May 18th Mortgage Secrets Revealed: What Experts Don't Want You to Know About Today's Rate Shifts

Navigating the mortgage market on May 18th requires more than just checking a daily ticker. Many borrowers and real estate professionals assume that interest rates are set in stone by the Federal Reserve, but the reality is much more fluid. Behind the scenes, a complex dance of bond yields, inflation data, and lender profit margins dictates the actual cost of your home loan.

Understanding these shifts is the difference between securing a manageable monthly payment and overpaying by thousands of dollars over the life of your loan. For homeowners in Alabama, investors in Chicago, and realtors across Florida or Virginia, the "secrets" of the industry are actually accessible mechanics that you can use to your advantage.

The Invisible Engine Driving Your Rate

Lenders do not select interest rates based on a whim. They closely follow the 10-year U.S. Treasury yield and the price of Mortgage-Backed Securities (MBS). When the 10-year Treasury yield rises, mortgage rates almost always follow suit. Conversely, when investors seek safety in bonds, driving yields down, your potential mortgage rate improves.

10-Year Treasury Yield: This is the interest rate the U.S. government pays on its ten-year debt. It serves as the primary benchmark for 30-year fixed-rate mortgages.

Mortgage-Backed Securities (MBS): These are bundles of home loans sold to investors on the secondary market. When demand for MBS is high, prices go up and interest rates stay lower.

You can track these indicators yourself to anticipate which way the wind is blowing. If you see a morning report showing a spike in Treasury yields, you should expect lenders to issue a "reprice for the worse" by mid-afternoon. According to research from Investopedia, the correlation between these yields and home loans is one of the most reliable signals in the financial world.

The Credit Score Tier Myth

Most consumers believe that a "good" credit score is enough to get the best rate. In reality, mortgage pricing works in tiers, and being just one point below a threshold can cost you a quarter percent in interest. A score of 739 might be grouped with a much lower tier, while a 740 unlocks the "excellent" pricing bucket.

Loan-Level Price Adjustment (LLPA): These are risk-based fees assessed by Fannie Mae and Freddie Mac. They are often "baked into" the interest rate you are quoted based on your credit score and down payment.

For a borrower in Michigan or Missouri, moving from a 5% down payment to a 3% down payment might actually improve the rate in some specific conventional loan scenarios due to how private mortgage insurance (PMI) interacts with these tiers. Always ask your strategist to show you the "pricing breaks" for your specific profile.

The Truth About "No-Cost" Mortgages

There is no such thing as a free lunch in real estate finance. A "no-cost" mortgage simply means the lender is providing a credit to cover your closing costs. To afford this, the lender gives you a higher interest rate than the market baseline.

Lender Credit: This is a payment from the lender to the borrower that offsets closing costs in exchange for a higher interest rate. It is a powerful tool for buyers who are short on cash but have high monthly income.

Discount Points: This is the opposite of a credit. You pay a fee upfront to "buy down" the interest rate for the life of the loan.

If you plan to stay in your home in Georgia or California for 20 years, buying points is often a wise investment. However, if you are a "fix and flip" investor or plan to refinance in two years, taking a higher rate with a lender credit to keep cash in your pocket is usually the smarter move.

Strategic Equity Extraction for Investors

Investors in hot markets like Florida and Virginia are increasingly moving away from traditional financing. Instead of focusing on their personal debt-to-income ratio, they are utilizing the equity in their existing portfolios to fuel growth.

Cash-Out Refinance: This involves replacing your current mortgage with a new, larger loan and taking the difference in cash. It is a primary method for landlords to fund renovations or acquire new properties.

Consider an investor in Atlanta who owns a duplex worth $650,000 with a $350,000 balance. By executing a cash-out refinance at 75% Loan-to-Value (LTV), they can pull out roughly $137,000 after costs. This capital can be used to purchase a second property or renovate the existing units to command higher market rents. This strategy is essential for the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method.

The Power of the DSCR Loan

For self-employed borrowers or those with complex tax returns in Illinois or Kentucky, traditional income verification can be a hurdle. This is where the Debt Service Coverage Ratio (DSCR) loan becomes a game-changer.

Debt Service Coverage Ratio (DSCR): A calculation that compares a property's annual net operating income to its annual mortgage debt. If the property generates enough rent to cover the mortgage, the borrower's personal income is not used for qualification.

Non-QM Loan: This is a "Non-Qualified Mortgage" that does not follow the standard federal guidelines. These loans are designed for investors, foreign nationals, and self-employed individuals.

Using a DSCR loan allows you to scale a portfolio quickly because your personal "DTI" (Debt-to-Income) does not limit the number of properties you can finance. As long as the rental income supports the payment, the deal moves forward. You can view current trends on Freddie Mac’s Primary Mortgage Market Survey to see how these non-traditional rates compare to the national average.

Navigating Short-Term Rental Volatility

Airbnb and short-term rental (STR) investors face unique financing challenges. Many banks view STR income as unstable. However, expert strategists know how to use "AirDNA" data or historical rental records to qualify these properties using the same DSCR logic applied to long-term rentals.

