Mortgage News Secrets Revealed: What Today’s Market Headlines Mean for Your Next Refinance

The mortgage landscape on this Saturday, June 6, 2026, presents a starkly different picture than the volatility we witnessed just two years ago. As the sun rises over the Chicago skyline and stretches across the coastal properties of California and Florida, homeowners and investors are waking up to a market that has finally found its footing. The headlines today reflect a stabilizing economy where the aggressive rate hikes of the mid-2020s have transitioned into a more predictable, downward-drifting cycle. For those who have been waiting on the sidelines, the secrets hidden within today’s mortgage news offer a clear roadmap for your next financial move.

Understanding the nuance of today’s market requires looking beyond the surface-level percentages that dominate the nightly news. While the national average for a 30-year fixed mortgage has settled into the mid-6% range, the real opportunities lie in how you leverage these rates against your current property equity. Whether you are a homeowner in Virginia looking to lower your monthly obligation or a seasoned investor in Georgia seeking to expand a rental portfolio, the current data suggests that the "wait and see" approach is rapidly losing its utility. Jump in as we dissect the latest trends and reveal how to position yourself for a successful refinance in this evolving environment.

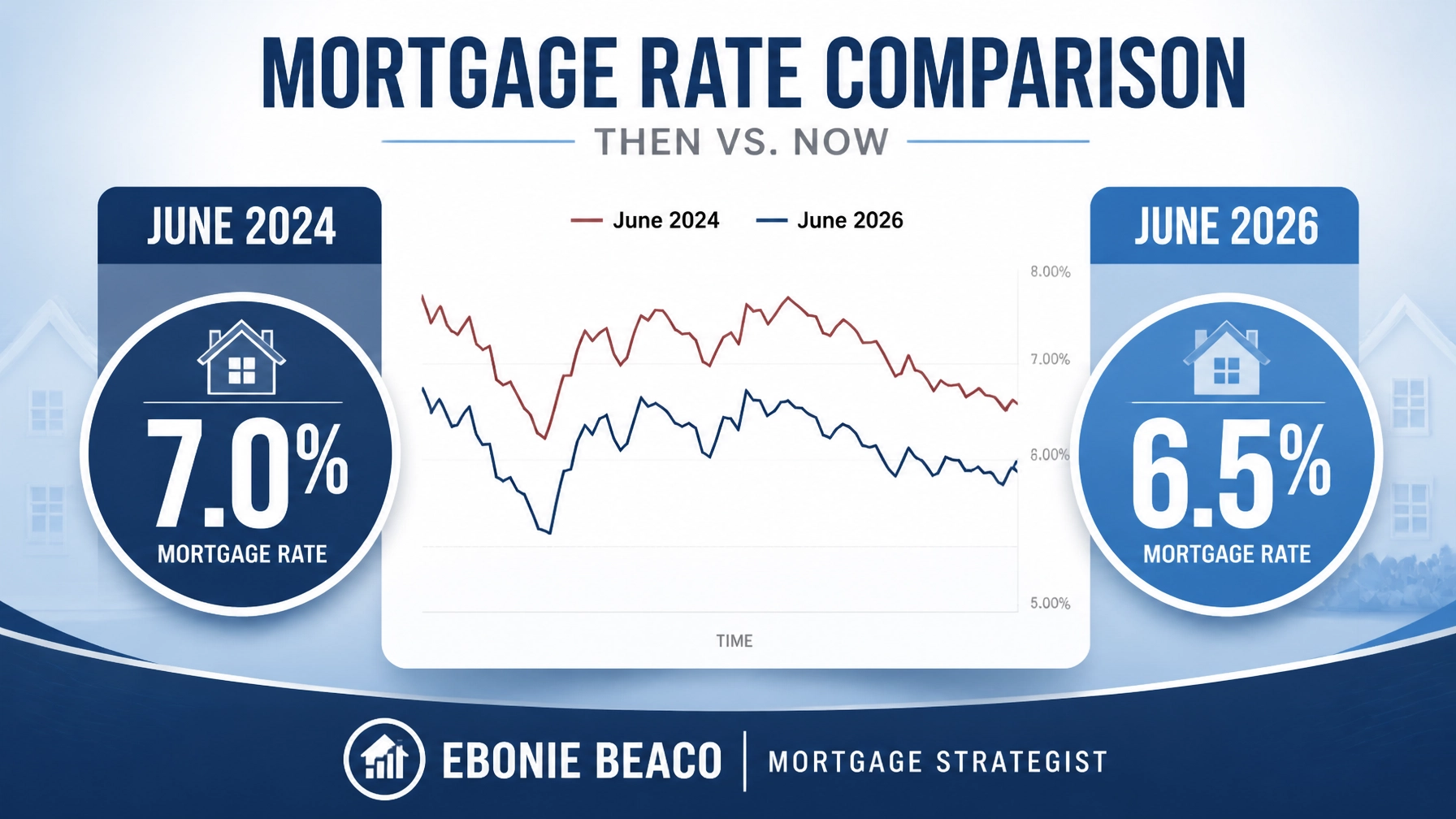

Decoding the 2026 Rate Shift: From 7% to Stability

If you examine the data from June 2024, the primary headline was the persistent struggle with 7% interest rates and a severe lack of housing inventory. According to the National Association of Realtors (NAR), affordability was at a historical low during that period, forcing many families to delay their dreams of homeownership or refinancing. Fast forward to June 2026, and the narrative has shifted toward a gradual easing of borrowing costs, providing a much-needed reprieve for those locked into higher-rate debt from the previous cycle.

This shift is not merely a coincidence but the result of cooling inflation and a more balanced labor market that has allowed the Federal Reserve to maintain a neutral stance. For homeowners in states like Michigan and Indiana, this means that the "lock-in effect": where sellers were afraid to move because of their ultra-low 3% rates from the pandemic era: is starting to thaw. As rates move closer to the 6% mark, the math for moving or refinancing becomes increasingly attractive, especially when considering the significant home price appreciation seen over the last twenty-four months.

