Looking For a Way to Pay for Your Remodel? Here Are 10 Things You Should Know About HELOCs

You finally found that perfect mid-century modern home in Indianapolis or a classic colonial in Virginia. Maybe you have lived in your Florida bungalow for years and the kitchen is screaming for an update. You know the renovation will increase your property value, but finding the cash to start can feel like a hurdle.

If you are looking for a flexible way to fund your vision, a Home Equity Line of Credit (HELOC) is often the smartest tool in the shed. Whether you are a homeowner in Chicago or a real estate investor in Alabama, understanding how to leverage your equity is a game changer.

Explore these ten critical insights before you sign on the dotted line.

1. Your Equity Is the Engine

A HELOC allows you to borrow against the equity you have built in your home. Equity is the difference between the current market value of your property and the remaining balance on your mortgage.

Equity: The financial interest or value a homeowner has in their property.

Practical Application: If your home is worth $400,000 and you owe $250,000, you have $150,000 in equity to potentially tap into.

Using your home as collateral allows a Kentucky HELOC lender to offer you better terms than an unsecured credit card. This is because the loan is backed by a physical asset.

2. It Works Like a Credit Card, Not a Personal Loan

Unlike a traditional loan where you get a giant check on day one, a HELOC is a revolving line of credit. You are granted a maximum limit, and you only borrow what you need when you need it.

Line of Credit: A flexible loan from a bank or financial institution that consists of a defined amount of money that you can access as needed.

Practical Application: You can draw $10,000 for new flooring this month and another $20,000 for cabinets next month without reapplying.

This flexibility is why many homeowners in Michigan and Missouri prefer HELOCs for multi-stage renovations. You are not forced to pay interest on money sitting in your bank account that you haven't used yet.

3. Interest Rates Are Generally More Affordable

Because a HELOC is a secured loan, the interest rates are typically much lower than personal loans or high-interest credit cards. This makes it a preferred choice for large-scale projects like a primary suite addition or a full basement finish in Georgia.

Secured Loan: A loan backed by collateral, such as a home or car, to reduce the risk for the lender.

Practical Application: Using a HELOC instead of a credit card for a $50,000 remodel can save you thousands of dollars in interest charges over the life of the loan.

You can compare current trends and see how these rates fit your budget by using mortgage calculators.

4. Potential Tax Benefits for Home Improvements

One of the best kept secrets of the HELOC is the potential for tax deductibility. If you use the funds to buy, build, or substantially improve the home that secures the loan, the interest might be deductible.

Substantial Improvement: A renovation that adds value to the home, prolongs its useful life, or adapts it to new uses.

Practical Application: Replacing a roof or upgrading the HVAC system in an Arkansas rental property could qualify as a substantial improvement.

Always consult with a tax professional to see how this applies to your specific situation in California or Virginia.

5. Perfect for Projects with Moving Parts

Renovations rarely go exactly according to plan. Costs fluctuate, materials get delayed, and contractors might find issues behind the walls. HELOCs are ideal for these scenarios because they accommodate ongoing costs.

Jump in and start your project knowing you have a safety net. If the kitchen remodel in your Chicago condo ends up costing $5,000 more due to plumbing issues, you simply draw more from your line. You can learn more about how this fits into the loan process to stay prepared.

6. The Draw Period vs. The Repayment Period

Every HELOC has two distinct phases. During the draw period, which often lasts 10 years, you can take money out and usually only have to pay the interest. Once that period ends, you enter the repayment period.

Draw Period: The initial phase of a HELOC during which the borrower can access funds from the line of credit.

Repayment Period: The phase following the draw period where the borrower can no longer access funds and must pay back both principal and interest.

Practical Application: A homeowner in Florida might enjoy low interest-only payments during the 10-year draw period while they finish their renovations and then transition to full payments later.

7. Accessing Your Cash Is Simple

Managing payments to contractors or buying supplies at the hardware store in Alabama is easy with a HELOC. Most lenders provide you with a specialized debit card or a book of checks linked directly to your line of credit.

Access your funds instantly without having to wait for wire transfers or manual approvals. This makes you a more agile "cash buyer" in the eyes of local contractors.

8. You Need a Solid Financial Profile

To qualify, lenders look for specific benchmarks. You generally need at least 10% to 20% equity remaining in your home after the HELOC is added. A Indiana HELOC lender will also evaluate your credit score and your Debt-to-Income (DTI) ratio.

Debt-to-Income (DTI) Ratio: A personal finance measure that compares an individual's monthly debt payment to their monthly gross income.

Practical Application: If your monthly debts are $2,000 and your gross income is $6,000, your DTI is 33%, which is generally considered strong for qualification.

9. Strategic Equity Extraction Example

Let's look at how the math works for a typical homeowner or investor. Imagine you own a property in California valued at $600,000.

- Current Mortgage Balance: $350,000

- Max Combined Loan-to-Value (CLTV): 85%

- Total Allowable Debt: $510,000 ($600,000 x 0.85)

- Available HELOC Limit: $160,000 ($510,000 - $350,000)

With a $160,000 line of credit, you could fully gut a kitchen, add a bathroom, and still have a cushion for unexpected repairs. This strategy is common for BRRRR investors (Buy, Rehab, Rent, Refinance, Repeat) who use a HELOC on one property to fund the down payment on a DSCR rental property loan for another.

