Looking for a Virginia HELOC Lender? Here Are 10 Things You Must Know Before You Sign Anything

If you are a homeowner in Virginia, Michigan, or Florida, you are sitting on a goldmine of equity. The real estate market across states like Alabama, Arkansas, California, Georgia, Illinois, Indiana, Kentucky, and Missouri has seen significant appreciation over the last few years. Whether you want to fund a renovation, consolidate high-interest debt, or build a real estate investment portfolio, a Home Equity Line of Credit (HELOC) is one of the most flexible tools in your financial toolkit.

However, searching for a Virginia HELOC lender or a Michigan HELOC lender can feel overwhelming if you don't know the rules of the game. Before you tap into your home’s value, you need to understand how these lines of credit actually function.

1. The Variable Rate Trap

HELOCs are unique because they are typically variable-rate products. This means your interest rate is tied to an index, usually the Wall Street Journal Prime Rate.

Variable Interest Rate: A loan interest rate that fluctuates over time based on an underlying benchmark or index.

- Application: This means your monthly payment can increase if the Federal Reserve raises interest rates, so you should always budget for potential fluctuations.

Most lenders will quote you a "Prime plus margin" rate. If the Prime Rate is 7.5% and your margin is 1.0%, your effective rate is 8.5%. You should ask every Michigan HELOC lender you interview what their specific margin is and if they offer a "Fixed-Rate Lock" option for specific draws.

