Mortgage App Surge: Rates Dip and Borrowers Jump In

Wednesday, March 18, 2026

If you have been waiting for a sign to look at your financing options, this week just handed you a billboard. We are seeing some serious movement in the market right now. As of today, Wednesday, March 18, 2026, the data is in, and it looks like a lot of you were just waiting for that one specific nudge to get off the sidelines.

According to recent reports, mortgage application volume just saw a massive 16% weekly surge. Why the sudden rush? It comes down to a brief but significant dip in interest rates. After a period of holding steady, we saw rates hover around 7.02% this week, and for many borrowers: from first-time buyers to seasoned real estate investors: that was the "green light" they needed.

You can read the full breakdown of how this brief drop in mortgage rates caused a surge in mortgage applications over at CNBC, but I want to talk about what this means for you right here, right now, in our current 2026 market.

The 16% Surge: Breaking Down the Momentum

The 16% jump in applications is not just a random blip. It tells us something very transparent about the psychology of today's market. Whether you are looking at properties in Chicago, scouting for vacation rentals in Florida, or managing a portfolio in Virginia, the sentiment is the same: buyers are sensitive to even small movements in cost.

When rates dipped toward that 7.02% mark, both purchase and refinance applications caught fire. For homeowners who bought when rates were at their peak, this window represents a chance to breathe. For investors, it is an opportunity to lock in better numbers on a DSCR rental property loan or a new acquisition.

Understanding the Technicals

To navigate this market, you need to understand the tools at your disposal. Here are a few key terms we are seeing pop up frequently during this surge:

DSCR: Debt Service Coverage Ratio.

A metric used by lenders to measure a property's ability to pay its own mortgage through rental income.

Practical Benefit: This allows investors to qualify for loans based on the property’s cash flow rather than their personal income or tax returns.

LTV: Loan-to-Value.

The ratio between the amount of the loan and the appraised value of the property.

Practical Benefit: Understanding your LTV helps you determine how much equity you can pull out during a cash-out refinance to fund your next investment.

Non-QM: Non-Qualified Mortgage.

A loan program that does not follow the standard federal guidelines for traditional mortgages.

Practical Benefit: These are perfect for self-employed borrowers or investors who use bank statement programs to prove income rather than W-2s.

Explore your options and compare programs today.

