Looking for the Daily Mortgage Briefing? Here Are 5 Things You Should Know Before Tomorrow’s Market Opens

Navigating the mortgage market requires a proactive approach, especially as economic indicators shift daily and influence your borrowing power. On this Saturday, May 30, 2026, the housing landscape remains in a state of watchful waiting as the market digests the latest inflation data released just yesterday. For homeowners in Virginia, real estate investors in Florida, and first-time buyers in Illinois, understanding these shifts is essential for making informed financial decisions. Tomorrow’s market opening is expected to reflect a week of volatility driven by Treasury yield fluctuations and geopolitical developments.

The current atmosphere suggests that "higher-for-longer" is more than just a phrase; it is the prevailing strategy of the Federal Reserve as they navigate stubborn price pressures. While national averages for a 30-year fixed mortgage are currently hovering between 6.56% and 6.65%, the path forward is heavily dependent on upcoming economic reports and global stability. Whether you are managing a portfolio of short-term rentals in Alabama or looking to tap into your home equity in California, staying ahead of the opening bell gives you a strategic advantage.

1. The PCE Inflation Impact and Fed Sentiment

The Personal Consumption Expenditures (PCE) price index, which is the Federal Reserve's preferred measure of inflation, was released on May 29, 2026, and the results have sent ripples through the mortgage bond market. This data directly influences the Federal Open Market Committee (FOMC) as they prepare for their next meeting on June 17–18. If inflation remains sticky, as recent reports suggest, the likelihood of a rate cut in the near term diminishes significantly. Mortgage lenders typically price their loans based on these expectations, often moving rates ahead of actual Fed policy changes to mitigate risk.

For borrowers, this means that the "wait-and-see" approach might carry a higher cost if rates continue to drift upward through the summer months. The current federal funds target rate of 3.50% to 3.75% is designed to cool the economy, but until the PCE index shows a consistent return toward the 2% target, mortgage rates are unlikely to drop into the 5% range. Investors and homeowners should prepare for a choppy environment where day-to-day moves are influenced more by economic "surprises" than by seasonal trends.

Ebonie Beaco - Mortgage Strategist

2. Geopolitical Shifts and the 10-Year Treasury Yield

Mortgage rates are not set by the government; they are closely tied to the performance of the 10-year Treasury yield. Recently, yields have pushed toward the 4.57% mark, largely driven by international uncertainty, including the ongoing conflict in Iran. When global tensions rise, investors often seek the safety of bonds, but inflationary pressures linked to rising oil prices can counteract this, pushing yields and mortgage rates higher. This delicate balance is a primary reason why rates have seen a week-over-week increase of nearly 18 basis points.

Understanding this relationship is vital for anyone planning a purchase or a cash-out refinance in states like Georgia or Michigan. When the 10-year yield climbs, the cost of funding for lenders increases, which is then passed on to the consumer in the form of higher interest rates. If you are watching the market tomorrow morning, keep a close eye on the 10-year Treasury note; a breach above 4.6% could signal a more aggressive upward move for conventional and FHA loans alike.

3. Regional Spotlight: Growth and Pricing in AL, FL, and CA

While national averages provide a benchmark, real estate is fundamentally local, and market activity varies significantly across our served states. In Florida and Alabama, we are seeing a steady demand for DSCR investor loans as landlords seek to capitalize on the robust rental market. Conversely, in high-cost areas like California, many homeowners are turning toward HELOC (Home Equity Line of Credit) options to access liquidity without disturbing their low-interest primary mortgages. This regional divergence highlights the need for a personalized financing strategy that accounts for local appreciation and inventory levels.

In metropolitan hubs like Chicago, Illinois, the commercial real estate sector is adapting to the current rate environment by utilizing more creative financing. Investors are increasingly looking at multi-unit properties and mixed-use buildings as a hedge against inflation. For realtors in Indiana and Kentucky, the focus remains on educating buyers about the benefits of "buying the house and dating the rate," with the intention of a future rate-term refinance once the market eventually stabilizes.

