May 27 Mortgage Update: Understanding Rate Volatility for Your Florida or California Home Search

Today is Wednesday, May 27, 2026, and the mortgage market continues to display the "choppy" behavior that has defined the late spring season. Over the last twenty four hours, we have seen a modest pullback in national averages, providing a slight reprieve for buyers who were sidelined by last week's sudden spike. While the broader trend remains elevated by historical standards, the daily movement suggests that bond investors are reacting to shifting energy prices and geopolitical headlines.

If you are currently searching for a home in high demand markets like Florida or California, understanding these micro shifts is essential for timing your lock or structuring your offer. The interaction between the 10-year Treasury yield and consumer mortgage rates remains the primary engine of movement this week. As the yield dipped toward 4.46% today, several lenders adjusted their pricing downward by roughly four to five basis points.

The National Mortgage Rate Snapshot: May 27, 2026

The 30-year fixed-rate mortgage for purchase transactions is currently hovering around 6.35% to 6.36% APR. This represents a notable decline from the levels seen at the start of the week. For those exploring shorter term financing, the 15-year fixed average sits at approximately 5.79% APR, remaining relatively stable despite the volatility in longer duration bonds.

Adjustable rate mortgages (ARMs), particularly the 5-year ARM, are quoting near 6.45% APR. This inversion between fixed and adjustable rates highlights the unique market conditions where investors are pricing in future rate cuts. According to recent data from Freddie Mac, the weekly survey through late May showed a slight uptick in the national average before this most recent four day cooling period began.

What is Driving the Current Rate Movement?

The primary catalyst for today’s movement is the recent easing of oil prices. Energy costs play a significant role in inflation expectations, and as WTI crude dropped under $90 per barrel, the market signaled a reduction in inflationary pressure. This shift allows bond yields to fall, which naturally pulls mortgage rates lower.

Geopolitical tensions, specifically the ongoing conflict involving Iran, continue to serve as a backdrop for market volatility. Reports of potential de-escalation or diplomatic reviews have helped calm the markets "down a hair" in recent trading sessions. However, until a definitive resolution is reached, headline driven swings remain a constant risk for anyone tracking mortgage rates for an upcoming purchase or refinance.

Florida Market Outlook: A Tale of Two Segments

In Florida, the housing market is currently exhibiting a fascinating bifurcation between single family homes and the condominium sector. While single family residences are seeing a spike in closed sales and a move toward market equilibrium, the condo market is increasingly favoring buyers. In many coastal regions, the supply of condos has exceeded nine months, driven by rising insurance premiums and new legislative requirements for structural reserves.

Investors and homeowners in the Sunshine State are frequently utilizing DSCR (Debt Service Coverage Ratio) loans to bypass personal income verification. With Florida's median home price stabilizing near $405,000, the math for rental property acquisitions has improved for those focusing on high growth areas like Orlando, Tampa, and Jacksonville. You can explore more about Florida real estate investing to see how these trends affect localized portfolios.

California Real Estate: Equity and Jumbo Strategies

The California market remains resilient, even as rates reached a seven month high earlier this spring. In markets like Malibu, Silicon Valley, and San Diego, the reliance on Jumbo Loans is high because property values consistently exceed conforming loan limits. A jumbo loan is a mortgage used to finance properties that are too expensive for a conventional conforming loan, typically requiring higher credit scores and significant cash reserves.

Many California homeowners are sitting on substantial equity and are choosing to access that wealth through HELOC (Home Equity Line of Credit) or Cash-Out Refinance options. This strategy allows owners to fund renovations or consolidate debt without sacrificing their existing low interest first mortgage. If you are navigating the luxury market in the Golden State, jumping in with a solid understanding of California real estate investing strategies is vital for long term wealth building.

Homeowner Equity Strategies: The Power of the HELOC

For homeowners who do not want to touch their primary mortgage rate, a HELOC provides a flexible way to tap into home equity. This revolving line of credit works much like a credit card but is secured by your property. This allows for a lower interest rate than most unsecured personal loans or credit cards.

Example Calculation:

Imagine a homeowner in Illinois or Georgia with a home valued at $500,000 and an existing mortgage balance of $280,000. If a lender allows an 85% combined loan-to-value (CLTV), the total available borrowing limit would be $425,000. Subtracting the $280,000 existing mortgage leaves $145,000 in available equity that can be accessed for investments or home improvements.

