Mastering ARV: The One Number That Makes or Breaks Your Wholesale Real Estate Deal

Meta Title: Mastering ARV in Wholesale Real Estate | Home Loans Network Meta Description: Learn how to calculate After-Repair Value (ARV) like a pro to ensure your wholesale real estate deals stay profitable and attractive to cash buyers in 2026.

Wholesale real estate moves at a lightning pace, but one incorrect variable can bring your entire operation to a screeching halt. Whether you are hunting for off-market opportunities in Chicago or scaling an investment portfolio across the sunbelt in Florida, you have likely heard the term ARV mentioned in every conversation. ARV stands for After-Repair Value, which is the estimated market value of a property once all necessary renovations and upgrades are completed. Think of this number as the North Star for your entire deal structure because every other calculation flows directly from it. Without a precise and realistic ARV, you cannot calculate your maximum allowable offer or your potential assignment fee with any degree of certainty. Mastering this metric allows you to present deals to your buyers with total confidence and professional transparency.

Visual: A row of clean, realistic suburban homes in a well-maintained neighborhood. Footer: Ebonie Beaco - Mortgage Strategist. Overlay: Comp A $250k | Comp B $260k | ARV Average $250k.

Visual: A row of clean, realistic suburban homes in a well-maintained neighborhood. Footer: Ebonie Beaco - Mortgage Strategist. Overlay: Comp A $250k | Comp B $260k | ARV Average $250k.

ARV functions as the primary anchor that determines whether a professional house flipper or a long-term landlord will actually purchase your contract. Real estate investing is built upon predictable outcomes, and the ARV tells your end buyer exactly what their exit price looks like before they even pick up a hammer. To arrive at this figure, you must analyze comparable sales, commonly referred to as "comps," which are similar properties that have sold recently in the immediate vicinity. You generally want to find properties that have sold within the last 90 days and are located within a one mile radius of your subject property. Ensuring these comps match in square footage, bedroom and bathroom count, and architectural style is the only way to generate a figure that holds up under scrutiny. When you provide a deal with a rock-solid ARV, you are essentially pre-qualifying the opportunity for your buyer's capital.

Let’s jump in and look at a practical breakdown of how you might calculate this in a real world real estate investing scenario. Imagine you find a distressed property in a solid neighborhood and identify three highly relevant comps that were recently renovated and sold by other investors. Comp A sold for $250,000, Comp B sold for $260,000, and Comp C sold for $240,000, all within the last few months. By adding these three sale prices together and dividing the total by three, you find an average ARV of $250,000 for that specific pocket of the market. This $250,000 becomes the essential baseline for every subsequent decision you make on that wholesale deal. If your comps are scattered or inconsistent, your ARV becomes a guess rather than a data point, which is where most beginners lose their credibility.