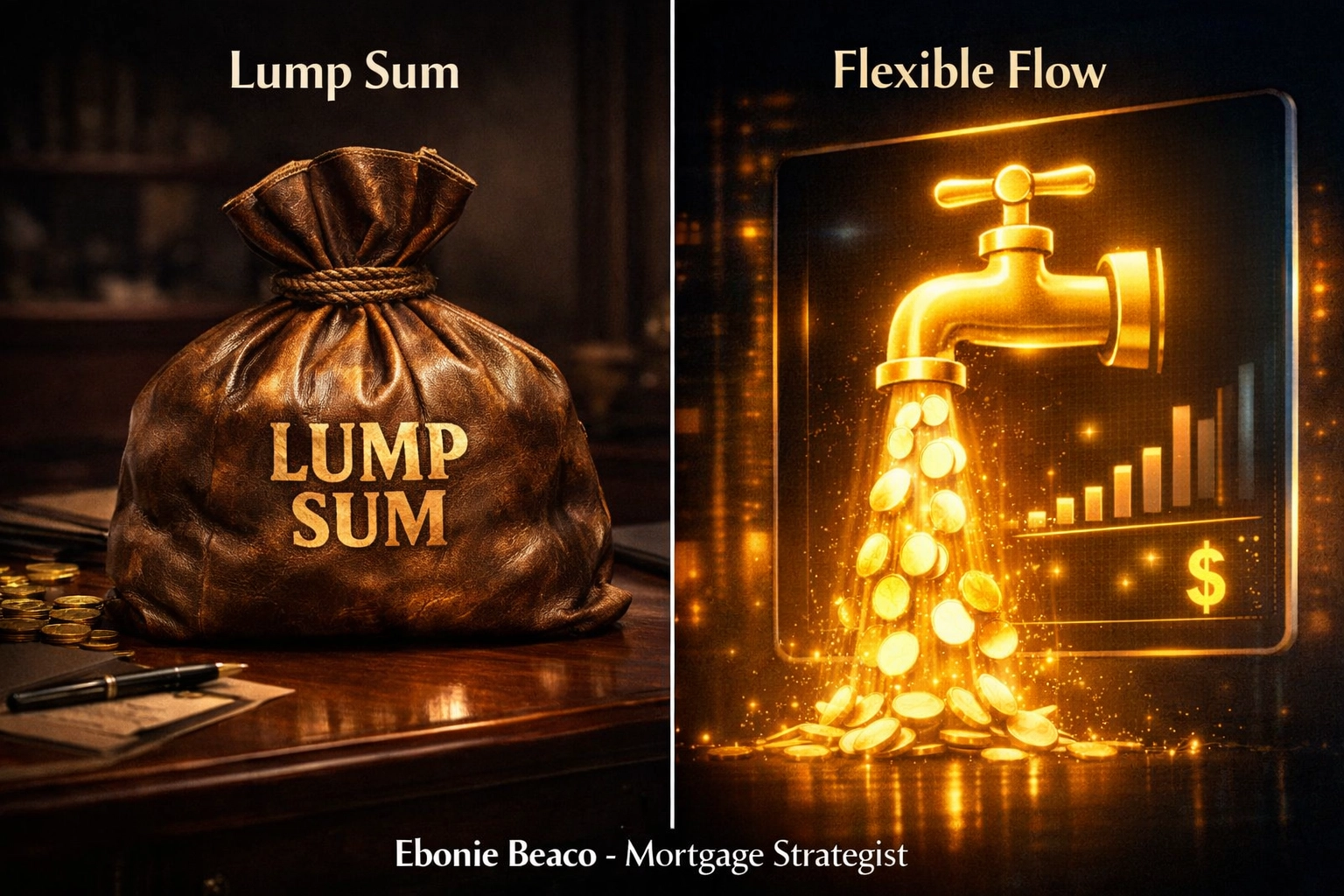

10. Comparing HELOCs and Home Equity Loans

While both involve your equity, they are different animals. A HELOC offers a variable rate and flexible borrowing. A Home Equity Loan provides a fixed lump sum with a fixed interest rate.

Variable Rate: An interest rate on a loan that fluctuates over time because it is based on an underlying benchmark interest rate.

Practical Application: If the prime rate goes up, your HELOC payment might increase, whereas a fixed-rate loan stays the same.

Compare these options carefully. If you have a one-time, fixed-cost project, a fixed-rate mortgage or home equity loan might be better. If you want a flexible rainy-day fund for ongoing upgrades in Kentucky or Virginia, the HELOC wins.

Leveraging Equity for Real Estate Growth

For real estate investors, a HELOC is more than just a renovation fund; it is a liquidity tool. Investors in markets like Chicago or major cities in Florida often use HELOCs to fund the "rehab" portion of a fix-and-flip project. This keeps their liquid cash available for other acquisitions or earnest money deposits.

If you are a landlord managing multiple units, having a HELOC attached to your primary residence or an investment property can cover emergency repairs like a burst pipe or a failed HVAC system without disrupting your cash flow. It functions as a high-limit emergency fund that costs you nothing until you actually use it.

Whether you are looking to create your dream kitchen or scale your investment portfolio, understanding the mechanics of equity is the first step. Home Loans Network provides a variety of loan programs tailored to your specific goals, from conventional financing to specialized investor products.

Stop guessing and start building.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664