Mortgage Liquidity Significance: Why Florida and California Investors Are Pivoting to DSCR Loans This Week

Mortgage liquidity represents the ease and speed with which capital flows from lenders to borrowers to facilitate property acquisitions. In the current lending environment of May 2026, liquidity is the quiet driver behind almost every successful investment deal across the Sunbelt and the West Coast. When traditional banks become cautious, credit availability tightens, and even high-quality projects may struggle to secure funding through standard channels. This week, we are observing a significant shift as seasoned investors in Florida and California pivot toward Debt Service Coverage Ratio (DSCR) loans to maintain their momentum. These investors prioritize reliable, scalable capital access over the rigid requirements of traditional personal income underwriting.

Understanding the Role of Mortgage Liquidity in 2026

The significance of liquidity cannot be overstated for those looking to expand a real estate portfolio in competitive markets like Miami, Orlando, or Los Angeles. Liquidity allows you to move quickly when a distressed property hits the market or when a high-yield short-term rental opportunity arises. Without accessible capital, your ability to leverage market cycles is severely diminished, regardless of how strong your personal credit might be. DSCR loans provide a vital alternative by shifting the focus from your personal debt-to-income (DTI) ratio to the performance of the asset itself. This creates a more fluid environment for capital, allowing deals to close in timeframes that conventional financing simply cannot match.

In states like Florida and California, where home prices often outpace local wage growth, traditional DTI limits act as a bottleneck for ambitious investors. By utilizing DSCR products, you can sidestep the delays associated with tax return reviews and complex employment verifications. This shift in underwriting philosophy ensures that liquidity remains available to those who can identify income-producing properties. This week’s market data suggests that investors are increasingly willing to trade slightly different rate structures for the certainty of a closed loan. When you understand how to navigate these liquidity shifts, you position yourself as a more capable buyer in any negotiation.