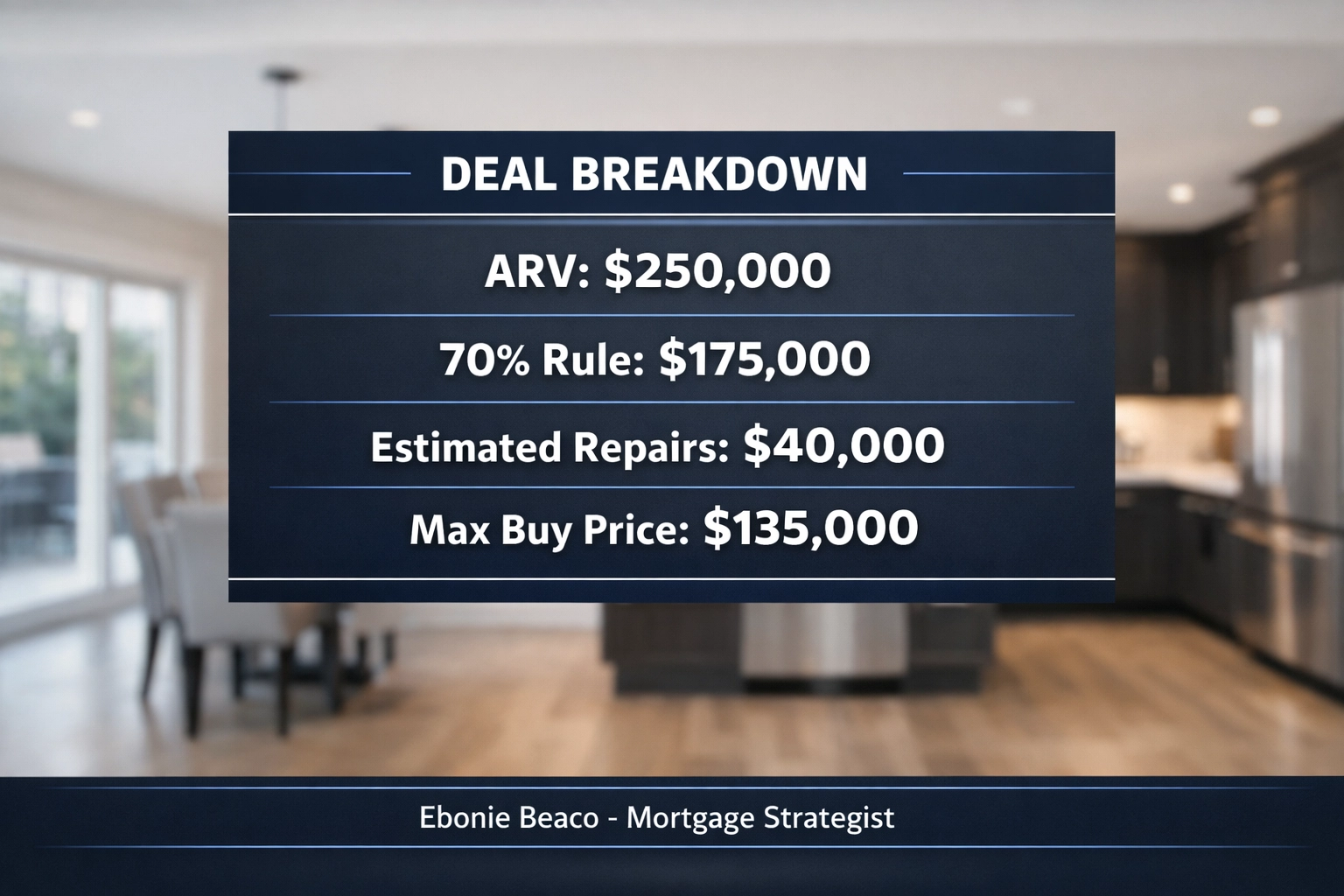

Once you have established that $250,000 ARV, you can finally work backward to determine if the deal is actually worth your time and effort. Most experienced investors in markets like Virginia, Georgia, or Michigan follow a version of the 70% rule to ensure they have a safety margin. This rule suggests an investor should pay no more than 70% of the ARV minus the estimated cost of all repairs. In our current example, 70% of the $250,000 ARV equals $175,000 as a starting point for the offer. If the house requires roughly $40,000 in renovation work, your maximum purchase price for your end buyer would be approximately $135,000. To secure a $15,000 assignment fee for yourself, you would need to get the property under contract with the original seller for $120,000 or less.

Visual: A professional deal analysis chart showing: ARV: $250,000 | 70% Rule: $175,000 | Estimated Repairs: $40,000 | Max Buy Price: $135,000. Footer: Ebonie Beaco - Mortgage Strategist.

Visual: A professional deal analysis chart showing: ARV: $250,000 | 70% Rule: $175,000 | Estimated Repairs: $40,000 | Max Buy Price: $135,000. Footer: Ebonie Beaco - Mortgage Strategist.

Understanding local housing market activity is essential because a proper ARV is never a static or permanent figure. A property in a rapidly gentrifying area of Atlanta might justify a slightly higher ARV than the raw data suggests if demand is skyrocketing and inventory is low. Conversely, in a cooling market where homes are sitting longer, you might want to be more conservative with your estimates to protect your cash buyers. Successful wholesalers always account for current interest rates and buyer appetite when they are finalizing their projected exit prices. This level of transparency in your numbers builds massive trust with your buyers list over time and leads to repeat business. You can find more information about current market trends by visiting our mortgage basics page to see how financing shifts affect local property values.

While you might be focused on the immediate assignment fee, your buyer is likely looking toward the future of the property and its financing needs. If your ARV is inflated or unrealistic, their fix and flip financing or DSCR investor loan appraisal will eventually come back low. This often causes the deal to fall apart at the closing table, which damages your reputation and wastes everyone’s time. Positioning yourself as a wholesaler who understands the loan process and how lenders evaluate collateral makes you an invaluable partner in the transaction. When you present a deal that is "bankable" because the ARV is accurate, you make it much easier for your buyer to secure funding. This professional approach separates the hobbyists from the high-volume wholesalers who close deals every single month.

Scaling your wholesale business requires moving beyond simple guesswork and into the realm of professional data analysis. You should strive to understand the various financing strategies your buyers use, such as bridge loans or hard money, so you can anticipate their potential objections. Knowing that a lender might only lend 75% of the ARV on a specific program helps you price your deals so they fit within those constraints. If you can defend your ARV with solid data, you can successfully negotiate with both the motivated seller and the savvy investor. This expertise allows you to handle increasingly complex transactions, including small multifamily properties or commercial assets, with total confidence. You can always check our FAQ for more insights on how different loan types interact with property valuations.

Mastering the ARV is effectively mastering the heart of the real estate transaction for any investor. It serves as the bridge between a distressed, neglected house and a beautiful, profitable investment property that adds value to the community. If you find yourself struggling to nail down these numbers or if your buyers are having trouble getting their deals funded, it may be time to reassess your strategy. Working with a dedicated mortgage strategist who understands the investor mindset can help you better structure your deals for long-term success. Reach out today to discuss how we can help you evaluate your next wholesale opportunity and connect your buyers with the right capital. Let us work together to ensure your next wholesale deal is a profitable win for everyone involved in the process.

📞 Work With Ebonie Beaco

If you are a wholesaler looking to:

- Close more deals

- Connect your buyers with financing

- Structure deals that actually get approved

- Learn how to grow into a real estate investor

I can help you every step of the way.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954

Phone: 312-392-0664 Website: HomeLoansNetwork.com/contact-us

👉 Whether you need lending, deal structuring, or mentorship, reach out today.