Mortgage Rates Impact: What Today’s Late-Day Market News Means for Your 2026 Home Purchase

Navigating the mortgage market requires a firm grasp of daily shifts and long-term economic trends. As we approach the end of May 2026, today’s late-day financial updates have sent a ripple through the industry, affecting everyone from first-time buyers in Alabama to seasoned investors in California. Staying ahead of these fluctuations is the only way to ensure your real estate strategy remains robust and profitable in a changing landscape.

Market volatility has returned to the forefront as late-day headlines suggest a shift in investor sentiment regarding the broader economy. For homeowners looking to refinance or buyers entering the competitive spring market, understanding the "why" behind the numbers is the first step toward a successful closing. We are seeing a unique intersection of inflation data and geopolitical headlines that directly influence how lenders price their products in real-time.

Defining Key Market Drivers

10-Year Treasury Yield: The benchmark interest rate on a 10-year debt obligation issued by the United States government. Application: This rate serves as the primary indicator for long-term mortgage pricing, meaning as this yield fluctuates, your potential home loan interest rate typically follows suit.

Mortgage-Treasury Spread: The difference in yield between a 30-year fixed-rate mortgage and the 10-year Treasury note. Application: A widening spread often indicates increased market risk or decreased liquidity, leading to higher rates for you even if the Treasury yield remains flat.

