Multi-Family Loans (2–4 Units Residential)

Post Description

Looking to break into real estate investing without needing a massive corporate bankroll? Multi-family loans for 2–4 unit residential properties are a game-changer for both new and seasoned investors. Whether you are looking at a duplex in Chicago, a triplex in Indianapolis, or a fourplex in Tampa, these loans allow you to qualify for a residential mortgage while generating rental income from day one. By living in one unit and renting out the others, a strategy known as house hacking, you can significantly offset or even eliminate your monthly mortgage payment. These programs offer lower down payment options compared to larger commercial projects, making property ownership more accessible. At Home Loans Network, we believe in providing a clear path to building your portfolio with transparency.

Ready to see how the numbers look for your next multi-unit purchase?

Schedule a 1-on-1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Understanding Multi-Family Loans (2–4 Units)

When you step into the world of residential real estate, most people think of the standard single-family home. However, savvy investors and proactive homebuyers often look toward small multi-family properties. These are buildings that contain two, three, or four separate housing units.

In the eyes of the lending world, a property with 1 to 4 units is considered "residential." This classification is vital because it allows you to access residential loan products, which typically have lower interest rates and more flexible down payment requirements than commercial loans for 5+ unit buildings.

Whether you are a first-time buyer in Virginia or an experienced landlord in Florida, understanding how to leverage these 2–4 unit properties can accelerate your path to financial independence. You can explore our mortgage basics to get a foundational understanding of how these structures differ from traditional loans.

Why 2–4 Unit Properties Are Popular

Multi-family properties offer a unique blend of residential comfort and investment potential. For a buyer in markets like Michigan or Alabama, purchasing a duplex might cost only slightly more than a large single-family home, but the financial upside is significantly higher.

House Hacking: This is the practice of living in one unit of your multi-family property while renting out the others. The rent collected from your tenants covers a large portion, if not all, of your mortgage, taxes, and insurance.

Scale: It is often easier to manage four units under one roof than four separate houses scattered across a city like Chicago or Los Angeles. You only have one roof to maintain, one yard to mow, and one foundation to monitor.

Simplified Financing: Because these are still "residential" properties, you do not have to deal with the complex requirements of commercial lending. You can use standard loan programs that you are likely already familiar with.

Visual: A comparison chart showing the differences between Single Family, Duplex, Triplex, and Fourplex properties. Footer: Ebonie Beaco - Mortgage Strategist. Title: Multi-Family Property Classifications.

Core Loan Programs for Multi-Family Properties

Choosing the right loan program depends on your goals, your credit profile, and whether you intend to live in the property.

FHA Loans (Federal Housing Administration)

FHA loans are a favorite for multi-family buyers because they allow for a down payment as low as 3.5%. This is a massive advantage when buying a fourplex that might cost $600,000. Instead of needing 20% down ($120,000), an FHA borrower only needs $21,000.

Self-Sufficiency Test: For 3–4 unit properties, the FHA requires the property to pass a "self-sufficiency test." This means the projected net rental income from all units must be enough to cover the total mortgage payment (Principal, Interest, Taxes, and Insurance). This ensures the property is a sound investment.

Conventional Loans

Fannie Mae and Freddie Mac offer conventional financing for 2–4 unit properties. Recently, guidelines changed to allow for much lower down payments on multi-family homes even for conventional products, making them highly competitive with FHA loans for those with stronger credit scores. You can check out more on the home purchase page to see current conventional trends.

VA Loans (Veterans Affairs)

If you are a veteran or active-duty service member, the VA loan is perhaps the most powerful tool in real estate. You can buy up to a 4-unit property with $0 down payment. This allows veterans in states like Georgia or Kentucky to become landlords with almost no upfront capital, provided they occupy one of the units.

DSCR Loans (Debt Service Coverage Ratio)

If you do not plan on living in the property and want to buy it purely as an investment, a DSCR loan might be the best fit. These loans qualify you based on the property’s ability to generate rent, rather than your personal income or tax returns. This is ideal for self-employed borrowers or investors with complex tax situations.

Qualification Requirements

Lenders look at a few specific metrics when you apply for a multi-family loan. While each program has its nuances, the following factors are almost always present.

