Mortgage Rate Secrets Revealed: What Experts Don’t Want You to Know About This Week’s Market Shift

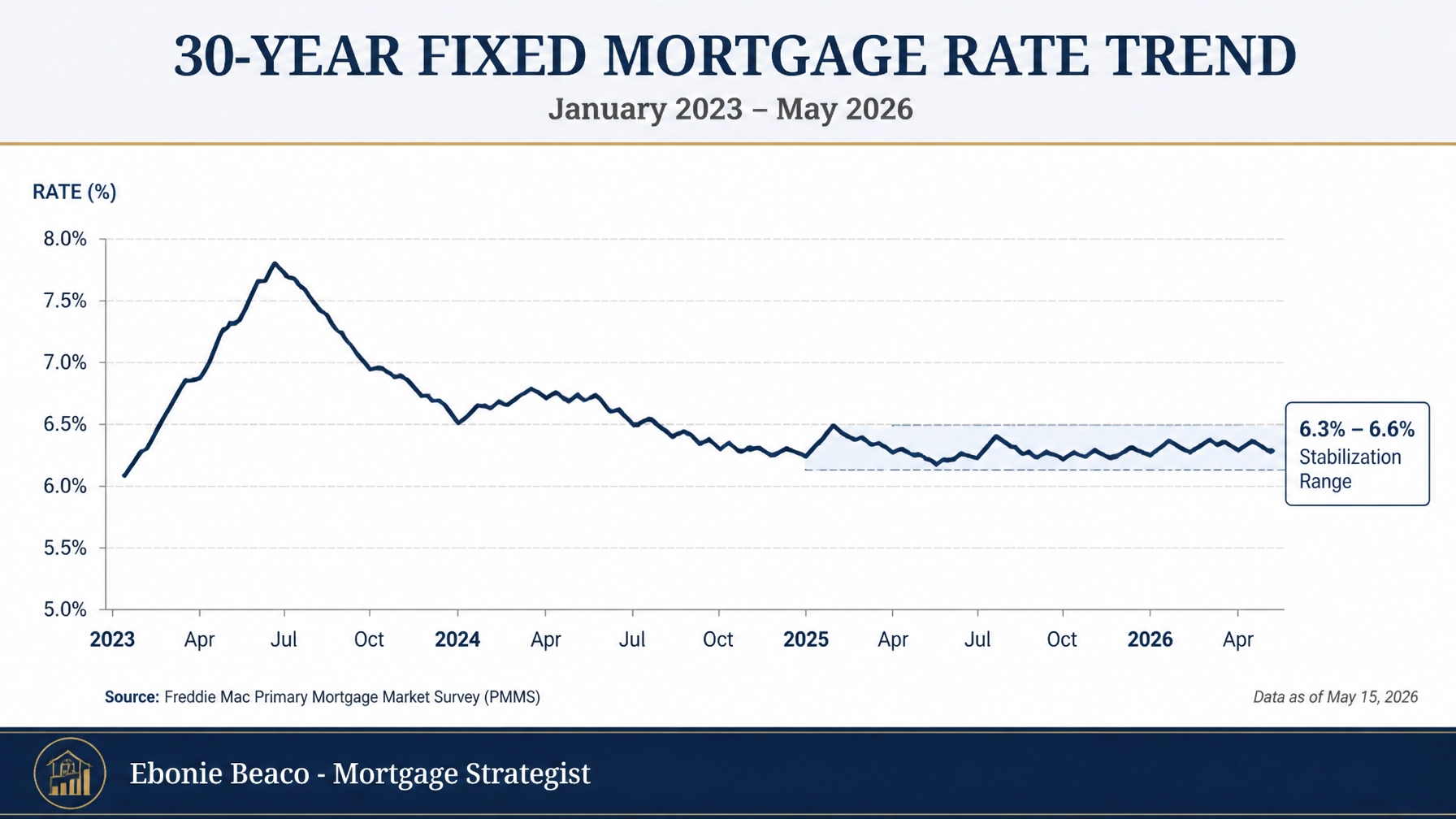

The mortgage landscape in early June 2026 has reached a pivotal stabilization point that many analysts failed to predict just a few months ago. While the headlines often focus on the daily fluctuations of the 30-year fixed rate, a more profound shift is occurring beneath the surface of the primary market. Borrowers across the United States are moving away from the "waiting game" as the reality of a higher-for-longer interest rate environment becomes the established baseline for personal and professional planning. This week, we are seeing the average 30-year fixed mortgage rate hover between 6.3% and 6.6%, creating a unique window for those who understand how to navigate non-traditional financing.

Understanding the Language of Today’s Market

To navigate the current financial climate, it is essential to understand the technical frameworks that lenders use to evaluate risk and opportunity. These terms are often the foundation of the strategies used by successful investors and homeowners in states like Illinois, Florida, and California. By mastering these concepts, you can better align your financing goals with the products currently available in the marketplace.