Analyzing Today's Late-Day Market Sentiment

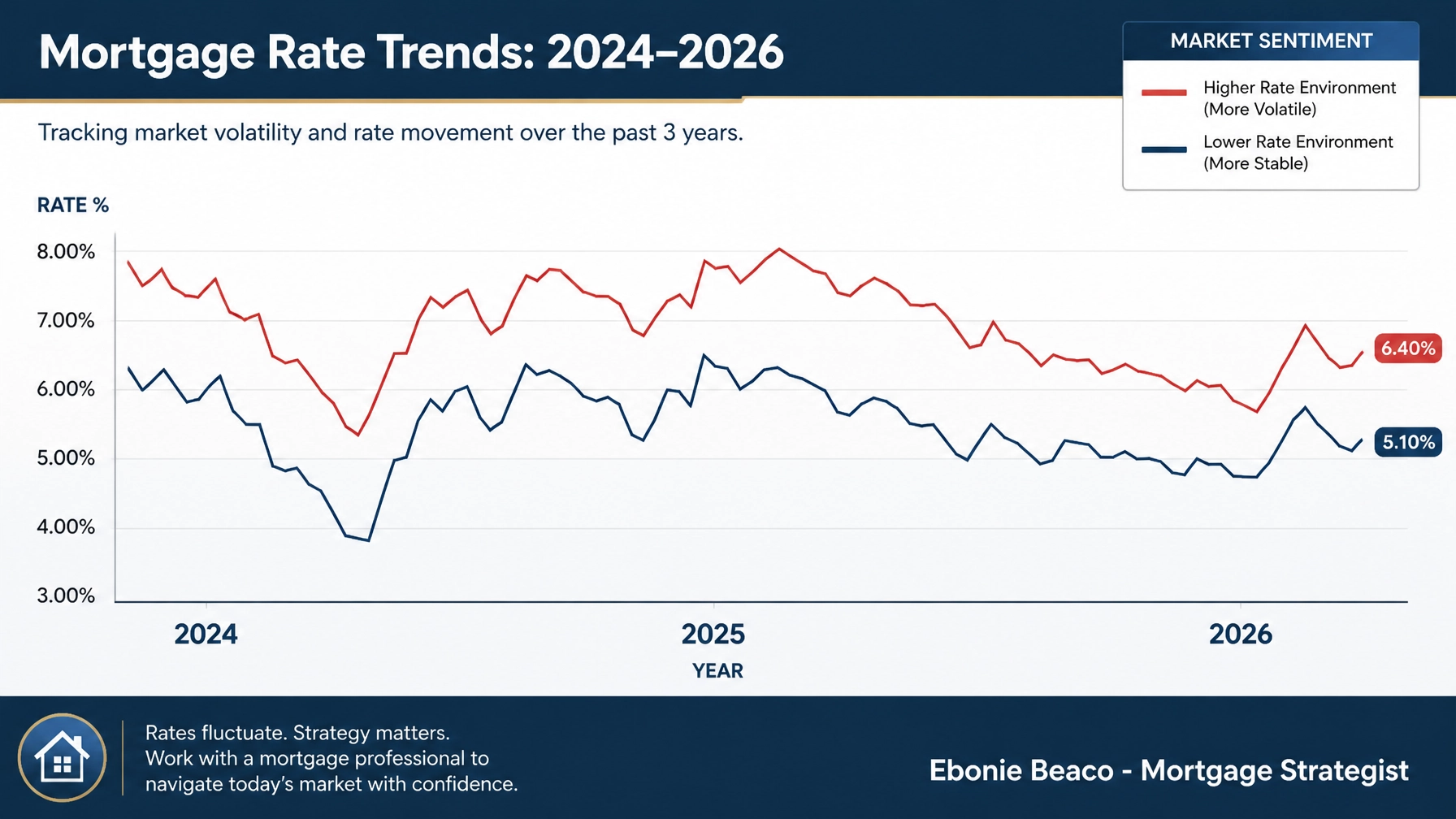

As of late this evening, the 30-year fixed-rate mortgage is hovering near 6.51%, a slight jump from earlier in the week. This movement stems from recent inflation reports and geopolitical tensions in the Middle East that have caused investors to retreat into safer assets. According to the Freddie Mac PMMS, while rates are lower than the 7% peaks seen in early 2024, they remain higher than many economists projected for the mid-2020s.

This "higher-for-longer" environment forces a strategic pivot for those planning a move in Florida, Georgia, or Virginia. The late-day sell-off in the bond market suggests that the Federal Reserve may remain cautious about further rate cuts in the immediate future. For you, this means that the window to lock in a sub-6.5% rate may be narrowing as we head into the summer months.

The housing market in 2026 is characterized by persistent demand and a slow thawing of inventory. While more sellers are listing their homes compared to two years ago, the "lock-in effect" still keeps many traditional homeowners on the sidelines. Consequently, the buyers who are winning today are those utilizing Non-QM mortgage loans and creative financing structures to offset the impact of current rates.

Regional Market Highlights: From Chicago to the Atlantic Coast

In Illinois, specifically throughout the Chicago metropolitan area, real estate activity remains high despite the late-day rate news. Market reports indicate that entry-level homes are still seeing multiple offers, often closing above the asking price within days. This localized demand creates a sense of urgency for buyers to secure their financing before further rate volatility occurs.

Investors in Michigan and Indiana are increasingly turning to DSCR rental property loans to bypass personal debt-to-income (DTI) requirements. By focusing on the income potential of the property rather than personal W-2 earnings, these investors can scale their portfolios even when traditional rates fluctuate. This strategy is particularly effective in college towns and growing urban centers where rental demand is consistent.

Across the Southeast in Arkansas, Kentucky, and Missouri, the availability of down payment assistance (DPA) programs is helping more families bridge the affordability gap. While the late-day news may seem daunting, these programs provide a critical buffer for first-time buyers. Understanding the local nuances of these markets is essential for anyone looking to build wealth through real estate this year.

Strategic Financing for Real Estate Investors

For the professional investor, today's news is a signal to review existing portfolios and look for equity extraction opportunities. Using a Cash-Out Refinance can provide the necessary capital to fund a fix and flip project or acquire a new Airbnb and short-term rental property. When you extract equity strategically, you are essentially "recycling" your capital to increase your overall net worth and monthly cash flow.

Case Study: The DSCR Calculation

DSCR (Debt Service Coverage Ratio) Loans: A loan where qualification is based on the rental income generated by the property rather than the personal income of the borrower. Application: Ideal for real estate investors who want to scale their portfolios without their personal debt-to-income ratio getting in the way.

Consider an investor in Florida purchasing a property valued at $500,000. With a 75% loan-to-value (LTV), the loan amount is $375,000. If the monthly principal, interest, taxes, and insurance (PITI) payment is $3,100 and the expected monthly rent is $4,000, the calculation is as follows:

- $4,000 (Monthly Income) / $3,100 (Monthly Expense) = 1.29 DSCR

Because the ratio is above 1.20, most specialized lenders will fund this deal based on the property’s performance alone. This allows the investor to close quickly and move on to the next deal without the hurdles of traditional documentation. Explore how these ratios can work for your specific investment goals by analyzing your target properties today.