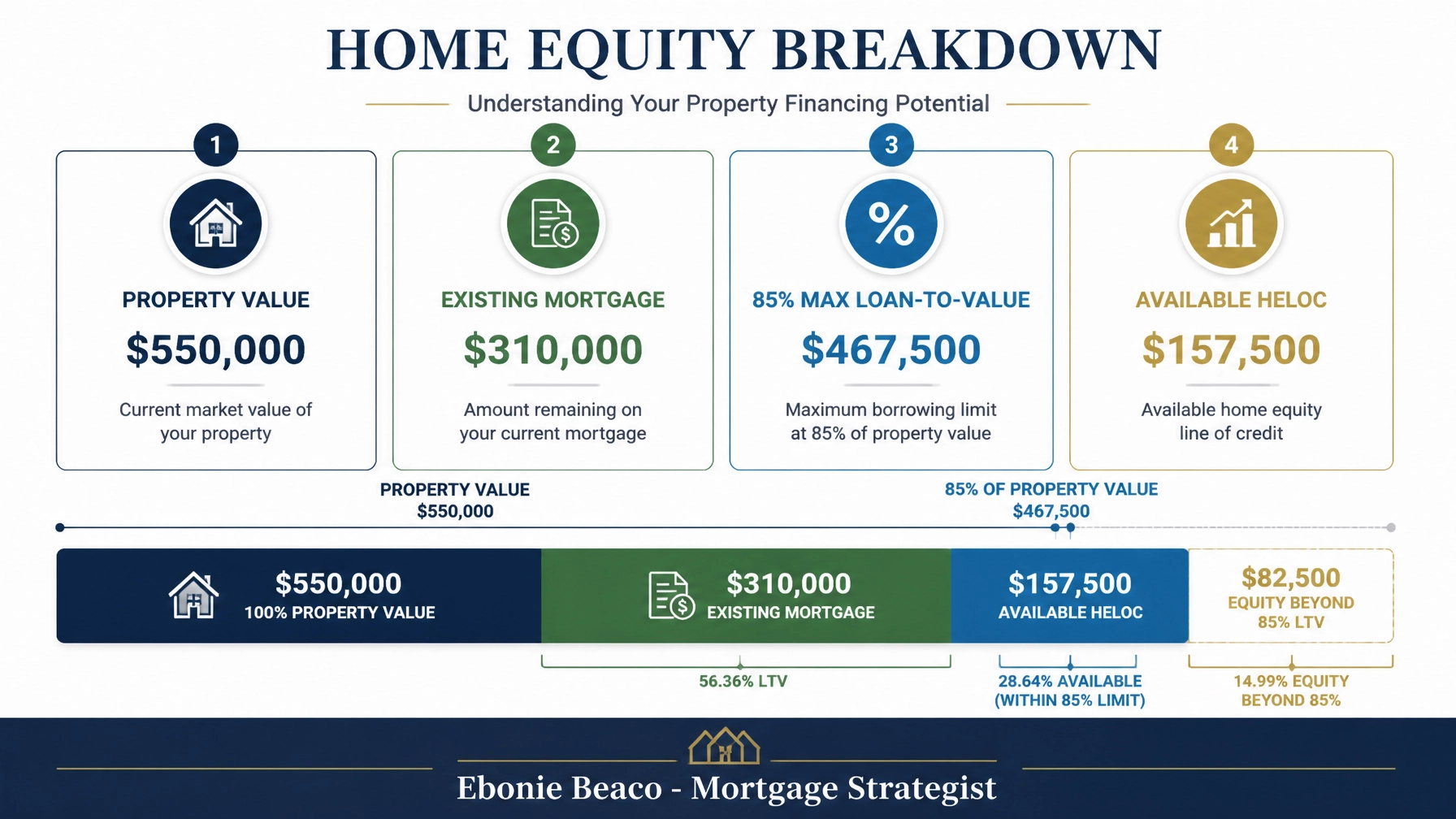

2. The 85% Ceiling You Can’t Ignore

When you apply for a HELOC, lenders look at your Combined Loan-to-Value (CLTV) ratio. This is the total of all your mortgage debt divided by your home's current appraised value.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property to its total appraised value.

- Application: Most lenders in Virginia and Michigan cap this at 80% to 85%, meaning you must leave some equity "cushion" in the home.

Example Calculation:

Imagine you own a home in a suburb of Chicago or a growing neighborhood in Virginia worth $550,000. You currently owe $310,000 on your primary mortgage. If your lender allows up to an 85% CLTV, the math looks like this:

- Total Max Debt: $550,000 x 0.85 = $467,500

- Available HELOC: $467,500 - $310,000 = $157,500

In this scenario, you could access a line of credit for $157,500 to use however you see fit. You can explore how this fits your profile by checking our Mortgage Calculators.