Defining the DSCR Loan for the Modern Investor

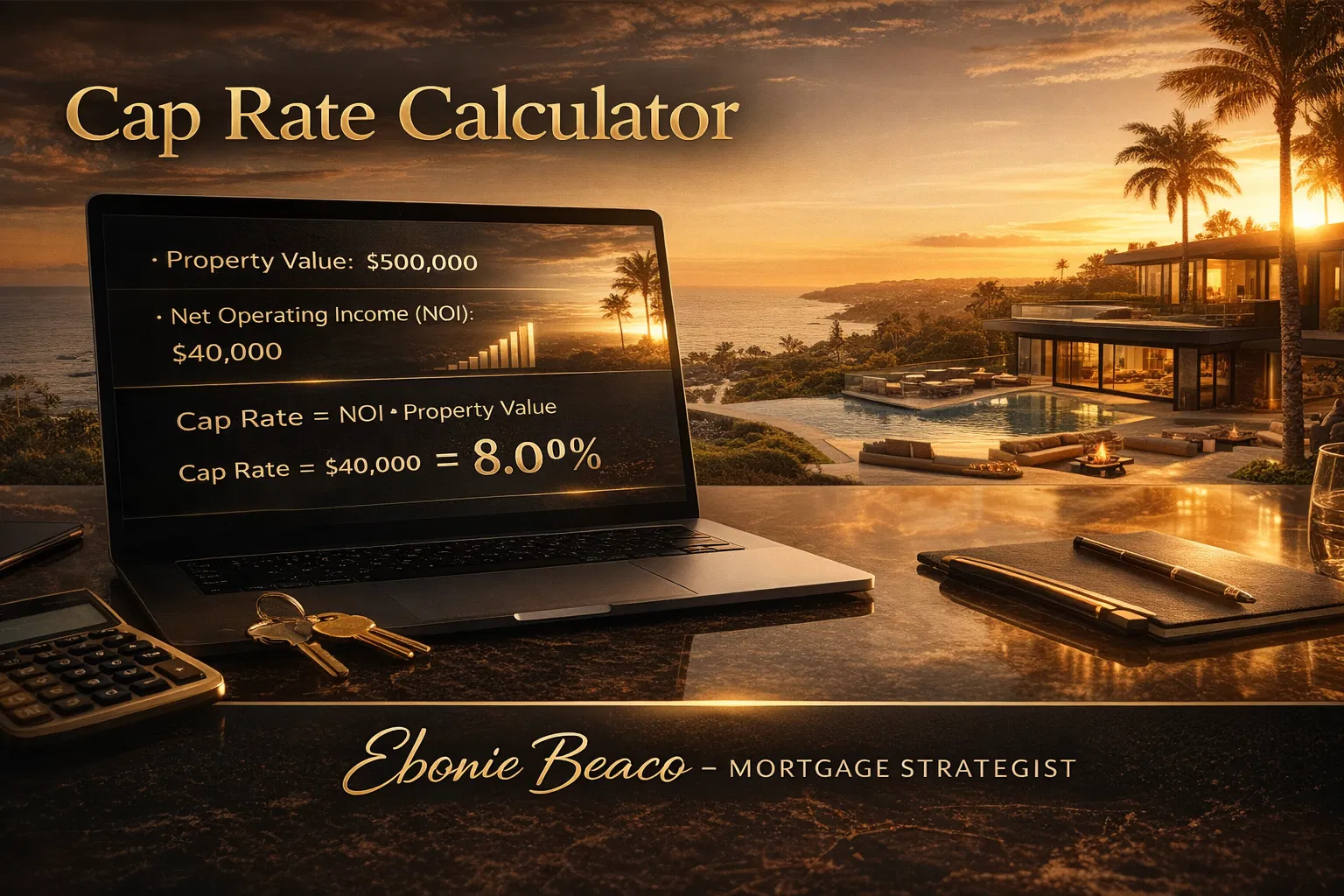

A DSCR loan is a specialized investment property mortgage underwritten primarily based on the property’s cash flow rather than the borrower’s personal income. DSCR stands for Debt Service Coverage Ratio, which is a mathematical comparison of the property’s Net Operating Income (NOI) against its annual debt service. If the property generates enough rent to cover the mortgage, taxes, insurance, and association dues, it qualifies for financing under this program. This eliminates the need for tax returns, W-2s, or pay stubs, which is a major advantage for self-employed individuals or those with significant tax write-offs. You can explore the specific requirements for these programs through our loan programs page.

The DSCR Calculation Explained

The basic formula for this ratio is simple: DSCR = Monthly Rental Income ÷ Monthly PITI (Principal, Interest, Taxes, Insurance). A ratio of 1.0 means the property breaks even, while a ratio of 1.25 indicates the property generates 25% more income than its total debt obligations. While some lenders in 2026 are tightening their standards, many still offer "no-ratio" products for investors with strong down payments or high-liquidity backgrounds. This flexibility is essential for those acquiring properties in emerging markets where future rent growth is expected but current yields are lean. By focusing on the asset's viability, these loans empower you to build a portfolio based on real-world performance.

Why Florida Investors Are Leading the DSCR Pivot

Florida remains one of the most active states for DSCR lending due to its robust tourism industry and continued population growth. Investors in cities like Tampa, Jacksonville, and the Florida Keys are leveraging these loans to capitalize on the high demand for vacation rentals. Because DSCR lenders often allow the use of projected short-term rental (STR) income, properties that might fail a traditional mortgage test become viable investment targets. The speed of execution in the Florida market is another reason for this pivot, as cash-like closing speeds are often required to win bids. Investors are finding that the ability to close a deal in two weeks provides a massive competitive edge over those using agency financing.

Recent data from the National Association of Realtors indicates that investor activity in Florida remains higher than the national average, even as insurance costs fluctuate. This trend is supported by the availability of "landlord loans" that do not count against an investor's personal credit capacity in the same way a conventional loan does. For those managing multiple properties in the Sunshine State, the ability to scale without hitting a 10-loan limit is a game-changer. This week, we are seeing a surge in inquiries for refinancing existing Florida assets to pull equity for new acquisitions. This strategy, often paired with the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), relies heavily on the liquidity provided by the DSCR market.

California’s Unique Drive Toward Asset-Based Lending

California presents a different set of challenges, including some of the highest entry prices in the United States and complex regulatory environments. In markets like San Diego, San Francisco, and the Inland Empire, investors often find that their personal DTI is maxed out after just one or two acquisitions. DSCR loans serve as a vital release valve for this pressure, allowing California residents to continue investing regardless of their personal debt levels. This is particularly relevant for the "paper poor" investor who has substantial assets and equity but uses legal tax deductions to minimize their adjusted gross income. By ignoring the tax return and focusing on the property’s rent-to-value ratio, California investors can unlock financing that big banks would typically deny.