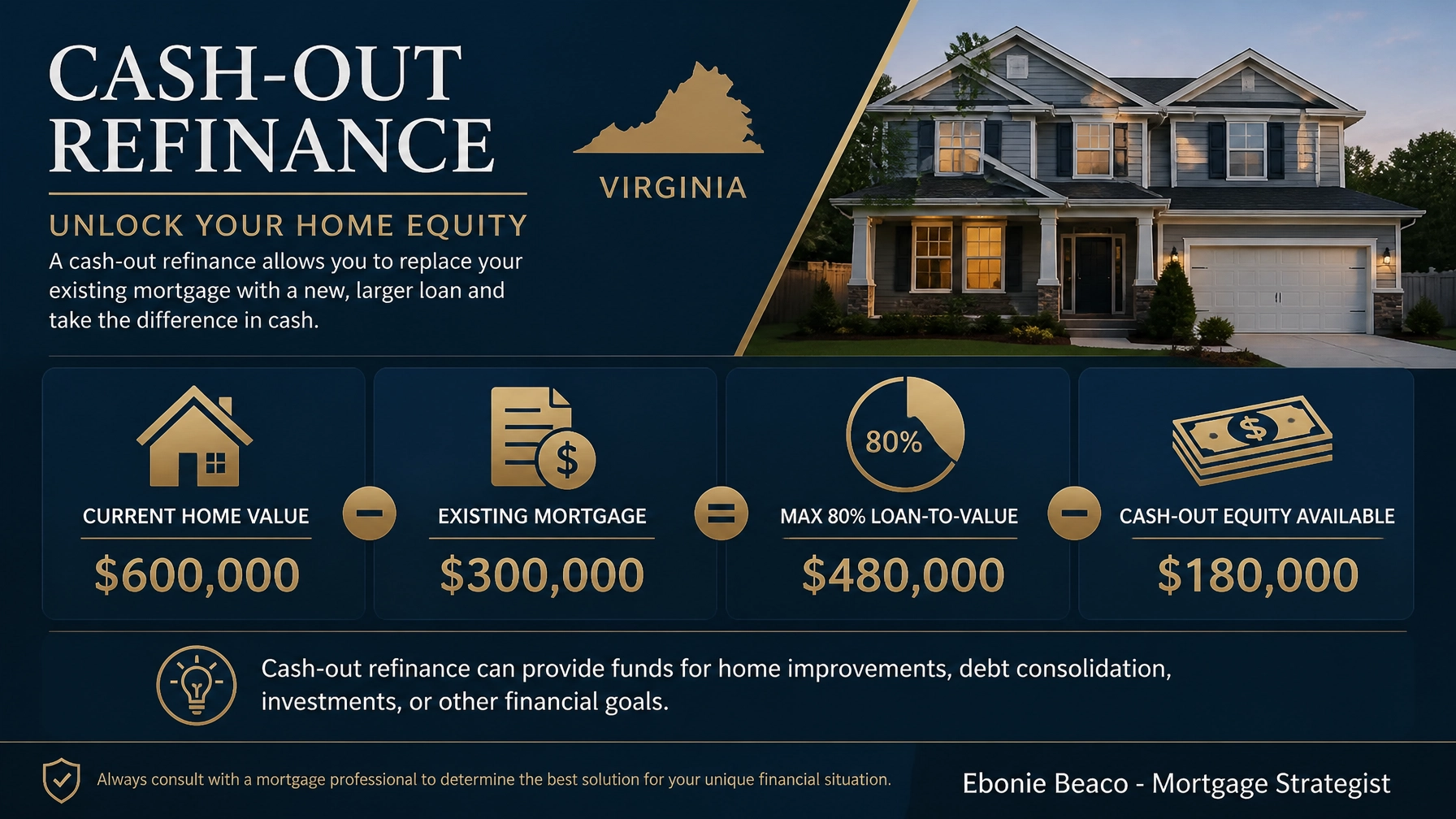

Leveraging Home Equity in a Rising Rate Environment

If you are a homeowner in Virginia or California with significant equity, today’s market news shouldn't deter you from accessing your home's value. A HELOC (Home Equity Line of Credit) functions as a revolving credit line that allows you to borrow against your equity for renovations or further investments. Unlike a traditional second mortgage, you typically only pay interest on the amount you actually use.

Equity Extraction Strategy

Imagine a homeowner in Virginia with a property valued at $600,000 and an existing mortgage balance of $300,000. By utilizing a cash-out refinance at an 80% combined loan-to-value (CLTV), the numbers break down like this:

- Current Property Value: $600,000

- Max 80% LTV: $480,000

- Existing Debt: $300,000

- Accessible Equity: $180,000

With $180,000 in liquid capital, this homeowner can pay off high-interest debt or provide a down payment for a new investment property. Compare the benefits of a HELOC versus a full cash-out refinance to determine which path preserves your current low-interest rate on your primary mortgage.

Navigating Late-Day Volatility with Confidence

The key to succeeding in the 2026 housing market is agility and education. When you hear news of late-day rate spikes, it is easy to feel overwhelmed, but having a clear plan in place mitigates that uncertainty. Access the tools and guidance you need to interpret these numbers through the lens of your long-term financial goals.

Whether you are looking at bridge loans for a quick acquisition or bank statement loans for the self-employed, there is always a path forward. The market does not stop moving, and neither should your plans for homeownership or investment. By staying informed on daily trends, you position yourself as a savvy participant in one of the most dynamic real estate environments in recent history.

Jump in to a conversation about your specific scenario to see how these market updates impact your purchasing power. We are here to guide you through the complexities of the current landscape with transparency and expertise. Every shift in the market presents a new opportunity for those who are prepared to act.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664