Monday’s Mortgage Update: How Today’s Economic Data Impacts Your Home Loan Strategy

Navigating the mortgage market requires a sharp eye on economic indicators that shift by the hour. Today is Monday, May 25, 2026, and the financial landscape is reacting to several key data points that influence how you buy, refinance, or invest in real estate. Whether you are a first-time homebuyer in Virginia or a seasoned investor scaling a portfolio in Florida, understanding these shifts is essential for your success.

The current economic climate is defined by a delicate balance between cooling inflation and a resilient labor market. This environment creates both challenges and opportunities for borrowers across the country. In states like Illinois and Michigan, we are seeing localized trends that demand a specific financing approach to ensure long-term wealth preservation.

Understanding Key Economic Indicators

To manage your home loan strategy effectively, you must speak the language of the market. Economic reports serve as the compass for interest rate movements. When inflation data comes in higher than expected, the market typically anticipates a more restrictive policy from the Federal Reserve, which can lead to higher mortgage rates.

Consumer Price Index (CPI): A measure that examines the weighted average of prices of a basket of consumer goods and services.

Investors monitor this report to gauge inflation trends because high CPI readings often lead to increased mortgage rates.

Federal Funds Rate: The interest rate at which depository institutions lend reserve balances to other depository institutions overnight.

While this does not directly set mortgage rates, it influences the broader interest rate environment and the cost of borrowing for lenders.

Personal Consumption Expenditures (PCE): A measure of the prices that people in the United States pay for goods and services.

The Federal Reserve prefers this metric for tracking inflation, making it a critical indicator for future rate adjustments.

