Michigan's Mortgage Rate Reality: What 6.4% Means for Your Next Flip

Date: March 25, 2026

The Michigan real estate landscape shifted this week as mortgage rates hit a 2026 high of 6.4%. For the casual observer, a fractional increase in percentage points is a headline. For the professional fix and flip investor or wholesaler in Detroit, Grand Rapids, or Lansing, this shift represents a fundamental change in how you must structure your next deal.

When rates climb during the onset of the peak homebuying season, as reported by Real Estate News, the margin for error evaporates. As a mortgage strategist, I view this environment through the lens of risk management. Success in the current Michigan market requires moving beyond simple "buy low, sell high" mentalities and into the realm of structured finance and asymmetric risk protection.

Understanding Asymmetric Risk in Michigan Flipping

Asymmetric Risk: A scenario where the potential for loss and the potential for gain are unequal. In a rising rate environment, the risk often leans toward the downside if the holding period extends beyond the initial projection.

In a 6.4% environment, your carrying costs are higher, and your end buyer’s purchasing power is lower. This creates a "pincer effect" on your profit margins. If you do not account for the possibility of a longer "days on market" (DOM) cycle, your renovation profit can quickly be consumed by interest payments.

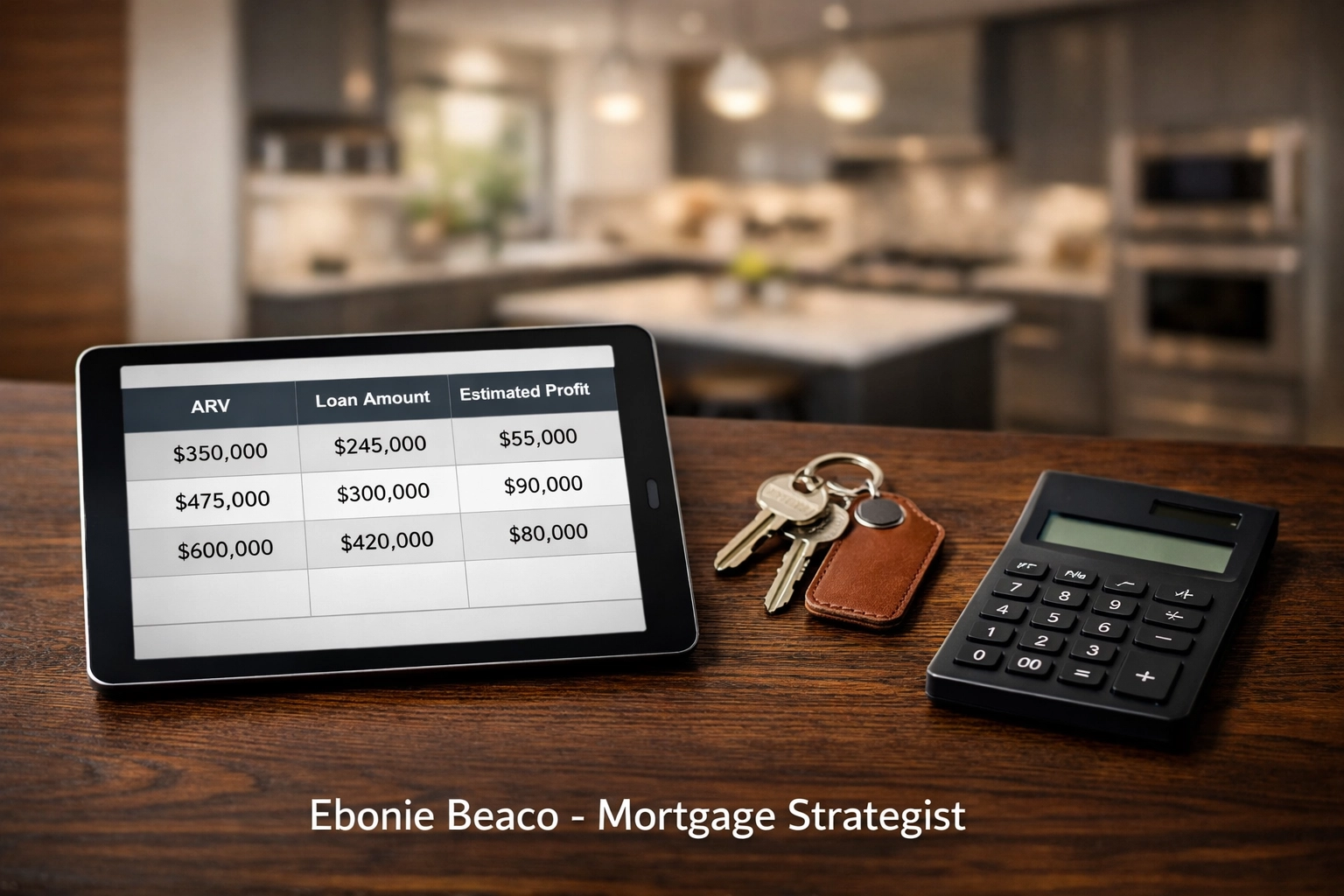

Explore the way you calculate your exit strategy. If your ARV (After Repair Value) was based on 5.5% rates from earlier in the year, you must recalibrate. Your buyer pool in cities like Ann Arbor or Kalamazoo has just seen their monthly payment appetite tighten.