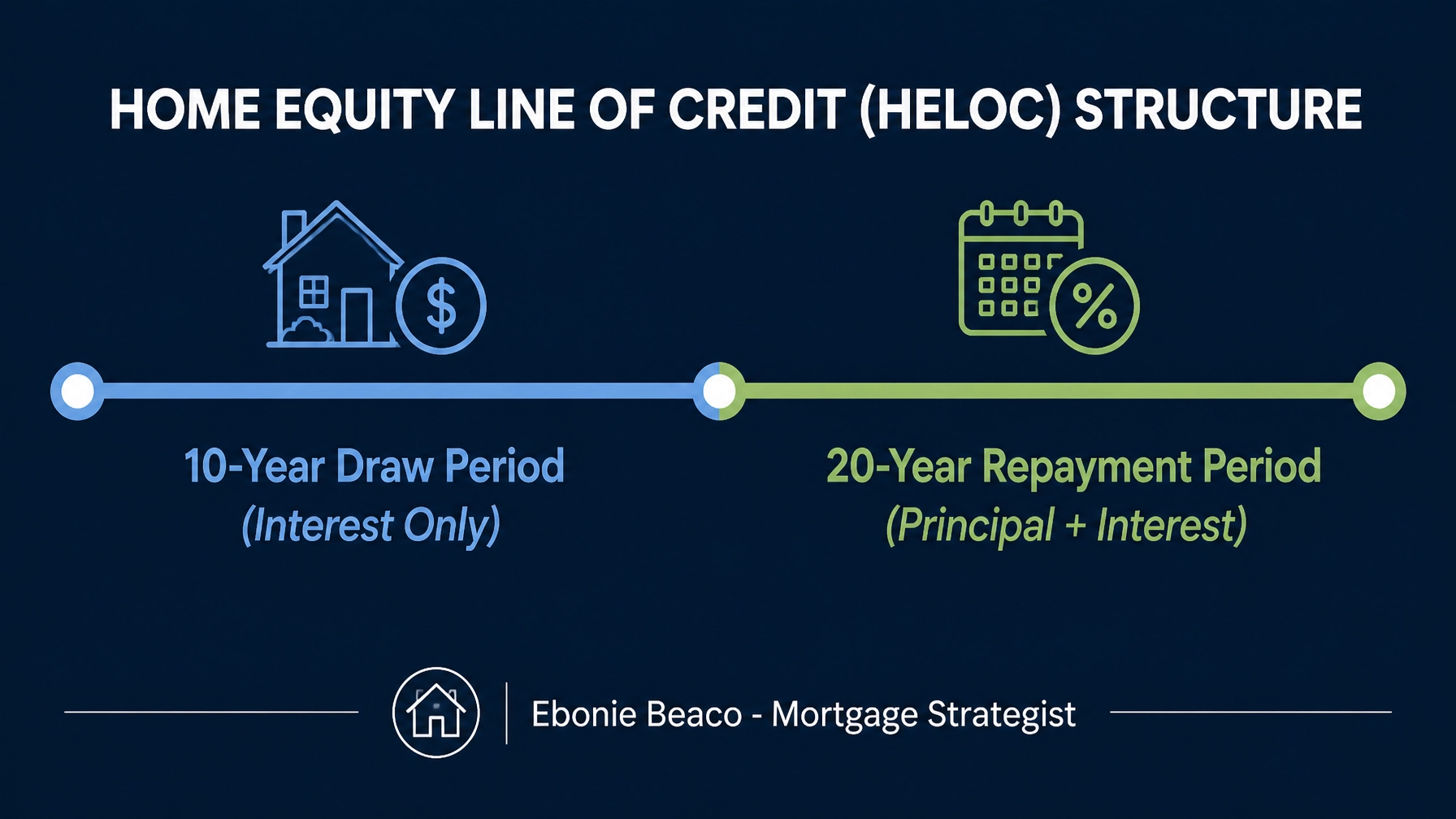

3. The Drawing Period Cliffhanger

A HELOC is not a lump-sum loan; it is a revolving line of credit. It is divided into two distinct phases: the Draw Period and the Repayment Period.

Draw Period: The timeframe (usually 10 years) during which you can borrow money from your credit line and typically make interest-only payments.

- Application: Use this time to fund projects or investments, but remember that you aren't paying down the principal balance yet.

Repayment Period: The phase (often 20 years) following the draw period where you can no longer borrow money and must pay back both principal and interest.

- Application: Your monthly payment will likely jump significantly once this phase begins, so planning your exit strategy is essential.

4. Credit Score Tiers and "As Low As" Rates

You might see advertisements for incredibly low rates from a Virginia HELOC lender, but those are usually reserved for "Tier 1" borrowers.

Credit Tiering: The practice of offering different interest rates based on the borrower’s credit score.

- Application: To get the best margins, you typically need a credit score of 740 or higher, though options exist for scores as low as 640.

If your credit isn't perfect, don't worry. Many Non-QM Mortgage Loans and specialized programs allow for flexibility. You can even request a Soft Pull Credit Request to see where you stand without hurting your score.

5. Closing Costs: The Hidden Surprise

Many homeowners assume HELOCs are free to set up. While some credit unions in Virginia or Michigan might waive certain fees, there are often costs involved.

Closing Costs: Fees paid at the conclusion of a real estate transaction, including appraisal, title search, and government recording fees.

- Application: You should expect to pay between $500 and $2,500 to open a line, depending on whether a full appraisal is required.

6. The 43% DTI Ceiling

Lenders want to ensure you can actually afford the payments. They look at your Debt-to-Income (DTI) ratio, including your new HELOC payment (calculated at the fully indexed rate).

DTI (Debt-to-Income): The percentage of your gross monthly income that goes toward paying debts.

- Application: Keeping your total debt obligations under 43% of your income is the standard goal for most traditional lenders.

7. Tax Deductibility Nuances

Is the interest on your HELOC tax-deductible? In 2026, the rules are specific. Generally, interest is only deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan.

Tax Deductibility: The ability to subtract certain expenses from your taxable income to reduce your tax bill.

- Application: If you use a HELOC to pay off credit cards or buy a car, that interest is generally not tax-deductible; always consult a CPA.

8. The Power for Real Estate Investors

For real estate investors in Florida, Georgia, or California, a HELOC on a primary residence is the ultimate "BRRRR" tool. You can use the equity to purchase a distressed property, fix it up, and then refinance it into a DSCR Investor Loan.

DSCR Loan: A loan based on the property’s rental income rather than the borrower’s personal income.

- Application: This allows you to scale your portfolio quickly without being limited by your personal W-2 income.

9. Appraisal Surprises in Michigan and Virginia

A Michigan HELOC lender may use an Automated Valuation Model (AVM) or a "drive-by" appraisal to determine your home's value. If you have done significant interior renovations, a standard AVM might undervalue your home.

AVM (Automated Valuation Model): A service that uses mathematical modeling and databases to provide an estimate of property value.

- Application: If you believe your home is worth more than the computer says, you may need to pay for a full interior appraisal to unlock more equity.

10. The Strategy of the Safety Net

You don't have to spend the money just because it is available. Many savvy homeowners in Virginia and Michigan set up a HELOC as an emergency fund. You only pay interest on what you actually borrow.

Revolving Credit: A credit line that can be used repeatedly up to a certain limit as long as the account remains open and payments are made.

- Application: This provides a financial safety net for unexpected repairs or investment opportunities that require quick cash.

Access Your Equity with Confidence

Navigating the world of home equity doesn't have to be a solo mission. Whether you are looking for a Virginia HELOC lender or exploring Landlord Loans in Alabama, having a mortgage strategist on your side helps you compare options and avoid costly mistakes.

Jump in and explore how your home equity can work for you. Compare programs, access expert guidance, and align your financing with your long-term wealth goals.

Ready to see how much equity you can unlock?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664