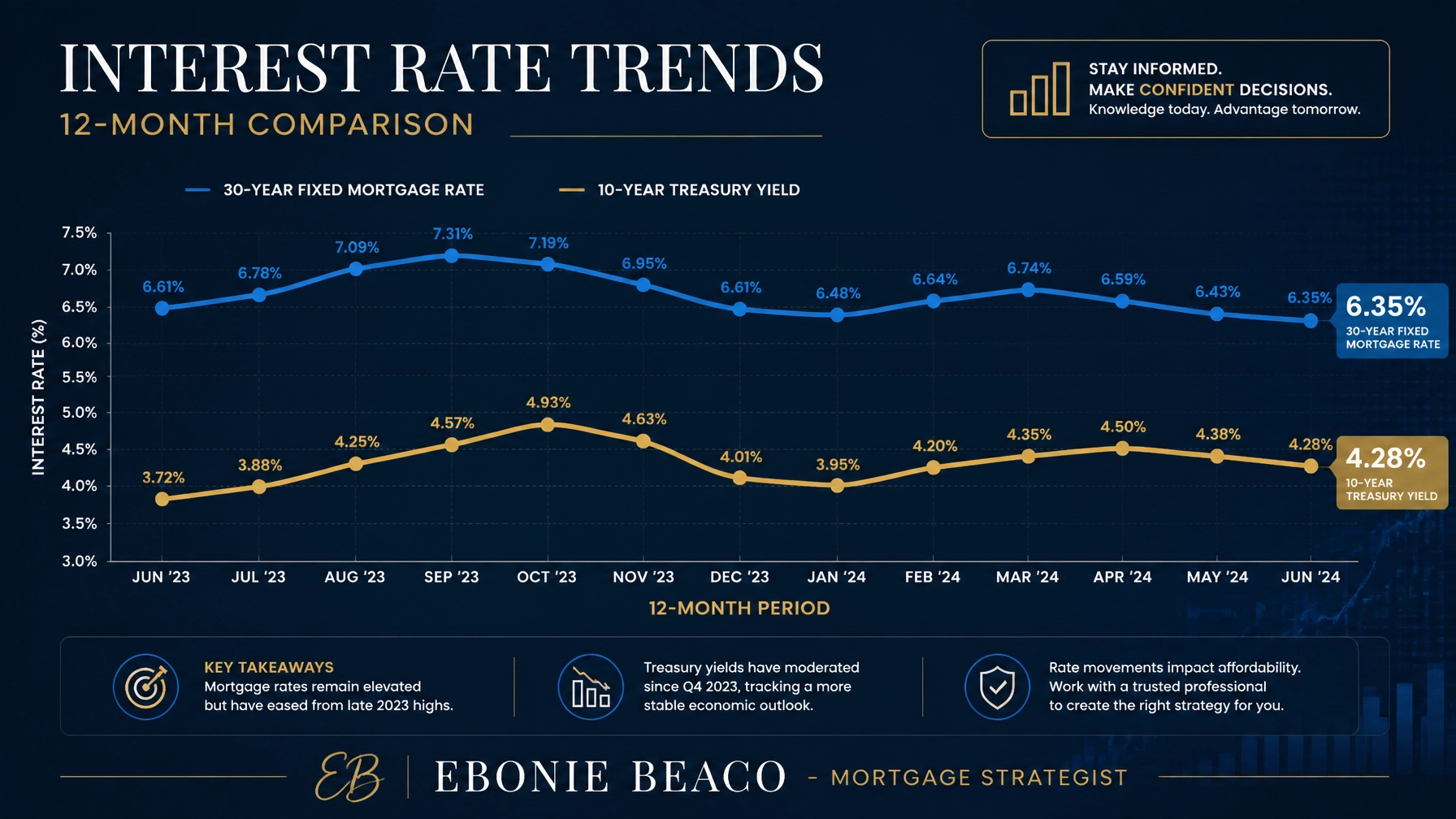

The Current State of Mortgage Rates

As we move through May 2026, mortgage rates are finding a new equilibrium. After a period of volatility in 2024 and 2025, the market is showing signs of stabilization. This stability allows homeowners in California and Georgia to plan their next moves with greater confidence.

Explore the current trends and you will see that while rates are lower than their recent peaks, they remain higher than the historical lows of the early 2020s. This "new normal" requires a more strategic approach to financing. Jump in and compare your options, as even a small difference in your rate can save you thousands of dollars over the life of your loan.

According to recent data from Freddie Mac, the 30-year fixed-rate mortgage is currently averaging around 6.37%. This level is noticeably improved from the highs seen in previous years. For residents in Alabama and Arkansas, this dip provides a window of opportunity to lock in a more favorable rate before the next economic report drops.

Strategic Financing for Real Estate Investors

Investors often play by a different set of rules than traditional homebuyers. If you are building a rental portfolio in Missouri or Indiana, you likely focus on cash flow rather than just the lowest interest rate. This is where specialized loan products come into play.

DSCR (Debt Service Coverage Ratio) Loan: A mortgage specifically for investment properties that qualifies the borrower based on the property’s rental income rather than personal income.

This program is perfect for investors who want to scale their portfolios without being limited by their personal debt-to-income ratios.

Fix and Flip Financing: Short-term funding used by investors to purchase and renovate a property before selling it for a profit.

These loans provide the necessary capital for quick acquisitions and construction costs in competitive markets like Chicago.

Bridge Loan: A temporary loan used to provide immediate cash flow while waiting for permanent financing or the sale of an existing property.

Investors use bridge loans to secure deals quickly and avoid losing out to cash buyers in hot markets like Florida.