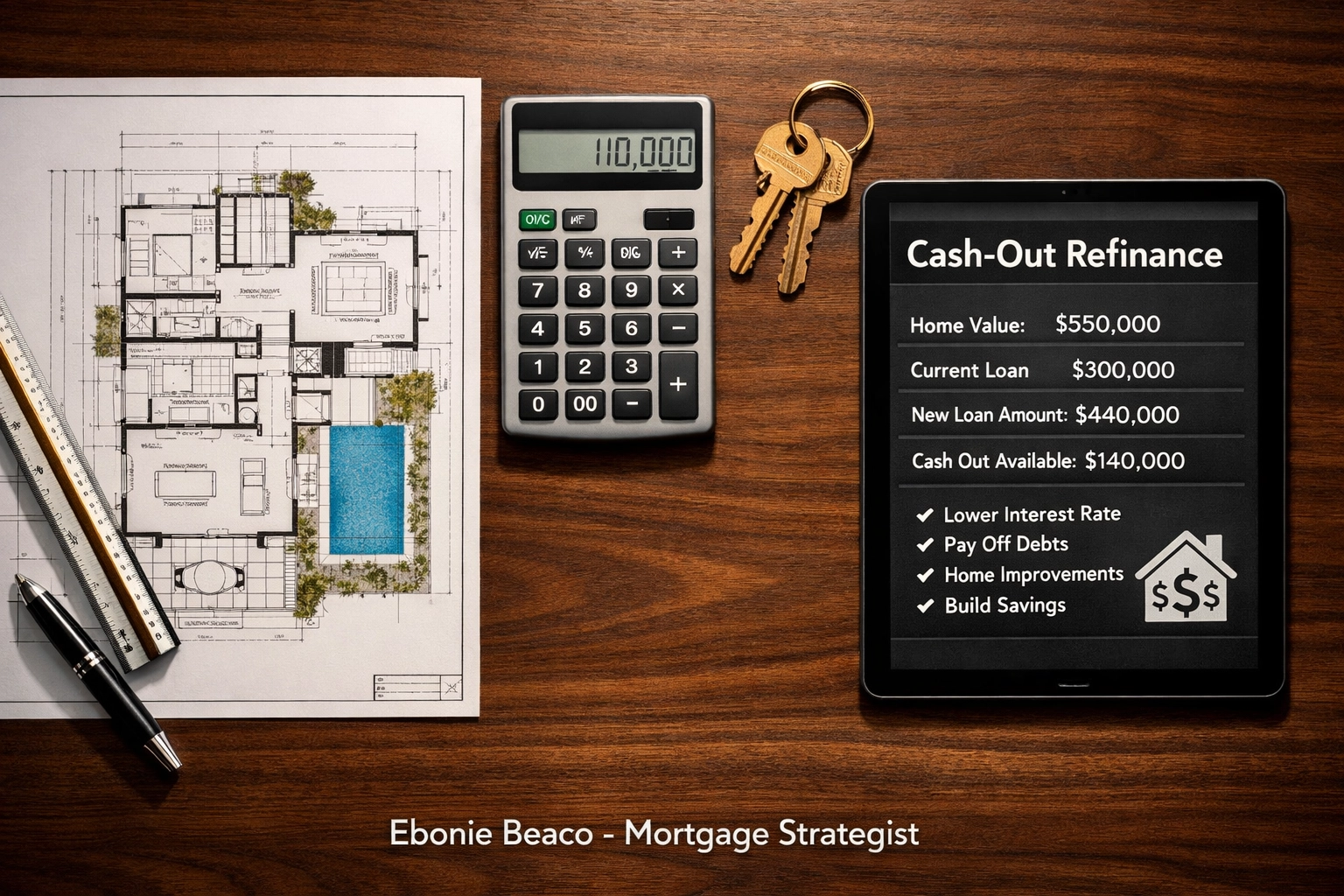

The Homeowner Strategy: Accessing Equity

While the 16% surge includes a lot of new buyers, we are also seeing a significant amount of activity from current homeowners in states like Michigan and Indiana. If you have been sitting on a house for a few years, you likely have a significant amount of equity.

With rates dipping, many are looking at a Cash-Out Refinance. This is a strategy where you replace your existing mortgage with a new, larger loan and take the difference in cash. In a market where inventory is tight, using that cash to renovate your current home or as a down payment on an investment property in Georgia or Alabama is a smart move.

Consider this scenario:

- Property Value: $450,000

- Current Mortgage Balance: $250,000

- Max LTV (80%): $360,000

- Available Cash for Reinvestment: $110,000 (minus closing costs)

By accessing this $110,000, a homeowner in a city like Virginia Beach could potentially fund a fix-and-flip project or secure a down payment for a duplex in a growing Michigan suburb.

The Investor Play: DSCR and Short-Term Rentals

For the real estate investors we work with at Home Loans Network, this rate dip is a tactical advantage. If you are an Airbnb host in Florida or a landlord in California, the cost of debt is a primary factor in your monthly cash flow.

Many investors are shifting toward DSCR Investor Loans. Because these loans focus on the property's income, the recent dip to 7.02% makes the "math work" on properties that might have been marginal just a month ago. When the interest expense goes down, your Debt Service Coverage Ratio improves, making it easier to secure funding and scale your portfolio.

If you are a BRRRR investor (Buy, Rehab, Rent, Refinance, Repeat), this surge in activity suggests that the "Refinance" part of your strategy just got a little bit more profitable. Locking in a rate in the low 7s, or even high 6s depending on your specific scenario, can significantly impact your long-term ROI.

Regional Market Highlights

The impact of this week's news varies depending on where you are looking to buy or refinance.

- Chicago and Illinois: We are seeing a steady demand for multi-unit apartment buildings. Investors are using bridge loans to acquire distressed properties, then moving into long-term financing as rates soften.

- Florida and Georgia: Short-term rental financing remains a hot topic. With more travelers looking for unique stays, investors are jumping back in to grab properties before the spring season fully kicks off.

- California and Virginia: Higher property values mean that even a small dip in rates results in a large monthly savings. This is driving a lot of interest in Jumbo Loans.

Why the Window Might Be Short

Market volatility is the name of the game in 2026. While the 16% surge shows that there is plenty of pent-up demand, these "rate windows" can close quickly. Economic shifts or changes in central bank policy can push rates back up just as fast as they came down.

This is why transparency is one of our core values. We want you to see the market for what it is. If the numbers make sense for your investment goals or your family’s budget at 7.02%, it is often better to move forward than to gamble on a further drop that may not come.

Jump in and see what your numbers look like right now.

How to Prepare for Your Next Move

Whether you are a wholesaler in Arkansas or a developer in Alabama, being ready to move when rates dip is essential. Here is a quick checklist to make sure you can take advantage of the next surge:

- Check your credit score: Even in a "down" week for rates, the best pricing goes to those with the strongest profiles.

- Organize your documents: If you are self-employed, have your last 12-24 months of bank statements ready for a Non-QM loan application.

- Know your equity: Use a mortgage calculator to estimate how much you can realistically pull out of your current properties.

- Connect with a strategist: Don't just talk to a "loan officer": talk to someone who understands how real estate investment actually works.

The recent 16% surge in applications is a clear signal that the market is ready to move. If you have been waiting for the right moment to refinance your primary residence, fund a fix-and-flip, or acquire your next rental property, this week has shown us that the opportunity is there for those who are prepared.

Access our online forms to get started on your pre-approval.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664