Credit Score: For FHA, you typically need a minimum score of 580. For conventional multi-family loans, a score of 620 or higher is usually preferred to get the best terms.

Debt-to-Income (DTI) Ratio: Lenders look at how much of your monthly income goes toward debt. The great news with 2–4 unit properties is that you can often use 75% of the projected rental income from the other units to help you qualify. This can "boost" your income and help you qualify for a larger loan than you could for a single-family home.

Owner Occupancy: To get the best rates and lowest down payments, you usually must commit to living in one of the units for at least one year. If you are strictly an investor, expect to put down 20% to 25%.

Cash Reserves: Multi-family properties come with more responsibility. Lenders often want to see that you have a few months of mortgage payments tucked away in savings to cover potential vacancies or repairs.

Visual: A checklist of qualification requirements: Credit Score, DTI, Reserves, and Occupancy Status. Footer: Ebonie Beaco - Mortgage Strategist. Title: Multi-Family Loan Qualification Checklist.

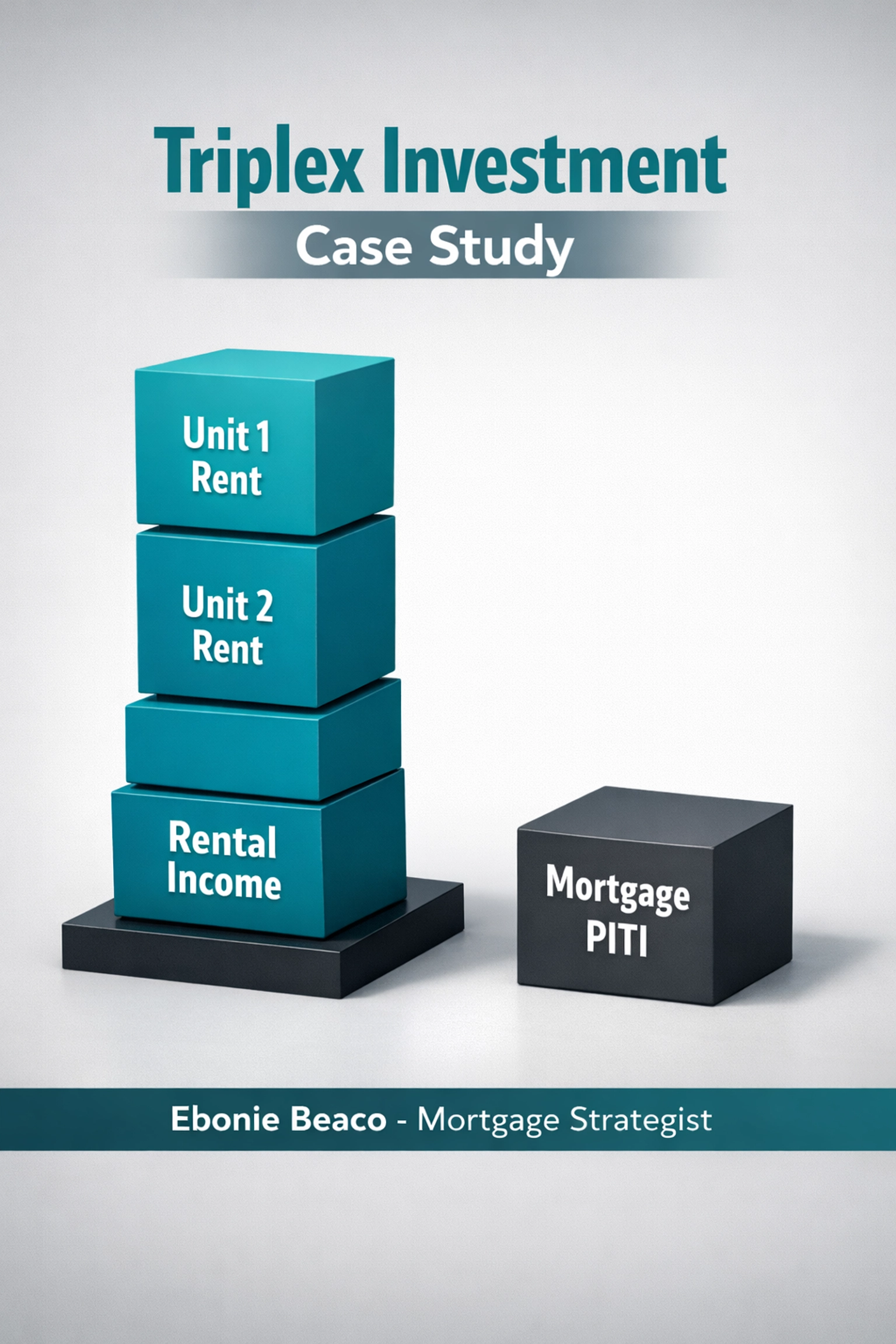

The Financial Impact: A Real-World Example

Let’s look at a scenario for an investor purchasing a triplex in a market like Indianapolis or a suburb of Atlanta.

The Deal:

- Purchase Price: $450,000

- Loan Type: FHA (3.5% Down)

- Down Payment: $15,750

- Monthly Mortgage Payment (PITI): $3,400

The Income:

- Unit 1: Owner-occupied ($0 rent)

- Unit 2 Rent: $1,500

- Unit 3 Rent: $1,500

- Total Monthly Rental Income: $3,000

The Result:

In this scenario, the owner is collecting $3,000 in rent from their neighbors. Their total mortgage is $3,400. This means their "out of pocket" cost to live in a $450,000 property is only $400 per month. If they were renting a similar apartment elsewhere, they might be paying $1,800 or more.

By living here, they are saving $1,400 a month while their tenants pay down the mortgage and the property potentially appreciates in value. This is the transparency we aim for at Home Loans Network, showing you exactly how the numbers can work in your favor. You can run your own scenarios using our mortgage calculators.

Visual: A financial breakdown chart of the Triplex example. Showing Purchase Price, Down Payment, Rental Income vs. Mortgage Payment. Footer: Ebonie Beaco - Mortgage Strategist. Title: Triplex Investment Case Study.

Geography and Market Dynamics

The strategy for 2–4 unit properties varies by region.