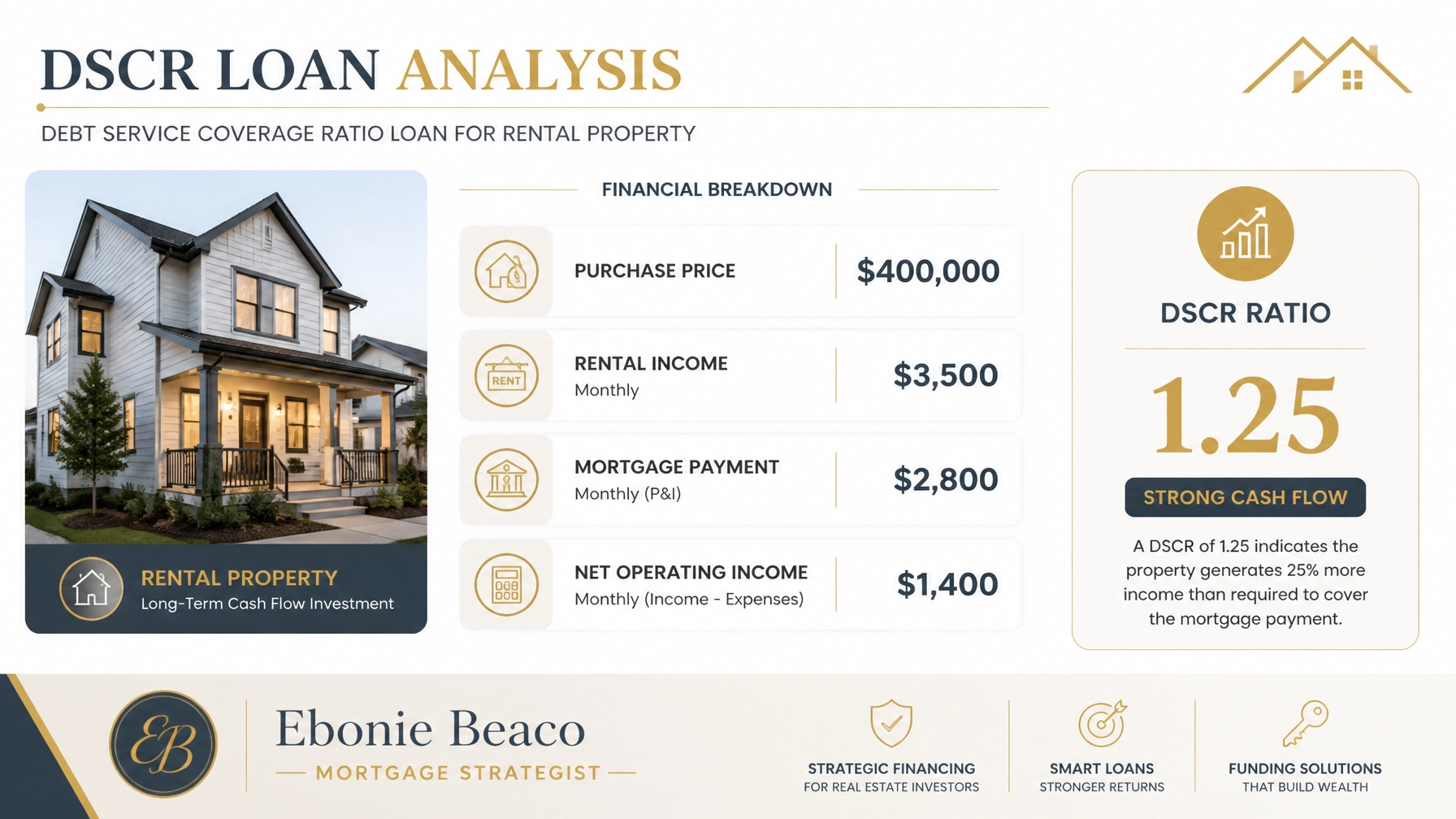

Case Study: Scaling with a DSCR Loan

Consider an investor in Atlanta, Georgia, who is looking to purchase a multi-unit property. By using a DSCR loan, the lender focuses on the property's ability to cover the mortgage payment through its rental revenue.

In this scenario, the investor identifies a duplex priced at $400,000. The projected monthly rental income is $3,500, while the total mortgage payment (including taxes and insurance) is $2,800. The resulting DSCR ratio is 1.25, which meets the standard requirement for most investor programs. Accessing this type of financing allows the investor to keep their personal credit lines open for other opportunities.