4. Investor Strategy: The Resilience of DSCR and Landlord Loans

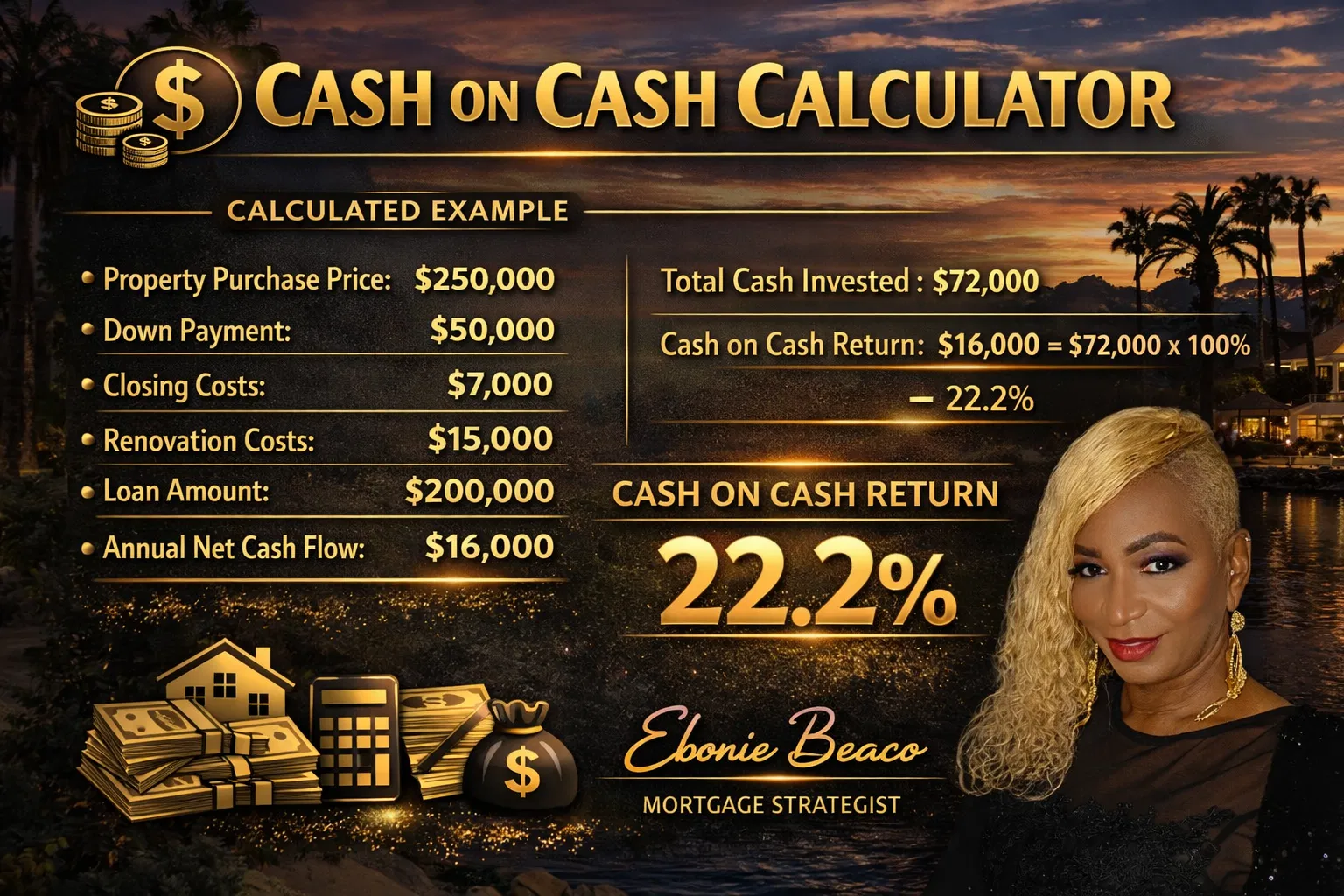

Real estate investors are currently prioritizing cash flow and debt coverage over speculative appreciation. The DSCR (Debt Service Coverage Ratio) loan has become a cornerstone of this strategy because it qualifies the borrower based on the income potential of the property rather than personal W-2 income. This is particularly beneficial for self-employed entrepreneurs and portfolio landlords who may have complex tax returns but own high-performing rental assets. Even in a 6.5% rate environment, a property with a strong DSCR remains a viable investment.

Consider an investor looking to purchase a four-unit building in a growing market like Atlanta, Georgia. If the property generates enough rental income to cover the mortgage, taxes, insurance, and HOA fees with a margin (typically 1.20x or higher), the loan is considered lower risk for the lender. This allows investors to continue scaling their portfolios without being sidelined by the same debt-to-income (DTI) constraints that affect traditional residential borrowers.

Definition: DSCR (Debt Service Coverage Ratio)

Definition: A financial metric used by lenders to measure a property's ability to cover its debt obligations with its own income.

Application: Investors use this to qualify for loans based on rental revenue rather than personal income, facilitating easier scaling of rental portfolios.