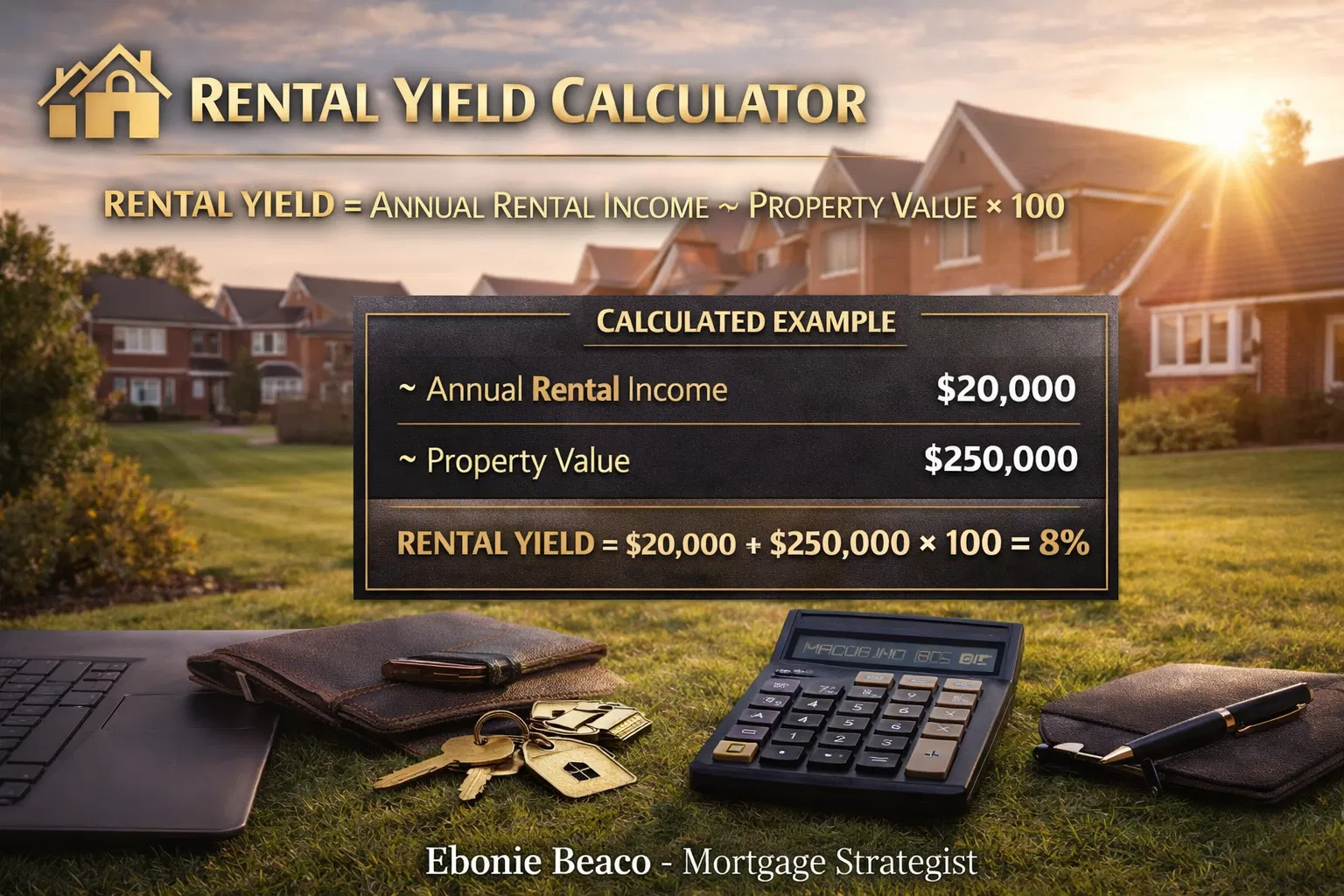

Whether you are looking at vacation homes in the Blue Ridge Mountains of Virginia or coastal properties in Florida, the key is the rental yield.

Rental Yield: The total annual rental income divided by the property value, expressed as a percentage. It helps investors compare the profitability of different locations.

An 8% yield on a $250,000 property indicates a healthy cash flow. If the property's yield is low, it might be better suited for a long-term play or a different financing structure like a Bridge Loan.

The "Float-Down" Strategy

When you apply for a loan, you typically "lock" your rate for 30 to 60 days. If rates drop significantly while you are under contract, you might feel like you missed out. This is why you must ask about a "float-down" clause.

Rate Lock: A guarantee from the lender that your interest rate and points will not change for a specific period.

Float-Down Option: A feature that allows a borrower to lower their locked interest rate if market rates drop significantly before the loan closes.

Not every lender offers this, and those that do often have strict requirements (e.g., the market must drop by at least 0.25%). For a buyer in the competitive California or Chicago markets, having a float-down option provides peace of mind during the stressful escrow period.

Financing Solutions for Diverse Needs

The mortgage landscape today is broader than just 30-year fixed loans. There are specialized programs designed for every scenario:

- ITIN Mortgage Loans: For individuals who have an Individual Taxpayer Identification Number but do not have a Social Security Number.

- Bank Statement Loans: Perfect for entrepreneurs in Indiana or Arkansas who have high revenue but high tax deductions.

- Bridge Loans: Short-term financing used to "bridge" the gap between buying a new home and selling an old one.

- Hard Money Loans: Asset-based financing used primarily by fix-and-flip investors who need speed over low interest rates.

The best way to navigate these options is to treat your mortgage as a strategic financial tool rather than a simple debt. Whether you are a first-time homebuyer or a seasoned commercial investor, the structure of your financing has a massive impact on your long-term wealth.

Take Control of Your Financial Future

The "secrets" of May 18th aren't about hidden tricks; they are about understanding the technical mechanics of the market. From tracking the 10-year Treasury to optimizing your credit score for a specific pricing tier, you have more control over your mortgage rate than you might think.

Explore your options, jump in with a clear plan, and compare strategies that align with your long-term goals. Accessing the right information today ensures you aren't left behind by tomorrow's market shifts.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664