Leveraging Home Equity for Homeowners

For current homeowners in Virginia and Kentucky, your property might be your most valuable financial tool. As home values have climbed, many owners find themselves sitting on significant amounts of equity. Tapping into this equity can fund home improvements, debt consolidation, or even the down payment on a second home.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home as needed.

It functions similarly to a credit card but uses your home as collateral, typically offering much lower interest rates than unsecured debt.

Cash-Out Refinance: A new mortgage for an amount greater than what you owe, with the difference paid to you in cash.

This is a popular strategy for homeowners looking to lock in a fixed rate on a larger sum of money for long-term projects.

Loan-to-Value (LTV) Ratio: A financial term used by lenders to express the ratio of a loan to the value of an asset purchased.

Lenders use the LTV ratio to determine the risk level and the maximum amount you can borrow against your home's equity.

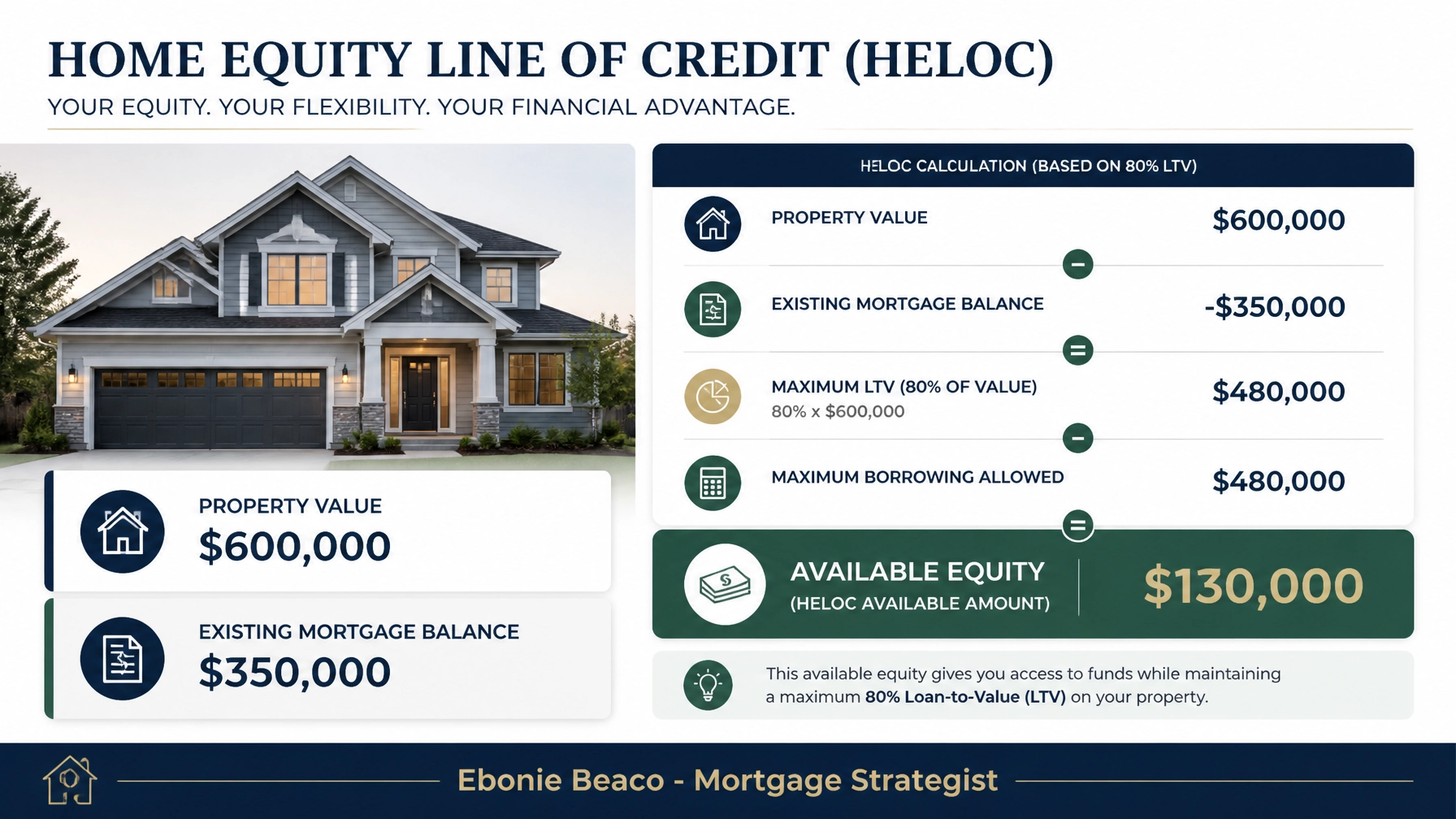

Calculating Your Available Equity

If you own a home in a growing market like Northern Virginia or coastal Florida, your equity has likely increased over the last few years. Calculating how much you can access is the first step in your home equity strategy.

Let's look at a homeowner in Alexandria, Virginia. Their home is currently valued at $600,000, and they have an existing mortgage balance of $350,000. Most lenders allow you to borrow up to 80% of your home's total value. By multiplying $600,000 by 0.80, we find a total allowable debt of $480,000. Subtracting the existing mortgage of $350,000 leaves the homeowner with $130,000 in available equity to use for their next big move.

The Rise of Short-Term Rental Financing

The Airbnb and short-term rental (STR) market remains a powerhouse in states like Florida and California. Financing these properties requires a lender who understands the unique income patterns of vacation rentals. Traditional lenders often struggle with the seasonal nature of STR income, but specialized Non-QM loans are designed exactly for this purpose.

