this means carefully analyzing the total carrying cost, including taxes and insurance, to ensure that the financing structure aligns with your cash flow goals.

Georgia’s Investment Landscape in a Shifting Rate Environment

Georgia, particularly the Atlanta metropolitan area, offers a different set of opportunities compared to its southern neighbor. The state’s diverse economy and steady population growth provide a robust foundation for rental property demand. In a mid-6% interest rate environment, Georgia investors often focus on value-add opportunities where they can increase equity through renovations and subsequent rent hikes.

Atlanta Market Dynamics: The specific economic and social factors that influence property supply, demand, and pricing within the Atlanta region. This concept helps you understand why some neighborhoods may see rapid price growth while others remain stable, even when national interest rates are high.

Compare the various loan programs available to see which fits the Georgia market best for your needs. Many landlords in cities like Savannah and Augusta are utilizing bridge loans to secure properties quickly, then transitioning into long-term financing once renovations are complete. This strategy allows you to capitalize on the state’s growth while navigating the volatility of the current mortgage market.

Strategic Financing: DSCR and Cash-Out Refinance

For the real estate investor, the Debt Service Coverage Ratio (DSCR) loan has become a vital tool in today's market. Unlike traditional mortgages that rely heavily on personal income and debt-to-income (DTI) ratios, DSCR loans focus on the cash flow generated by the property itself. This is particularly beneficial in a higher-rate environment where personal DTI might be stretched, but a high-performing rental property can still justify its own financing.

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments using its own rental income. This allows you to qualify for financing based on the property’s performance rather than your personal tax returns or W-2 income.

Consider an example of an investor purchasing a duplex in a growing Georgia suburb. By focusing on the property's potential, you can bypass the rigorous documentation required for traditional loans. This approach is common among self-employed borrowers and professional landlords looking to scale their portfolios across multiple states including Alabama, Arkansas, and Michigan.