The pivot in California is also driven by the desire to move away from the slow, bureaucratic processes of traditional retail banks. With the current volatility in interest rates, the risk of a deal falling through due to a 60-day closing window is simply too high for many professionals. DSCR lenders in the Golden State are increasingly offering creative solutions for mixed-use properties and small multifamily units. This flexibility allows you to diversify your holdings within the state while maintaining the liquidity needed to address maintenance or renovation needs. As long as the property shows a path to profitability, the financing remains accessible, bridging the gap between high-cost entry and long-term wealth building.

Visualizing Your Investment Profitability

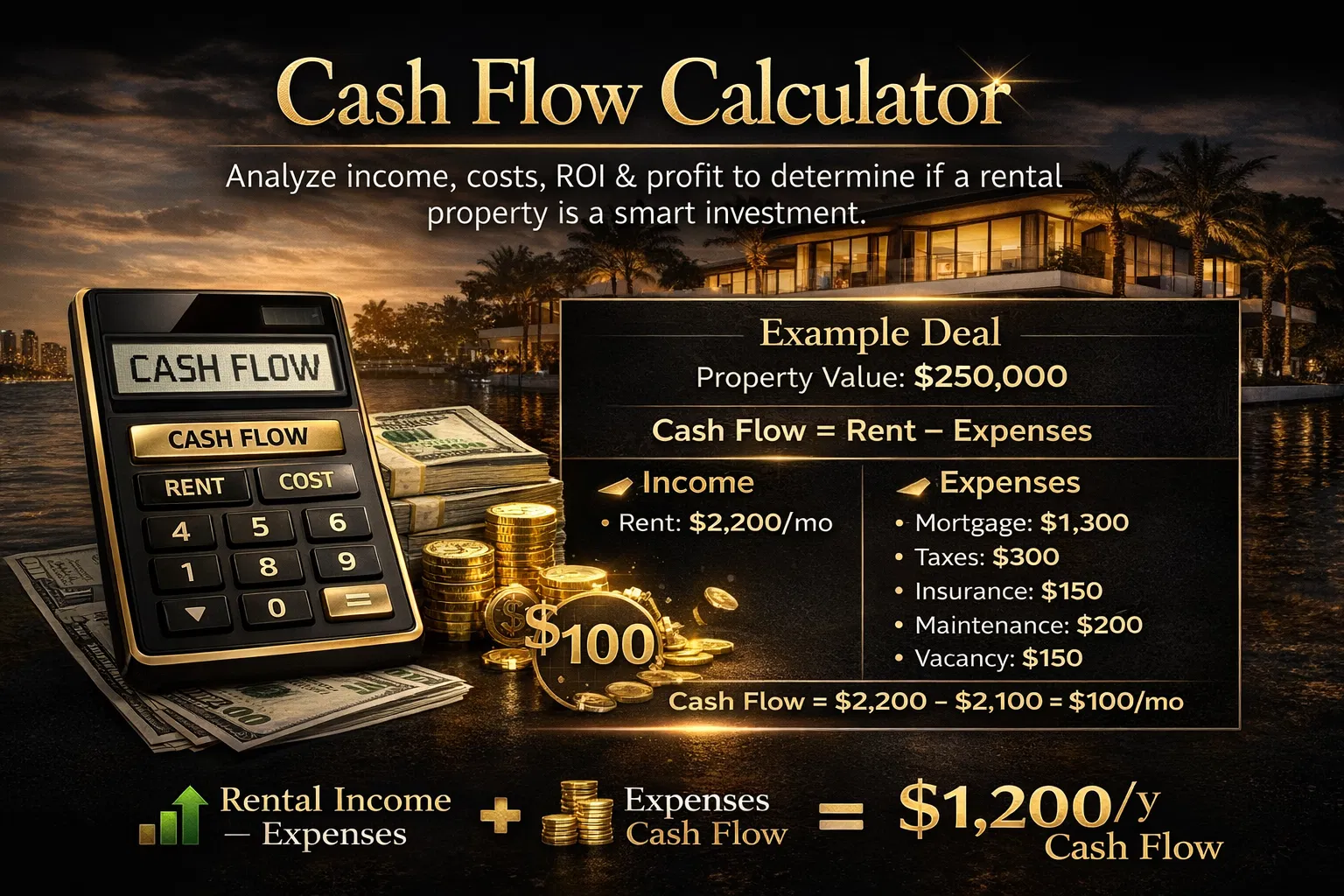

Understanding the numbers is the first step toward a successful pivot into DSCR lending. To illustrate how these deals are analyzed, consider a property with a purchase price of $400,000 and an expected monthly rent of $3,500. If the total monthly payment, including taxes and insurance, comes to $2,800, the DSCR would be 1.25. This healthy ratio would easily qualify for most standard programs, often with competitive interest rates and lower down payment requirements. You can use our mortgage calculators to run your own scenarios and see how different loan terms affect your monthly cash flow.

When you analyze a deal, you must also account for property management fees and vacancy rates to ensure your liquidity remains intact during lean months. Experienced investors in Virginia and Georgia are currently using these same metrics to evaluate "fix and flip" opportunities that they eventually transition into long-term rentals. This holistic approach to financing allows you to plan your exit strategy before you even sign the purchase agreement. By keeping your personal credit and income separate from your business assets, you protect your financial health while building a sustainable real estate enterprise. A clear understanding of your annual profit and cash-on-cash return is essential for presenting your portfolio to potential partners or future lenders.

The Strategic Advantage of Scaling with DSCR

One of the primary benefits of the DSCR model is the ability to scale a portfolio across multiple states without the friction of traditional underwriting. Whether you are looking at properties in Michigan, Illinois, or Alabama, the logic of the loan remains consistent: the property must perform. This allows you to build a national footprint while working with a single mortgage strategist who understands your overall goals. Instead of explaining your tax returns to ten different banks, you can provide a single set of documents to a lender that specializes in investor-friendly products. This efficiency is why many of our clients are moving away from local community banks and toward more agile, nationwide platforms.

