Monday Morning Mortgage Pulse: How Today’s Rate Shifts Impact Your Illinois and Indiana Investment Strategy

Navigating the real estate landscape in late May 2026 requires a steady hand and an eye for long-term trends. As of today, Monday, May 25, the mortgage market has settled into a sideways pattern that offers both predictability and caution for savvy investors. While the volatility of early spring has largely subsided, current borrowing costs remain at a level that demands precise underwriting for any new acquisition.

Understanding the "pulse" of the market today involves looking past the headlines and into the granular data of the Midwest. In major hubs like Chicago and suburban centers across Indiana, the cost of capital is the defining variable for cash flow. This editorial breakdown explores the specific rate shifts seen this morning and how you can align your financing strategy with these new market realities.

The Current State of the Market: Late May 2026

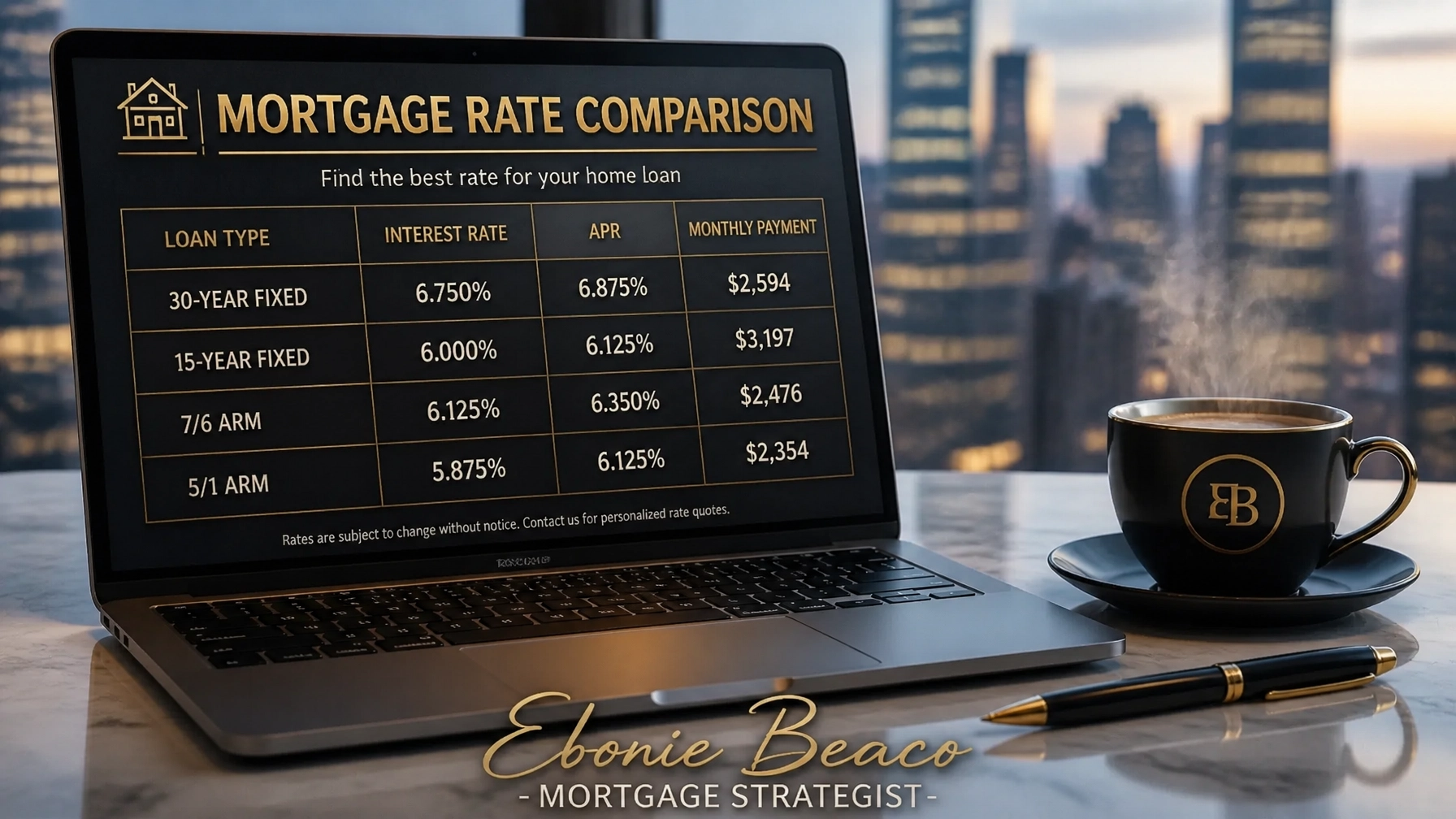

National mortgage averages for the 30-year fixed-rate loan are currently hovering near 6.4% interest, according to the latest NerdWallet mortgage reports. This stability is a welcome sight after the fluctuations seen in March, yet it keeps the APR around 6.46% for most conventional borrowers. For those looking at a 15-year fixed product, rates are more competitive, sitting just below the 6.0% threshold at roughly 5.95%.