Explore the current trends reported by Freddie Mac, which highlight how current mortgage applications for refinancing have reached their highest levels since 2022. This surge in activity indicates that the market is finally adjusting to the "new normal" of the mid-6% range. For residents in the diverse markets of Alabama, Arkansas, and Missouri, these national trends provide a foundation for local strategies that focus on equity preservation and wealth building through strategic debt restructuring.

The New Definitions of Mortgage Success

In today’s sophisticated lending environment, being an informed borrower means mastering the terminology that lenders use to evaluate your profile. We have categorized these essential concepts to help you navigate your refinance with confidence and clarity.

- Debt-to-Income Ratio (DTI)

- Definition: A personal financial metric that compares an individual’s monthly debt payments to their monthly gross income.

- Application: Lenders use your DTI to determine your ability to manage monthly payments and repay the money you plan to borrow.

- Debt Service Coverage Ratio (DSCR)

- Definition: A measurement of the cash flow available to pay current debt obligations, specifically used for investment property loans.

- Application: Investors use DSCR loans to qualify for financing based on the property’s rental income rather than their personal tax returns.

- Loan-to-Value (LTV) Ratio

- Definition: An assessment of lending risk that financial institutions examine before approving a mortgage, calculated by dividing the loan amount by the appraised property value.

- Application: Maintaining a lower LTV ratio often allows you to access better interest rates and avoid the requirement for private mortgage insurance.

- Non-QM Mortgage Loans

- Definition: A type of loan that does not conform to the standard guidelines of government-backed agencies like Fannie Mae or Freddie Mac.

- Application: These loans are ideal for self-employed individuals or entrepreneurs in states like California and Florida who have complex income structures.

Strategy 1: The Rate-Term Refinance

The most common motivation for a refinance today is the rate-term adjustment, which focuses on changing the interest rate or the length of the loan without extracting cash. If you purchased a home or investment property in 2023 or early 2024 when rates were peaking, you might be holding a mortgage with an interest rate above 7.5%. In the current June 2026 market, a rate-term refinance could potentially shave a full percentage point or more off your current note.

