Michigan HELOC Lender Secrets Revealed: The One Reason Your Bank Might Say No (and How We Say Yes)

You have spent years building equity in your home. You have seen property values rise across Michigan and Virginia, and you are ready to tap into that wealth to renovate, consolidate debt, or fund your next investment. You walk into your local big bank, confident in your application, only to receive a rejection letter a week later.

It is a common scenario. Many homeowners in states like Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Missouri, and beyond are finding that traditional lending institutions have set a bar so high it feels impossible to clear.

If you have been searching for a Michigan HELOC lender or a Virginia HELOC lender, you likely noticed that the big names in banking often have a very narrow "box" for approvals. When you do not fit perfectly inside that box, they simply say no.

We do things differently. By operating as a mortgage strategy hub with access to over 240 different lenders, we look for reasons to say yes where others see roadblocks.

The Rigid Barrier of the Debt-to-Income Ratio

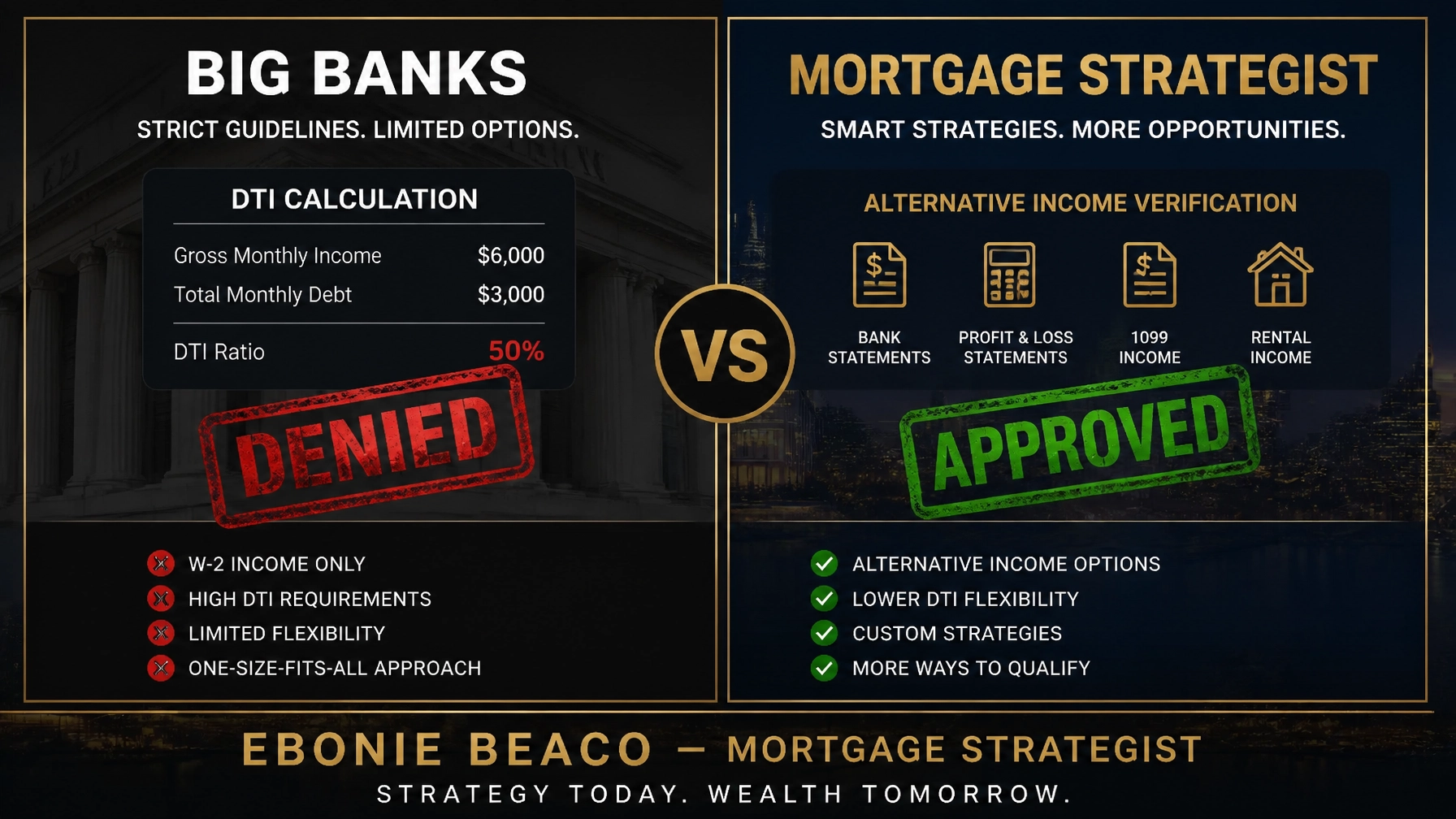

The primary reason most traditional banks say no to a Home Equity Line of Credit (HELOC) is a strict adherence to the Debt-to-Income ratio.

