Missouri Refinance Alert: Why the 27% Drop in Applications is a Warning Sign

The Missouri mortgage landscape shifted abruptly this March.

Data indicates that refinance applications plummeted by 27% as average interest rates climbed to 6.5%.

According to reports from HousingWire, this cooling trend reflects a broader national tightening, but the impact on the Missouri market is particularly acute.

As a mortgage strategist, I view this sudden drop not just as a statistic, but as a significant warning sign regarding market liquidity and homeowner psychology.

When the volume of refinance activity retracts this sharply, it suggests that the "easy money" era has officially exited the building.

Homeowners and real estate investors in St. Louis, Kansas City, and Springfield must now pivot their strategies to account for a high-rate environment that shows no immediate signs of retreating.

Understanding the Liquidity Crunch

Liquidity refers to the ease with which assets can be converted into cash without affecting their market price.

In real estate, liquidity is often tied to the ability of homeowners to access the equity sitting in their walls through financing.

A 27% drop in applications signals a "liquidity freeze" where homeowners feel trapped by their current low-interest primary mortgages.

If you are holding a 3% or 4% interest rate from 2021, the prospect of refinancing into a 6.5% loan feels like a backward move.

However, avoiding the market entirely can lead to missed opportunities for debt consolidation or portfolio expansion.

Visual: A realistic image of a professional office desk with a calculator, a pair of glasses, and a Missouri real estate market report, conveying a sense of strategic analysis. "Ebonie Beaco - Mortgage Strategist" is written at the bottom.

The Psychology of the 6.5% Rate Barrier

For the past several years, 6% was seen as a psychological "ceiling" that many expected the market to stay under.

Crossing the 6.5% threshold has triggered a massive standoff between lenders and consumers.

Homeowners are choosing to "wait it out," but this waiting game carries its own set of risks.

As a strategist, I analyze the Cost of Inaction.

If you need capital to repair a property or pay off high-interest credit card debt, waiting for rates to drop while your debt compounds can be a fatal financial error.

Comparing the Cash-Out Refinance and the HELOC

When refinance applications drop, savvy property owners shift their focus to alternative equity access tools.

Cash-Out Refinance: This is a new first mortgage that replaces your existing loan and provides a lump sum of cash at closing.

Practical Application: Best used when your current mortgage rate is already near market averages or if you need a large, fixed-rate sum.

HELOC (Home Equity Line of Credit): This is a second mortgage that functions like a credit card secured by your home.

Practical Application: Best used to preserve a low interest rate on your first mortgage while still accessing equity for specific projects.

In Missouri, where property values have remained relatively stable compared to the coastal volatility, the equity is there.

The question is how you extract it without destroying your overall weighted average cost of capital.

Financial Strategy Example: The Missouri Equity Play

Let's look at a real-world scenario for a homeowner in St. Louis.

Current Situation:

- Current Home Value: $450,000

- Existing First Mortgage: $200,000 at 3.25%

- Desired Capital for Investment: $100,000

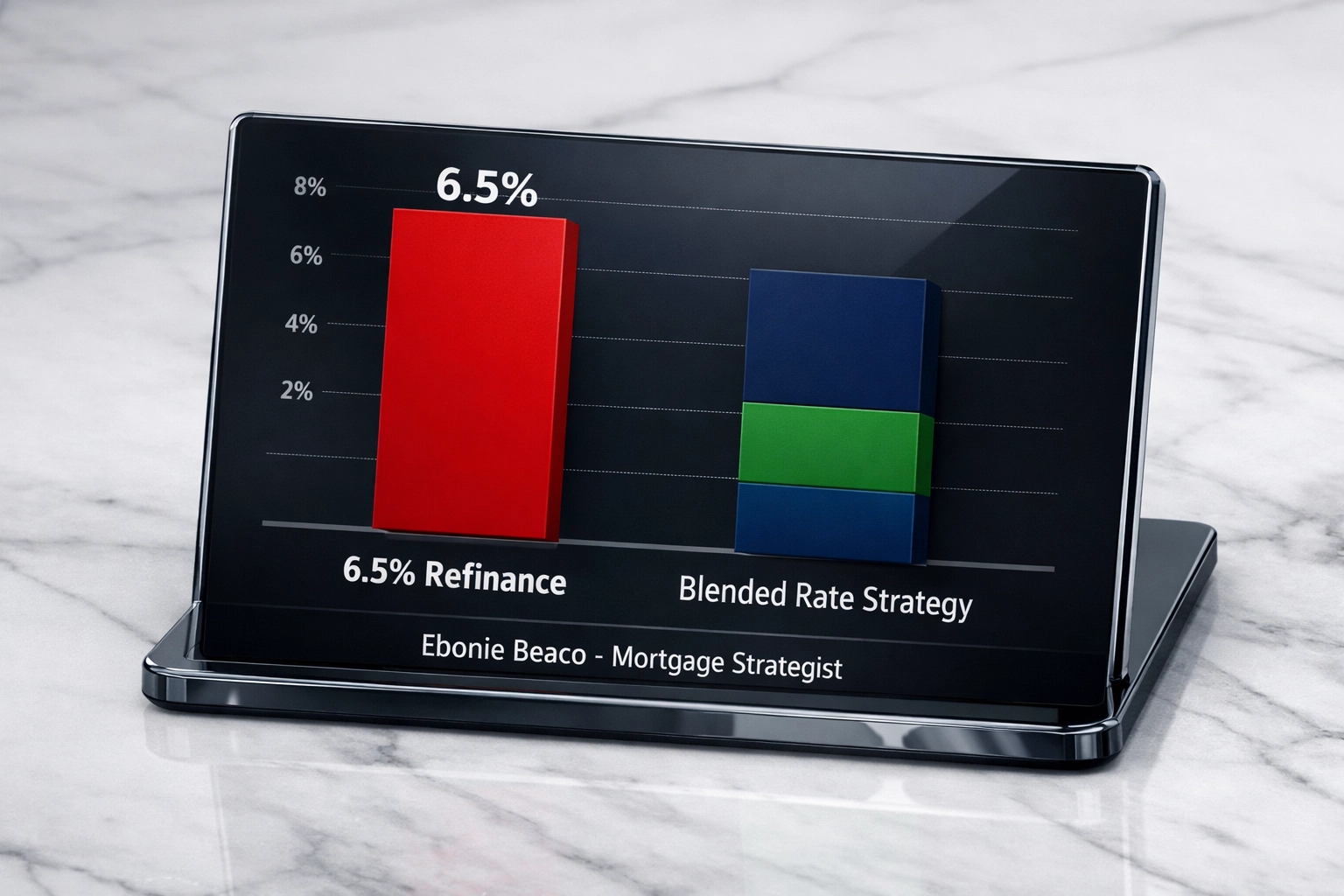

Option A: Full Cash-Out Refinance

If the homeowner refinances the entire $300,000 into a new loan at 6.5%, their monthly principal and interest payment jumps significantly because they are losing the 3.25% rate on the original $200,000.

Option B: The HELOC Strategy

The homeowner keeps the $200,000 loan at 3.25%. They take out a $100,000 HELOC as a second lien. Even if the HELOC rate is 9%, the "blended rate" of their total debt is still far lower than 6.5%.

Visual: A financial chart comparing the monthly payments of a 6.5% Cash-Out Refinance versus a Blended Rate strategy (3.25% First + 9% HELOC), showing the cost savings of the HELOC strategy. "Ebonie Beaco - Mortgage Strategist" is written at the bottom.

Warning for Real Estate Investors and Wholesalers

If you are an investor in Missouri, Illinois, or Indiana, the 27% drop in refinance applications is a leading indicator of a slowing purchase market.

When homeowners cannot refinance, they cannot easily move.

This leads to lower inventory, which keeps prices high but makes transactions sluggish.

For those using the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), the refinance stage just became significantly more expensive.

To maintain your margins, you must look toward DSCR Loans.

DSCR (Debt Service Coverage Ratio) Loan: A mortgage product for investment properties that qualifies the borrower based on the property’s rental income rather than personal income or debt-to-income ratios.

Practical Application: Use this to scale your portfolio when your personal DTI (Debt-to-Income) ratio is maxed out.

Explore our loan programs to see how these investor-focused products can bypass the traditional refinance hurdles.

Why the 27% Drop Impacts the Midwest and South

While this specific alert focuses on Missouri, we are seeing similar ripples across Alabama, Arkansas, Georgia, Florida, Michigan, and Virginia.

The "Rate Protection Strategy" is now a necessity.

In states like Florida and Georgia, where insurance premiums are also rising, the combination of high rates and high carrying costs is squeezing cash flow.

Investors are now leaning heavily into Non-QM Mortgage Loans.

Non-QM (Non-Qualified Mortgage): A loan that does not follow the standard government-backed criteria, often used for self-employed borrowers or unique property types.

Practical Application: Allows for bank statement qualifying if you cannot show traditional tax return income.

Visual: A realistic image of a modern bank building in a clean, professional urban setting, representing the stability of institutional lending. "Ebonie Beaco - Mortgage Strategist" is written at the bottom.

The Role of the Mortgage Strategist

In a volatile market, you do not need a "loan taker"; you need a strategist.

A loan taker simply tells you what the rate is today.

A mortgage strategist looks at your total financial profile to determine how to leverage equity without compromising your long-term wealth.

This involves calculating your LTV (Loan-to-Value) and ensuring you have a "Rate Protection Strategy" in place for when the market eventually cycles back down.

LTV (Loan-to-Value): The ratio of the loan amount divided by the appraised value of the property.

Practical Application: Keeping your LTV under 80% generally helps you avoid PMI and secure better interest rates.

Moving Forward in a High-Rate Environment

The 27% drop in Missouri is a signal to stop waiting for the "perfect" time and start planning for the "current" reality.

If you are a homeowner, assess your equity now.

If you are an investor, tighten your buy-box and focus on properties that can support a 6.5% to 7.5% interest rate while still cash-flowing.

Jump in and review our mortgage basics to refresh your understanding of how these levers move.

Compare your options between a traditional refinance and a second lien strategy before the window of opportunity narrows further.

The liquidity in the market is drying up, and those who act with a clear strategy will be the ones who survive the crunch.

Action Steps for Missouri Homeowners and Investors

- Request an Equity Analysis: Determine exactly how much "dead equity" is sitting in your property.

- Calculate Your Blended Rate: Do not fear the headline interest rate; calculate what your total debt cost would be.

- Review DSCR Options: If you are an investor, see if your rental income can carry the weight of today's rates.

- Audit Your Debt: If you have high-interest consumer debt, a 6.5% mortgage is still a massive net win compared to 24% credit card interest.

Access our online forms to start the evaluation process.

The Missouri market is changing fast.

The 27% drop is a warning, but for the prepared, it is also a map.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664