Compare the long-term savings of a lower monthly payment against the closing costs of the new loan to determine your "break-even" point. For homeowners in high-growth areas of Virginia or Kentucky, reducing a monthly payment by even $200 can result in tens of thousands of dollars in savings over the life of the loan. Access our mortgage calculators to run these scenarios for your specific property and see if the current headlines translate into real-world savings for your household.

Strategy 2: The Cash-Out Equity Extraction

For many property owners, the most powerful secret in today’s market is not just the interest rate, but the massive amount of equity accumulated since 2024. Despite higher borrowing costs, home values in metropolitan areas like Chicago, Atlanta, and across the state of Florida have continued to climb. A cash-out refinance allows you to tap into this equity to fund home improvements, consolidate high-interest debt, or provide the down payment for your next investment property.

Consider the following financial scenario for a homeowner in a thriving market:

Property Value: $600,000

Current Mortgage Balance: $320,000

Maximum Allowable Loan (80% LTV): $480,000

Available Equity for Cash-Out: $160,000

In this example, the borrower can access $160,000 in liquid capital while still maintaining a 20% equity stake in their primary residence. If this homeowner uses that $160,000 to purchase a duplex in a high-demand rental area of Michigan or Missouri, they are effectively using their existing home to build a multi-generational wealth machine. Accessing equity in this manner is a hallmark of sophisticated real estate investing, particularly for those looking to scale their portfolios without using their personal savings.

Strategy 3: DSCR for Rental Portfolios

For the modern real estate investor, the Debt Service Coverage Ratio (DSCR) loan has become the "secret weapon" of the 2026 market. Unlike traditional loans that require extensive W-2 documentation and personal income verification, DSCR loans focus on the performance of the asset itself. This is particularly beneficial for Airbnb and short-term rental operators in Florida and California, where seasonal income can sometimes complicate a standard mortgage application.

Jump in and analyze how a DSCR loan works in practice. If you are eyeing a luxury rental property in Atlanta or a multi-unit building in Chicago, the lender will look at the projected monthly rental income. If the property generates $3,500 in rent and the total mortgage payment (including taxes and insurance) is $2,800, the DSCR is 1.25. Most lenders view a ratio of 1.20 or higher as a strong indicator of a healthy investment, allowing you to secure financing based on the property’s ability to pay for itself.

Market Spotlight: From Chicago to California

The local nuances of the real estate market dictate the success of your financing strategy. In Chicago, we are seeing a resurgence in the acquisition of two- to four-unit buildings by "house hackers" who use residential financing to live in one unit while renting out the others. Our Chicago neighborhoods market reports indicate that areas with strong transit access continue to command premium rents, making them ideal candidates for high-LTV financing.

Moving south to Florida and Georgia, the demand for short-term rental financing remains robust. Investors are leveraging Non-QM and bank statement loans to navigate the unique tax advantages of those states while expanding their hospitality footprints. Meanwhile, in California, the focus has shifted toward Accessory Dwelling Units (ADUs) and utilizing HELOCs to add density to existing residential lots. Regardless of the state you call home, the fundamental principle remains the same: align your financing with the specific economic drivers of your local community.

Conclusion: Navigating Your Next Move

The mortgage news headlines of June 2026 provide more than just data; they provide a signal that the market is ready for action. Whether you are pursuing a rate-term refinance to increase your monthly cash flow or a cash-out refinance to fuel your next big investment, the tools and programs available today are designed to support your long-term wealth goals. Transparency, education, and strategic guidance are the keys to unlocking the doors that today’s market has opened.

If you are a homeowner, a seasoned landlord, or an aspiring investor, now is the time to audit your current mortgage and explore the possibilities that a stabilized rate environment offers. The secrets are no longer hidden; they are written in the equity of your home and the cash flow of your properties. Reach out to discuss how these national headlines can be translated into a personalized strategy for your unique financial profile.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664