Strategic Financing: Beyond the Standard Fix and Flip Loan

To navigate this 6.4% reality, Michigan investors must utilize diverse capital stacks. Relying solely on traditional financing is a recipe for stagnation. You need agility.

Bridge Loans

Bridge Loan: A short term loan used to provide immediate cash flow while permanent financing is secured or a property is sold. Application: Use a bridge loan to close a deal in 10 days or less when a wholesaler brings you a distressed property in Oakland County that requires an immediate commitment.

DSCR Loans

DSCR (Debt Service Coverage Ratio): A mortgage for investment properties where qualification is based on the property’s rental income rather than the borrower’s personal income. Application: If the Michigan flip market slows, your "Plan B" should be a pivot to a long term rental. A DSCR loan allows you to pull your capital out based on the lease agreement rather than your tax returns.

Quick-Close Financing

In competitive markets like Royal Oak or Grand Rapids, speed is a currency. Wholesalers often prioritize the certainty of a close over the highest offer price. Accessing capital that does not require a 45 day underwriting cycle allows you to negotiate deeper discounts on the front end, which offsets the 6.4% cost of capital on the back end.

Ebonie Beaco - Mortgage Strategist

Ebonie Beaco - Mortgage Strategist

Analyzing the Math: The Michigan Flip Scenario

Let's look at how a 6.4% rate environment influences a typical renovation project in a mid-market Michigan neighborhood.

The Scenario:

- Purchase Price: $160,000

- Renovation Budget: $55,000

- Holding Period: 6 Months

- Projected ARV: $295,000

At a 6.4% interest rate on a fix and flip line of credit (often priced at a premium above the prime or benchmark rate), your monthly interest only payment increases significantly compared to the 5% environment of previous years.

The Calculation Breakdown:

- Total Capital Deployed: $215,000.

- Monthly Carrying Cost (Interest Only): Approximately $1,146 (assuming a 6.4% rate).

- Total Holding Cost (6 Months): $6,876.

- Closing Costs and Commissions (Exit): $17,700 (6% of ARV).

- Projected Net Profit: $55,424.

Jump in and compare this to a 7.5% rate, which is common for higher risk bridge debt. Your holding cost would jump to $8,062. While $1,200 might not seem like a deal breaker, when you multiply that across a portfolio of five houses, you are looking at $6,000 in "lost" profit due to financing inefficiency.

Protecting Your Margins: Three Critical Strategies

As a mortgage strategist, I advise my clients in Michigan, Illinois, and Indiana to adopt these three tactics immediately to combat the 6.4% rate ceiling.

1. The "1% Contingency"

Always run your numbers with an exit rate 1% higher than the current market. If the deal still yields a 15% to 20% ROI at a 7.4% rate, the deal is resilient. If the deal only works at 6.4%, you are gambling on the Fed, not on the real estate.

2. Leverage Non-QM Options

Non-QM (Non-Qualified Mortgage): A loan that does not follow the traditional CFPB (Consumer Financial Protection Bureau) guidelines, often used for self-employed borrowers or investors using bank statements for income verification. Access these programs if you are a full time investor in Michigan whose tax returns do not reflect your true liquidity. This keeps your personal debt-to-income (DTI) ratio clean for future acquisitions.

3. Wholesale to Rental Pivot

If the "retail" buyer market in Michigan cools due to the 6.4% rates, do not force a sale. Explore the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method. By moving the property into a DSCR loan, you can wait out the rate cycle while the tenant pays down the principal.

Ebonie Beaco - Mortgage Strategist

Ebonie Beaco - Mortgage Strategist

Regional Context: Why Michigan is Unique

While I analyze markets across Florida, Georgia, and Virginia, Michigan offers a specific set of advantages even at 6.4%. The price-to-rent ratios in cities like Detroit and the surrounding suburbs remain some of the most favorable in the country for investors.

In high cost states like California or parts of Virginia, a 6.4% rate can make a $800,000 mortgage payment feel impossible. In Michigan, where the median home price is more accessible, the impact on the monthly payment is less likely to completely freeze the buyer market. This keeps the "exit" for flippers more fluid than in coastal markets.

Structure Your Capital Stack for Success

The goal for any serious real estate investor or wholesaler in the current climate is to maximize "dry powder." You do not want your capital trapped in a project that is sitting on the market.

Utilizing bridge loans for the acquisition and renovation phase, followed by a quick transition into a long term investment loan or a retail sale, is the standard for 2026.

For wholesalers in Alabama, Arkansas, and Missouri, the strategy remains the same: you must leave enough "meat on the bone" for your buyers to account for these higher financing costs. If you are wholesaling a deal in St. Louis or Birmingham, your underwriting must reflect the reality that your investor buyer is paying 6.4% or more for their money.

Conclusion

The 6.4% mortgage rate is not a barrier; it is a filter. It filters out the amateur "hobbyist" flippers and rewards the disciplined mortgage strategists who understand how to use leverage to their advantage.

Whether you are looking for a cash out refinance to fund your next Michigan acquisition, or you need a DSCR loan to stabilize a rental portfolio in Florida or Georgia, the structure of your debt is the most important component of your ROI.

Explore your options, analyze the asymmetric risk, and execute with precision.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Home Loans Network provides mortgage lending and real estate finance solutions across Alabama, Arkansas, Georgia, Florida, Illinois, Indiana, Michigan, Kentucky, Missouri, and Virginia. We specialize in DSCR loans, fix and flip financing, bridge loans, and home equity strategies for investors and homeowners.