- DSCR (Debt Service Coverage Ratio): A financial metric used primarily in investment property lending that compares a property's annual net operating income to its annual mortgage debt service. This allows investors to qualify for financing based on the property’s cash flow rather than their personal income or employment history.

- Non-QM (Non-Qualified Mortgage): A category of loan programs that do not fit the strict criteria of government-backed entities like Fannie Mae or Freddie Mac. These loans are often ideal for self-employed borrowers, entrepreneurs, or individuals with complex income structures who need flexible underwriting.

- DTI (Debt-to-Income Ratio): A percentage calculated by dividing your total monthly debt payments by your gross monthly income. While traditional loans have rigid DTI limits, many modern mortgage strategies focus on optimizing this ratio through strategic refinancing or restructuring.

- LTV (Loan-to-Value): The ratio of a loan to the value of the asset purchased, which determines the amount of equity required or available in a property. Understanding your LTV is the first step in accessing home equity through tools like a HELOC or a cash-out refinance.

The Great Stabilization: Why the Market Shifted This Week

The primary secret that many market commentators overlook is that the Federal Reserve has successfully moved the economy into a "balanced rate environment." With inflation holding near 3.8% and the federal funds rate positioned between 3.5% and 3.75%, the wild volatility seen in previous years has largely subsided. This stability is actually a hidden advantage for buyers in competitive markets like Chicago or Atlanta. When rates are stable, sellers are more willing to negotiate on price and concessions, a trend that is becoming increasingly visible in recent Bankrate mortgage survey data.

Investors and homeowners are beginning to realize that waiting for a return to 3% rates is a strategy of diminishing returns. The "lock-in effect" that previously kept inventory low is beginning to thaw as life events: such as relocation, family growth, or retirement: supersede the desire to hold onto a low-interest rate. In states like Michigan and Indiana, we are seeing a steady increase in new listings as homeowners accept the mid-6% range as the new normal. This shift is creating more options for first-time homebuyers and those looking to scale their investment portfolios through creative financing solutions.

Strategic Financing Across the Regional Markets

Each state presents its own set of opportunities and challenges within the current mortgage climate. In Florida and Georgia, the demand for short-term rental financing remains robust, even as traditional buyers face affordability hurdles. Investors in these regions are increasingly turning to DSCR rental property loans to acquire properties without the need for extensive personal income documentation. This approach focuses on the income-producing potential of the asset itself, which is a critical strategy in high-growth vacation markets.

Meanwhile, in the Midwest: specifically Illinois and Missouri: homeowners are finding significant value in tapping into their existing property equity. Property values have remained resilient, allowing many to explore a cash-out refinance to fund renovations or consolidate high-interest debt. In California and Virginia, where property values are higher, the use of bridge loans and fix-and-flip financing is a popular method for investors to secure properties quickly in low-inventory areas. By understanding the regional nuances, you can tailor your mortgage strategy to the specific housing activity in your local area.

The Investor’s Edge: Leveraging DSCR and Non-QM Loans

For the real estate investor, the current market shift highlights the power of specialized loan programs. Traditional financing often requires a level of personal documentation that can be burdensome for entrepreneurs and those with multiple properties. The DSCR investor loan serves as a vital tool for scaling a portfolio because it treats each property as an independent business. If the rent covers the mortgage, taxes, insurance, and HOA fees at a specific ratio (typically 1.15 to 1.25), the loan can move forward regardless of the borrower's personal salary.

This strategy is particularly effective for those engaged in the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method. Investors in Arkansas and Kentucky are finding that by using short-term bridge loans or hard money for the initial purchase and renovation, they can later transition into long-term DSCR financing once the property is leased. This allows for the recovery of initial capital, which can then be deployed into the next acquisition. The flexibility of Non-QM mortgage loans ensures that even as the primary market remains tight, the investment market continues to offer pathways to wealth creation.