Ebonie Beaco - Mortgage Strategist

5. Homeowner Strategy: HELOC vs. Cash-Out Refinance

Many homeowners currently find themselves "locked in" to low interest rates from 2020 or 2021, making a traditional cash-out refinance less attractive. However, the need for capital for home renovations, debt consolidation, or new investment opportunities remains high. This is where the HELOC becomes a powerful tool. Unlike a refinance, which replaces your entire mortgage with a new one at current rates, a HELOC sits as a second lien, allowing you to keep your 3% or 4% primary rate while accessing your equity at a variable market rate.

For a homeowner in Virginia or Missouri with significant equity, a HELOC offers flexibility. You only pay interest on the amount you draw, which is ideal for ongoing projects like a kitchen remodel or as a "just in case" credit line. On the other hand, if you need a large lump sum and your current primary rate is already near 6%, a cash-out refinance might be more efficient to consolidate all debts into a single, predictable monthly payment.

Definition: HELOC (Home Equity Line of Credit)

Definition: A revolving credit line secured by the equity in your home that allows you to borrow, repay, and borrow again during a set draw period.

Application: This is an excellent choice for homeowners who want to maintain their low primary mortgage rate while still accessing funds for improvements or other investments.

Analyzing a Real-World Financing Scenario

To illustrate how these strategies play out, let's look at a homeowner in the Chicago suburbs who wants to access $100,000 in equity to fund a fix-and-flip project.

Scenario: Equity Access Comparison

- Home Value: $600,000

- Current Mortgage Balance: $300,000 (at 3.25%)

- Target Cash: $100,000

Option A: Cash-Out Refinance

- New Loan Amount: $400,000

- New Rate: 6.65%

- Result: The entire $400,000 balance now carries the higher 6.65% interest rate, significantly increasing the monthly payment.

Option B: HELOC

- Primary Mortgage: $300,000 (stays at 3.25%)

- HELOC Amount: $100,000 (at current market rate, e.g., 8.5%)

- Result: The homeowner only pays the higher rate on the $100,000 they actually use, saving thousands in interest compared to refinancing the entire balance.

Ebonie Beaco - Mortgage Strategist

Strategic Opportunities for Real Estate Professionals

Realtors and wholesalers in Arkansas and Indiana can use this market data to help their clients overcome the "rate shock" hurdle. By presenting options like seller buy-downs or non-QM mortgage loans, you can structure deals that are affordable even when the national average ticks upward. For example, a 2/1 buy-down allows a buyer to start with a rate 2% lower than the market for the first year, providing immediate relief and a bridge to potential future refinancing.

Investors should also explore bridge loans and fix-and-flip financing if they are looking to acquire distressed properties that do not qualify for traditional financing. These short-term solutions are designed to get the property to a "stabilized" state, at which point it can be refinanced into a long-term landlord loan. This strategy is particularly effective in competitive markets like Florida or California, where speed of execution is often as important as the interest rate itself.

The Role of Non-QM and Bank Statement Loans

For the self-employed borrowers in our network, traditional tax returns don't always tell the full story of financial health. Bank statement loans allow us to look at 12 to 24 months of deposits to determine income, providing a path to homeownership for entrepreneurs who maximize their business deductions. Similarly, ITIN mortgage loans provide opportunities for borrowers without a Social Security number to enter the housing market, expanding the pool of potential buyers and strengthening the local economy.

As the market opens tomorrow, these specialized programs will continue to provide liquidity where traditional big-box lenders often fall short. We are committed to offering a wide range of solutions, from ground-up development loans to mixed-use commercial properties. Education and transparency are the foundations of our guidance, ensuring that every borrower understands their options in this complex environment.

Definition: Non-QM (Non-Qualified Mortgage)

Definition: A category of loans that does not follow the standard consumer protection guidelines set by the federal government, often used for borrowers with unique income situations.

Application: These loans allow self-employed individuals and investors to qualify using alternative documentation, such as bank statements or asset depletion.

Ebonie Beaco - Mortgage Strategist

Conclusion: Preparing for the Week Ahead

Tomorrow's market opening will likely see mortgage rates remain in the mid-to-high 6% range as the dust settles from Friday’s PCE report. While the headlines may focus on the challenges of the current environment, there are always strategic opportunities for those who are prepared. Whether you are looking to purchase your first home, refinance a rental property, or build a new commercial project, having a clear plan is the first step toward success.

If you have questions about how these national trends affect your specific situation in AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, or VA, we are here to help you navigate the process with confidence. Explore your options and access the tools you need to turn today’s market into tomorrow’s equity.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664