Compare the income potential of a traditional long-term rental with a well-managed STR in a tourist destination. A property in Orlando might generate $5,500 in monthly revenue during peak seasons. Even with higher operating costs of $1,800, the net income of $3,700 often far exceeds what a standard lease could provide. Explore our short-term rental programs to see how you can qualify using the projected STR income rather than just standard lease rates.

Success in the Fix and Flip Market

Competitive markets like Chicago and Detroit offer incredible opportunities for investors who can breathe new life into distressed properties. The key to a successful flip is speed and reliable capital.

An investor in Chicago might acquire a property for $200,000 using a fix and flip loan. With $75,000 in renovations, the property’s value could rise to $350,000. These loans often cover a significant portion of both the purchase price and the renovation costs. This strategy allows you to leverage your capital across multiple projects simultaneously, maximizing your annual returns.

Why Your Strategy Should Change with the Data

Economic reports are not just numbers on a screen; they are signals that tell you when to act. If the job market stays strong, interest rates may remain elevated for longer to curb inflation. Conversely, any sign of economic cooling could lead to a quick dip in rates.

Stay informed by checking resources like the Bureau of Labor Statistics for employment updates and the Bureau of Economic Analysis for GDP and PCE reports. These official sources provide the raw data that market analysts use to forecast future rate movements.

Whether you are looking to purchase your first home in Missouri or cash out equity from a portfolio in California, the right mortgage strategist will help you navigate these fluctuations. We focus on aligning your financing with your long-term wealth goals, ensuring that every move you make is a step toward financial freedom.

The mortgage market of 2026 is full of nuance. While general headlines provide a broad overview, your specific situation in states like Indiana or Alabama requires a personalized touch. Education and transparency are the foundations of a solid real estate strategy.

Take the time to analyze your current mortgage terms and your future goals. Is it time to refinance? Should you tap into your equity? Could a DSCR loan help you scale? The answers to these questions depend on the data we see today and the goals you have for tomorrow.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664