In Illinois, the pricing is slightly more localized, with 30-year fixed rates frequently quoted between 6.6% and 6.8% depending on the specific lender and property type. Borrowers in the Chicago metropolitan area often see a small premium on these rates, especially when financing multi-unit properties or non-owner-occupied investments. You can explore more detailed state-specific data at Rocket Mortgage's Illinois rate index.

Indiana continues to reflect the national average more closely, making it an attractive destination for investors seeking lower entry costs. While specific quotes for the Hoosier State generally align with the mid-6% range, the lower property taxes in many Indiana counties help offset the higher interest costs. This regional advantage allows for stronger cash-on-cash returns even in a higher-rate environment.

Explore our full range of loan programs to see how these current rates apply to your specific financial profile.

Technical Definitions for the Modern Investor

- DSCR (Debt Service Coverage Ratio): A financial metric used to evaluate a property's ability to cover its own debt payments based on its rental income. Use this calculation to qualify for a loan without relying on your personal W-2 income.

- HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home as needed. Access this flexible funding to pay for renovations or as a down payment on your next investment property.

- Cash-Out Refinance: A mortgage refinancing option where the new loan is for a larger amount than the existing one, allowing the borrower to take the difference in cash. Leverage this strategy to pull tax-free equity out of a property that has appreciated in value.

- Non-QM (Non-Qualified Mortgage): A type of loan designed for borrowers who do not meet the traditional criteria of a standard mortgage, such as the self-employed or those with unique income structures. Explore these options if you need a mortgage but do not have a traditional salary or pay stubs.

Strategy 1: The Landlord Edge with DSCR Loans in Chicago

For investors targeting the Chicago rental market, DSCR Investor Loans have become the primary vehicle for scaling portfolios. Because these loans focus on the property's income rather than the borrower’s personal debt-to-income ratio, they provide a streamlined path for acquisition. In the current 6.6% rate environment, a 2-to-4 unit building in neighborhoods like Logan Square or Avondale can still cash flow if the rent-to-price ratio is managed correctly.

Landlord Loans structured through the DSCR model typically require a 20% to 25% down payment, but they allow for faster closings and fewer documentation hurdles. As rates stay sideways, the key is to ensure the DSCR ratio remains above 1.20x to 1.25x to secure the best possible terms. This means the gross rental income should be at least 20% higher than the total mortgage payment, including taxes and insurance.

Jump in and review our Chicago neighborhood market reports to identify which zip codes currently offer the strongest rental yields for your next project.

Strategy 2: Tapping Suburban Equity in Indiana

Homeowners in Indiana cities like Indianapolis, Fort Wayne, and Carmel have seen significant equity growth over the last three years. Even with current interest rates in the mid-6% range, a HELOC can be a brilliant tool for seasoned property owners. Instead of refinancing a low-rate primary mortgage, a HELOC sits as a second lien, allowing you to access only the funds you need when you need them.

Many investors use these funds to bridge the gap between properties or to fund extensive "value-add" renovations. Because Indiana’s housing market remains relatively affordable, a modest line of credit can often cover the entire renovation budget for a distressed property. This "buy, rehab, rent, refinance" (BRRRR) cycle is still highly effective when powered by smart equity management.

Compare your potential equity access using our mortgage calculators to see how much you could unlock from your current residence.

Strategy 3: Fix-and-Flip Financing for Community Revitalization

The demand for updated, turnkey homes remains high across the Midwest, from Gary, Indiana to the south side of Chicago. Fix and Flip Loans provide the short-term capital needed to purchase and renovate these properties quickly. Unlike traditional 30-year mortgages, these are interest-only bridge loans designed to be paid off within 12 to 18 months once the property is sold.

Investors are currently focusing on "micro-flips" where the renovation timeline is short, minimizing the total interest paid during the hold period. Even with bridge loan rates typically being 2% to 4% higher than conventional rates, the profit margins in these markets remain robust due to the scarcity of high-quality inventory. Successful flippers in 2026 are those who focus on high-impact upgrades that drive appraisal value.

Explore how Fix and Flip financing can accelerate your project timeline and help you secure properties that traditional lenders might overlook.