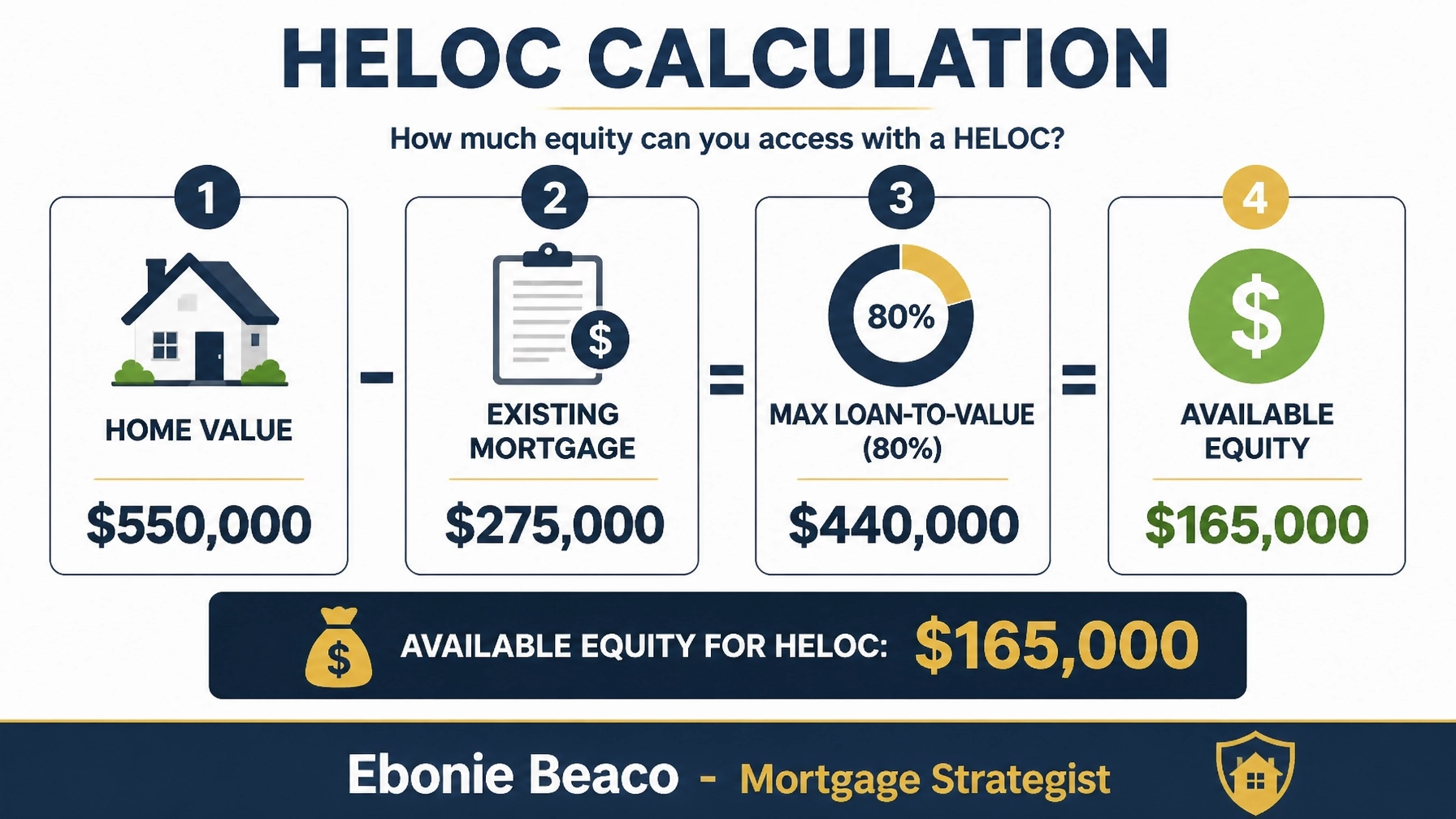

Practical Financial Example: Accessing Equity via HELOC

To understand how these concepts apply to your personal finances, let’s look at a common scenario for a homeowner in a city like Chicago. Many homeowners have seen their property values increase significantly over the last few years, yet they feel "trapped" by a low-interest first mortgage. A Home Equity Line of Credit (HELOC) allows you to access that wealth without disturbing your primary low-rate loan. Consider the following breakdown of how a homeowner might access funds for an investment property down payment or home improvements.

In this example, the homeowner owns a property valued at $550,000 with an existing mortgage balance of $275,000. Most lenders will allow a combined loan-to-value (CLTV) of up to 80%, which in this case equals $440,000. By subtracting the existing mortgage from this amount, the homeowner is left with $165,000 in available equity. This capital can be used as a down payment for a second property, a renovation of the current home, or even as a reserve fund for future investment opportunities. Accessing equity this way is often more cost-effective than a full cash-out refinance when your primary rate is significantly lower than current market offerings.

Navigating the Path Forward

As we move further into the summer of 2026, the key to success in real estate and mortgage financing is education and agility. The "secrets" of the market are hidden in the data and the specialized programs that go beyond the 30-year fixed average. Whether you are a first-time homebuyer in Alabama or a seasoned commercial investor in California, the current stability offers a chance to build a long-term strategy with confidence. Explore your options, compare the different loan programs available, and jump in when the numbers align with your financial goals.

The housing market is no longer defined by the rapid spikes of the early 2020s but by a steady, mature environment that rewards those who take a strategic approach to debt and equity. By aligning your financing with professional guidance and localized market knowledge, you can navigate these shifts with ease. Access the resources and calculators available to better understand your specific scenario and take the next step toward your homeownership or investment objectives.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664