- Chicago, IL: Known for its classic "two-flats" and "three-flats," Chicago is a premier market for multi-family lending. Many neighborhoods are built specifically with this density in mind, making inventory easier to find.

- Florida and California: In high-demand coastal states, multi-family properties are excellent hedges against rising housing costs. While the entry price is higher, the rental demand is consistently strong.

- Virginia and Georgia: These states offer a mix of urban multi-family options and suburban clusters. They are popular for those looking to balance cash flow with long-term appreciation.

Regardless of where you are looking, the loan process remains straightforward when you have a clear strategy in place.

Frequently Asked Questions

Can I use a multi-family loan for a 5-unit building?

No. Once a property hits 5 units, it is classified as commercial real estate. Financing for those buildings follows different rules, often requiring higher down payments and shorter loan terms.

Do I have to be a first-time homebuyer?

Not necessarily. While FHA is great for first-time buyers, anyone can use these programs as long as they meet the occupancy and credit requirements.

What if a unit is vacant when I buy it?

Lenders will use "appraiser-projected rents" to determine how much income the property can likely produce. You don't always need a signed lease in place to use that income for qualification. You can find more details in our FAQ section.

How do I handle repairs?

Many investors use a portion of their rental income to fund a "CapEx" (Capital Expenditure) fund. This ensures that when a water heater goes out in Unit 2, the money is already there to fix it without touching your personal savings.

Next Steps for Your Investment Journey

Multi-family properties are one of the most reliable vehicles for building wealth in the United States. They provide shelter, generate income, and offer tax benefits that single-family homes often cannot match.

If you are curious about how a duplex or fourplex fits into your financial future, the first step is to get a clear picture of your borrowing power. We provide transparent guidance to help you navigate the complexities of DTI ratios, self-sufficiency tests, and market-specific nuances.

Explore our about us page to learn more about our commitment to your success, or see what other investors are saying on our testimonials page.

Explore your options with a strategist who understands the numbers.

Schedule a 1-on-1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664