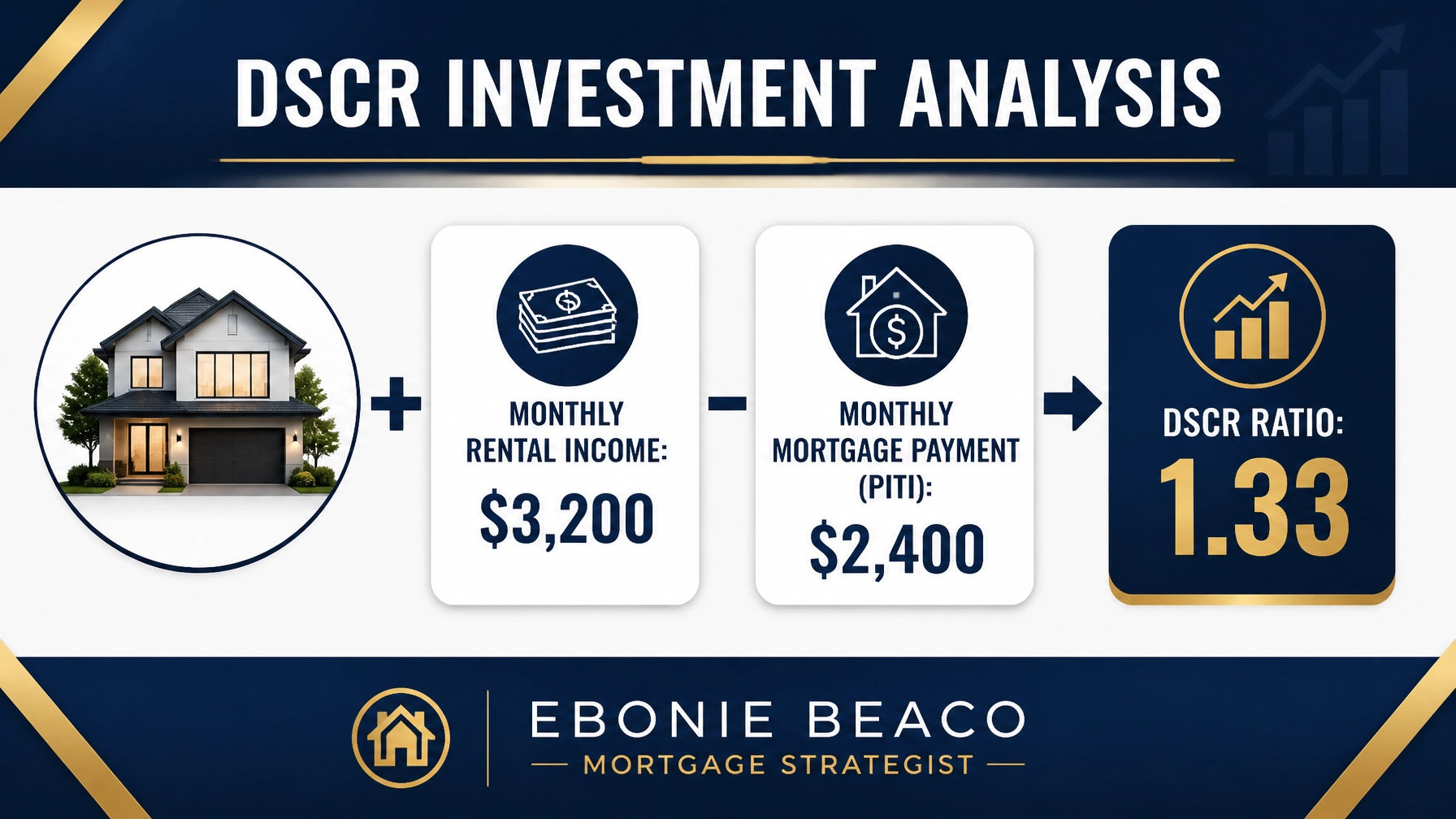

Real-World Financial Example: DSCR Calculation

To illustrate how this works in practice, let’s look at a scenario for a rental property acquisition. Imagine you are eyeing a single-family home in a desirable neighborhood with a purchase price of $450,000. Under current lending guidelines, you might secure a DSCR loan with a 25% down payment, leaving a loan amount of $337,500. At a mid-6% interest rate, your estimated monthly payment for Principal, Interest, Taxes, and Insurance (PITI) might be $2,400.

If the market rent for this property is $3,200 per month, the calculation is straightforward. You divide the monthly rent by the monthly PITI to find your ratio. In this case, $3,200 divided by $2,400 equals a DSCR of 1.33. Most lenders look for a ratio above 1.20, meaning this property would easily qualify for financing, allowing you to build wealth through real estate even when federal updates keep rates elevated.

Accessing Equity: HELOC and Cash-Out Strategies

Homeowners in Florida and Georgia who have seen significant property appreciation over the last few years may find themselves "equity rich" but "cash poor." A cash-out refinance or a Home Equity Line of Credit (HELOC) can be a powerful way to unlock that value for further investment or property improvements. While today's rates might be higher than the rate on your existing mortgage, the ability to access $100,000 or $200,000 in liquid capital can often outweigh the cost of a higher interest rate, especially if those funds are used to purchase a high-yield investment property.

Cash-Out Refinance: A mortgage restructuring that allows you to replace your current loan with a larger one, taking the difference in cash. This provides you with immediate liquidity that can be used for debt consolidation, home renovations, or new real estate investments.

Explore your options by checking our FAQ page for more details on how equity products work. Many investors use a "buy, rehab, rent, refinance, repeat" (BRRRR) strategy, which relies heavily on the ability to pull equity out once a property has been improved. This allows you to recycle your capital and grow your holdings more rapidly than if you were relying solely on personal savings.

The Outlook for the Remainder of 2026

As we look toward the second half of 2026, the theme remains one of strategic adaptation. Forecasters from major financial institutions like Fannie Mae and the Mortgage Bankers Association suggest that rates will likely hover in the 6.0% to 6.5% range for the remainder of the year. This suggests that waiting for a significant drop in rates may lead to missed opportunities in terms of property selection and price negotiation.

Access the latest market insights and expert guidance to help you navigate these fluctuations. Whether you are a first-time homebuyer in Virginia, a landlord in Indiana, or a developer in Illinois, the key to success is aligning your financing with your long-term wealth-building goals. Education and transparency are the cornerstones of a successful real estate journey, and understanding the federal influences on your local market is a major part of that process.

You are encouraged to resolve any uncertainty by speaking with a professional who understands the nuances of the 2026 mortgage market. By focusing on the fundamentals: cash flow, equity, and strategic financing: you can continue to thrive in any rate environment.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664