DTI (Debt-to-Income): A financial metric calculated by dividing your total monthly debt obligations by your gross monthly income.

Banks typically want to see a DTI at or below 43%. If you are a self-employed entrepreneur in Grand Rapids or a business owner in Richmond, your tax returns might show heavy write-offs. While these write-offs are great for your taxes, they can make your qualifying income look lower than it actually is.

Explore the possibility of using alternative documentation. We often utilize bank statement loans to verify income based on real cash flow rather than just the bottom line of a tax return. This allows us to provide financing to those who are financially strong but do not fit the traditional W-2 employee mold.

The Hidden Trap of Home Equity Caps

Even if your income is perfect, you might hit the equity wall. Most big banks cap your total borrowing at 80% of your home's value.

CLTV (Combined Loan-to-Value): The total percentage of all loans secured by a property compared to its appraised market value.

If you have a primary mortgage and want a HELOC, the bank adds both together. If that total exceeds 80%, you are often denied.

As a specialized Virginia HELOC lender, we have access to programs that allow for a higher CLTV, sometimes up to 85% or even 90% for qualified borrowers. This extra 5% to 10% can represent tens of thousands of dollars in liquidity that you can use for your goals.

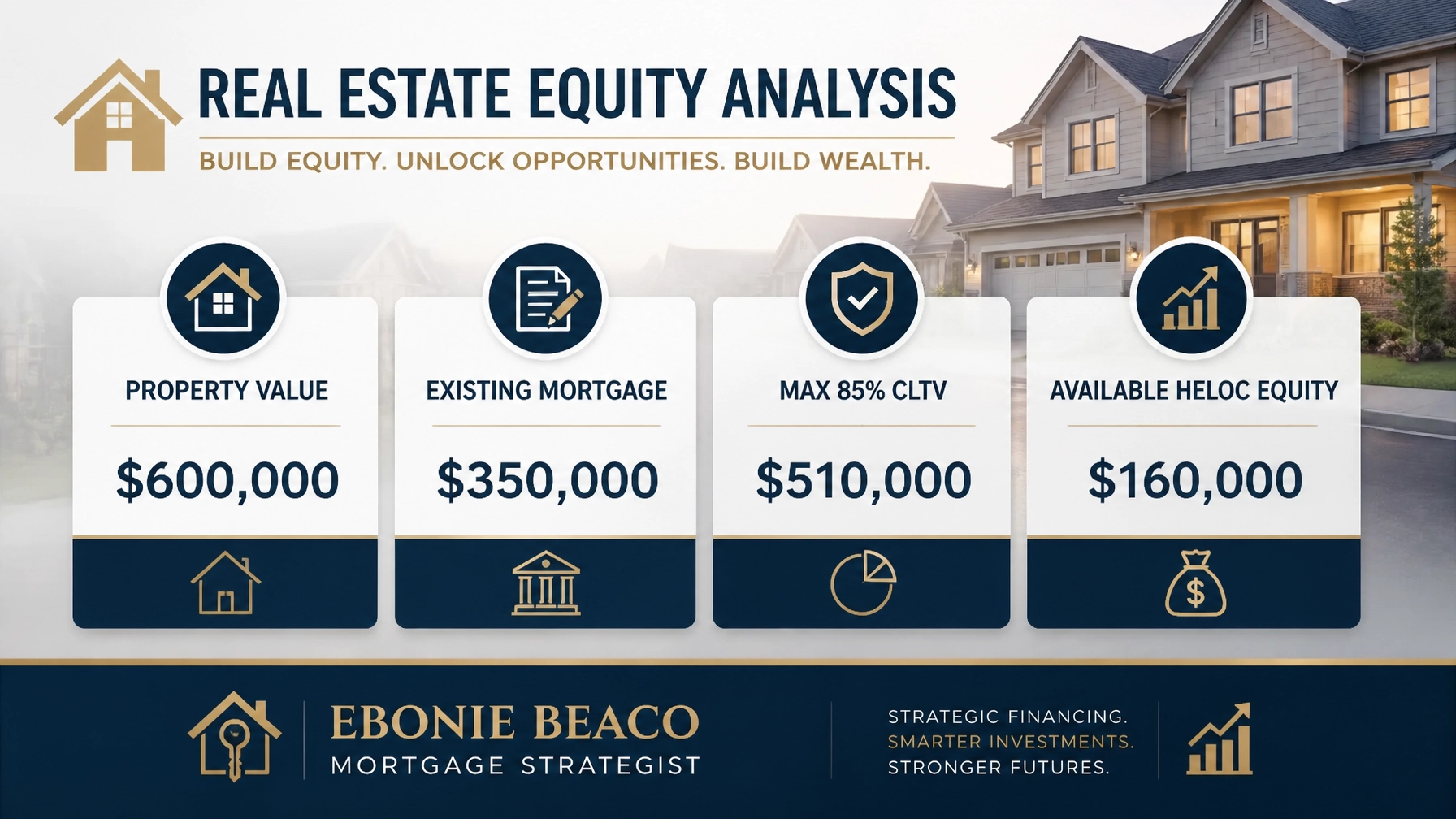

The Real-World Math of Equity Access

Let's look at how this works in practice. Many homeowners assume they have no options because their bank told them they reached their limit.

Imagine you own a home in a thriving market like Northern Virginia or a desirable suburb in Michigan.

The Calculation Example:

- Current Property Value: $600,000

- Existing First Mortgage Balance: $350,000

- The Bank's 80% Limit: $480,000 (Total available debt allowed)

- The Resulting HELOC: $130,000 ($480,000 minus $350,000)

Now, compare that to a strategy that allows for an 85% CLTV.

By increasing the allowed CLTV to 85%, the total allowable debt becomes $510,000. This increases your available HELOC to $160,000. That is an additional $30,000 in working capital simply by choosing a lender with more flexible guidelines. You can use our mortgage calculators to run these scenarios for your own property.

Why Your Bank Is Not the Only Option

Traditional banks operate on "overlays." These are extra rules they add on top of standard lending guidelines to reduce their risk. If a bank is "spooked" by the current economy, they might increase their credit score requirements or lower their DTI limits even further.