For those pursuing the BRRRR strategy, DSCR loans provide the perfect "refinance" vehicle to pull your initial capital back out of a project. Once a property is renovated and a tenant is in place, the new, higher rental income is used to justify a larger loan amount. This extracted equity can then be used as a down payment for your next acquisition, creating a self-sustaining cycle of growth. This week, we have seen successful examples of this in the Atlanta and Chicago markets, where investors are transforming distressed units into high-performing rentals. The flexibility of these programs ensures that your growth is limited only by your ability to find good deals, not by a lender's arbitrary cap on the number of properties you own.

Navigating Risks and Local Market Nuances

While DSCR loans offer incredible liquidity, it is vital to stay informed about local regulations that could impact your property's performance. In California, rent control laws can affect your ability to increase income, which directly impacts your future DSCR. In Florida, the rising cost of property insurance must be factored into your debt service calculations to ensure you remain above the lender's required ratio. We recommend reviewing current Federal Reserve lending data to stay ahead of broader economic shifts that could influence interest rates. Being an educated investor means looking beyond the immediate approval and considering the long-term viability of each asset in your portfolio.

Furthermore, investors in states like Virginia and Indiana should be mindful of local zoning changes that could affect short-term rental eligibility. If your DSCR calculation relies on Airbnb income, a change in city ordinances could suddenly turn a profitable asset into a monthly liability. Always have a "Plan B" where the property can still cover its debt as a long-term rental if needed. Maintaining a healthy cash reserve is another critical component of your liquidity strategy. Most DSCR lenders will require three to six months of payments in reserves to ensure you can handle unexpected repairs or vacancies. By preparing for these variables, you ensure that your pivot to DSCR lending is a sustainable move toward financial freedom.

Take the Next Step in Your Investment Journey

The shifting landscape of mortgage liquidity requires a proactive approach to financing. If you are a homeowner in Virginia looking to access equity or an investor in Florida ready to scale, understanding these options is the key to your success. At Home Loans Network, we specialize in guiding our clients through the complexities of real estate finance with clarity and confidence. We invite you to explore our resources, from mortgage basics to advanced investor strategies, to find the right fit for your unique situation.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664