A Financial Example: The Illinois Multi-Unit DSCR Deal

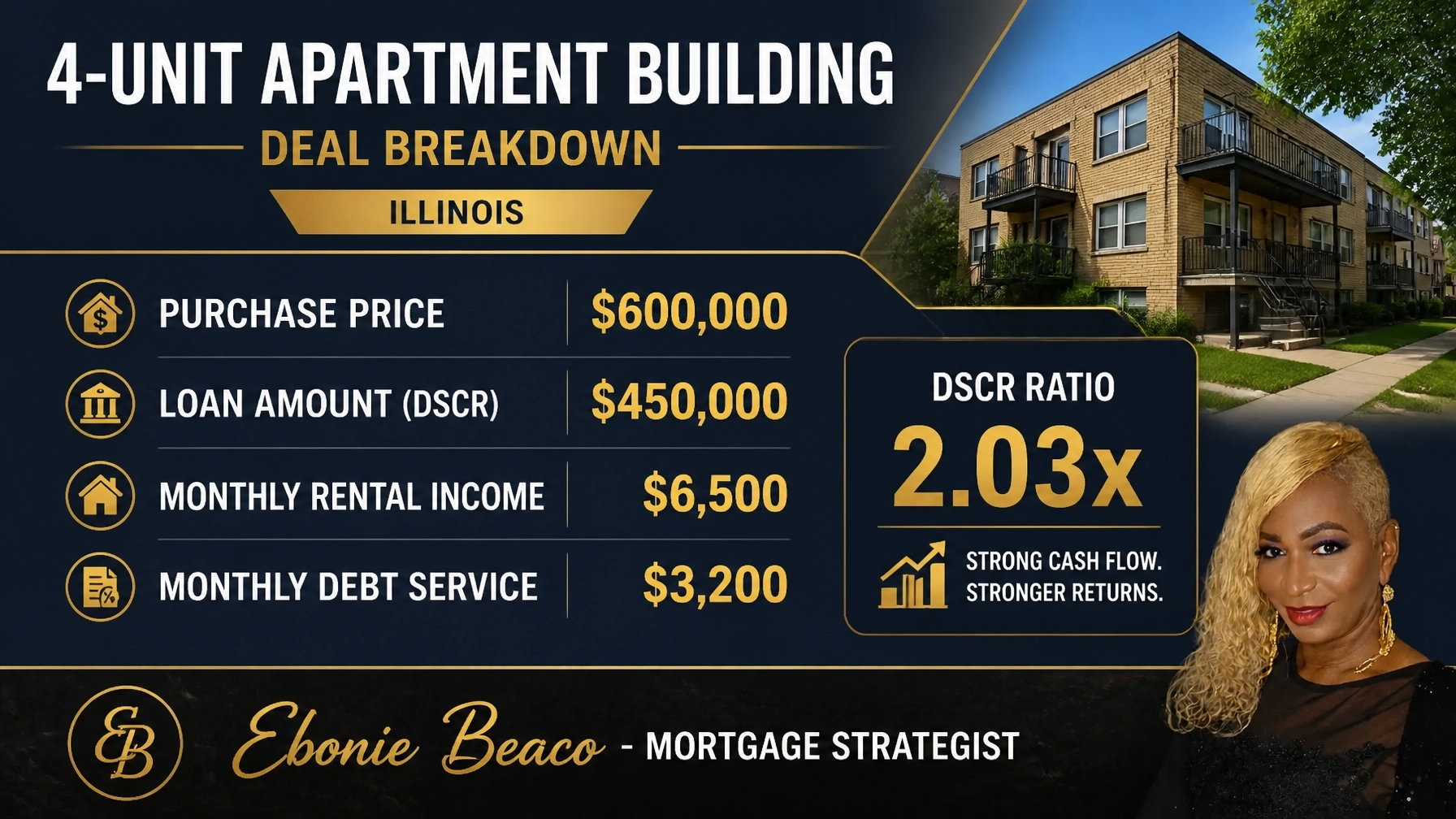

To illustrate how today's rates impact a real-world transaction, let's examine a 4-unit apartment building in a appreciating Illinois submarket. In this scenario, the investor is looking to use a DSCR loan to acquire the property without using personal income for qualification.

- Purchase Price: $600,000

- Down Payment (25%): $150,000

- Loan Amount: $450,000

- Interest Rate: 6.75% (30-Year Fixed)

- Monthly Rental Income (Total): $6,500

- Monthly Principal & Interest: $2,918

- Monthly Taxes & Insurance: $282

- Total Monthly Debt Service: $3,200

In this calculation, the DSCR Ratio is $6,500 divided by $3,200, which equals 2.03x. A ratio this high is excellent, as most lenders only require a 1.20x to qualify. This property would likely qualify for some of the most competitive terms available in the Non-QM space today.

Access our soft pull credit request to see what rates you might qualify for without impacting your credit score.

Aligning Your Strategy for the Months Ahead

As we move toward the summer of 2026, the "higher for longer" narrative continues to hold steady. While some analysts predict a slight softening of rates in late Q3, betting on a dramatic drop is not a sound investment strategy. Instead, focus on properties that make financial sense at today’s mid-6% levels. If rates do eventually fall into the 5% range, you can always execute a rate-term refinance to further improve your cash flow.

Whether you are a first-time homebuyer in Virginia, a landlord in Michigan, or a commercial developer in Florida, the fundamentals of real estate financing remain the same. Education and transparency are the best defenses against market uncertainty. By staying informed about daily rate shifts and regional trends, you can make decisions that align with your long-term wealth-building goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664