Jump in to a more diverse lending environment. Because we work with dozens of specialized wholesale lenders, we can shop your specific scenario. If one lender dislikes your high DTI, we find another that prioritizes your high credit score or significant equity.

Compare the traditional bank experience with a dedicated mortgage strategy. A bank has one product on the shelf. If you don't want it, or don't qualify for it, they have nothing else to offer. We treat financing as a puzzle, fitting the right pieces together to help you achieve homeownership or build wealth.

Leveraging HELOCs for Real Estate Investment

For real estate investors, a HELOC is often the "seed money" for a larger portfolio. Whether you are doing a Fix and Flip in Chicago or building a DSCR rental property portfolio in Florida, your primary residence is a powerful tool.

DSCR (Debt Service Coverage Ratio): A metric used to qualify a loan based on the rental income of the property rather than the borrower's personal income.

Many investors use a HELOC to provide the down payment for their next purchase. By accessing equity at a lower interest rate than a hard money loan, you can increase your cash flow on the new property.

We support investors across several states, including AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA. Whether you are looking for bridge loans, construction financing, or short-term rental funding for an Airbnb, the journey often begins with a strategic HELOC on your existing assets.

Access Professional Guidance in Michigan and Virginia

Geography should not limit your financial options. As a Michigan HELOC lender and Virginia HELOC lender, we understand the local market nuances. We know that a condo in Virginia Beach requires different handling than a single-family home in Ann Arbor.

Our commitment to transparency and education ensures you understand every step of the process. We break down the complicated mortgage terminology so you can make informed decisions. From HELOCs to cash-out refinances, we align your financing with your long-term wealth goals.

Access our full range of loan programs to see which solution fits your current needs. Whether you are a first-time homebuyer or a seasoned investor, we provide personal guidance every step of the way.

Stop letting a single "no" from a bank stall your progress. There is almost always a path forward when you have the right strategist in your corner.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664