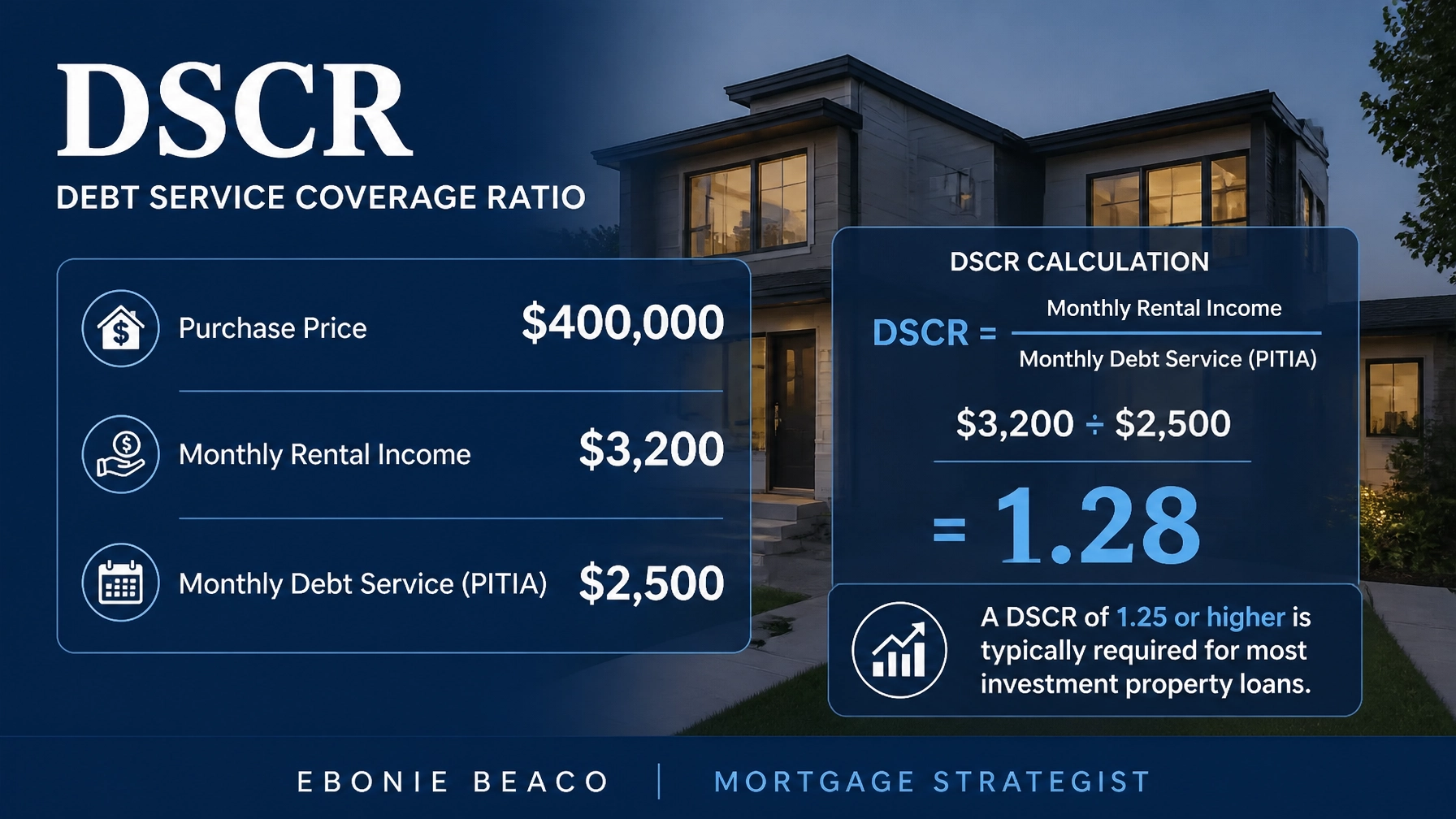

Real Estate Investing: Analyzing the DSCR Loan

Real estate investors across Alabama, Arkansas, Indiana, and Michigan are increasingly moving away from traditional W-2 based lending. The DSCR Investor Loan is a non-QM mortgage product where qualification is based solely on the property's ability to cover its own debt. This means your personal debt-to-income (DTI) ratio is not the primary factor in the approval process.

To calculate the DSCR, a lender divides the gross monthly rental income by the monthly PITIA (Principal, Interest, Taxes, Insurance, and Association dues). A ratio of 1.20 or higher is typically preferred, though some programs allow for lower ratios if the borrower has a strong credit profile. This product is a favorite for BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investors who want to scale their portfolios quickly.

Updates Across Other Key States

- Alabama and Arkansas: Inventory levels are beginning to rise, giving buyers more leverage in negotiations. Investors are finding success with fix and flip financing as distressed inventory hits the market in emerging suburban areas.

- Georgia and Virginia: The suburban markets around Atlanta and Northern Virginia remain competitive. Homeowners in these regions are frequently using cash-out refinance strategies to fund down payments on secondary properties.

- Kentucky and Missouri: These states offer some of the most accessible entry points for new investors. Bank statement loans are highly popular here for self employed entrepreneurs looking to purchase rental properties.

- Indiana and Michigan: Buy and hold strategies remain the dominant approach. Investors are focusing on landlord loans to lock in long term yields while property values continue their steady appreciation.

Navigating the Road Ahead

The current market environment requires a proactive approach to financing. Whether you are a first time homebuyer or a seasoned investor, the ability to compare loan programs and understand the impact of PMI (Private Mortgage Insurance) or DTI (Debt to Income) on your approval is critical. Staying informed about daily rate shifts helps you time your lock with confidence rather than uncertainty.

As we look toward the mid-June Federal Reserve meeting, expect continued volatility. The central bank's stance on inflation will dictate the long term trajectory of mortgage rates. By aligning your financing strategy with your specific financial goals today, you can position yourself to take advantage of opportunities as they arise in these dynamic housing markets.

If you have questions about how these rates apply to your specific scenario, reaching out for personal guidance is the best way to gain clarity.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664