Looking For a Georgia HELOC Lender? Here Are 10 Things You Should Know About Atlanta Equity

If you own a home in the Atlanta metro area, you have likely noticed the explosive growth in property values over the last few years. Whether you are in a historic bungalow in Virginia-Highland or a modern build in Alpharetta, that increase in value represents more than just a number on a real estate website: it is usable wealth.

Tapping into your "Atlanta equity" through a Home Equity Line of Credit (HELOC) has become one of the most popular ways for Georgia homeowners to fund renovations, consolidate high-interest debt, or even seed their next investment property. However, the lending landscape in Georgia can be specific. Finding a Georgia HELOC lender requires understanding local requirements and how your home’s value translates into borrowing power.

Here are 10 essential things you should know about leveraging equity in the current Georgia market.

1. Understanding the LTV and CLTV Ceiling

Loan-to-Value (LTV): The ratio of your current mortgage balance to the appraised value of your home.

Combined Loan-to-Value (CLTV): The total of all loans on your property (first mortgage plus the HELOC) divided by the home's value.

In Georgia, most lenders allow you to borrow up to a CLTV of 80% to 85%. Some specialized programs may go higher, but staying within these bounds typically secures the best interest rates. If your home in Marietta is worth $500,000 and you owe $300,000 on your primary mortgage, an 85% CLTV would allow you to access a total of $425,000 in financing. Subtracting your existing mortgage, you could potentially secure a $125,000 line of credit.

Explore your potential numbers using our mortgage calculators to see how much equity you can safely tap.

2. Credit Score Benchmarks for Georgia Homeowners

While you might qualify for a standard mortgage with a lower credit score, HELOC lenders in Georgia typically look for a bit more stability. Most programs require a minimum credit score of 620, but to access the most competitive pricing, a score of 740 or higher is the industry gold standard.

Your credit score influences your "margin": the percentage the lender adds to the Prime Rate to determine your interest rate. A higher score means a smaller margin, which leads to lower monthly payments during your draw period.

3. The Debt-to-Income (DTI) Equation

Debt-to-Income Ratio (DTI): A percentage that represents how much of your gross monthly income goes toward paying debts.

Lenders use this to ensure you can afford the potential payments on a new line of credit. In the Atlanta market, most lenders prefer a DTI of 43% or lower. However, if you have significant equity or high cash reserves, some loan programs may allow for a DTI up to 50%.

Jump in and review your monthly obligations before applying. If you are using the HELOC for debt consolidation, some lenders will exclude the debts you are paying off from your DTI calculation, which can help you qualify for a larger amount.

4. Variable Rates and the Prime Connection

Most HELOCs are variable-rate products. This means your interest rate is tied to an index, typically the U.S. Prime Rate. When the Federal Reserve adjusts interest rates, your HELOC rate will likely follow suit.

Variable Interest Rate: An interest rate on a loan that fluctuates over time because it is based on an underlying benchmark interest rate.

For homeowners who prefer stability, some Georgia lenders offer a "fixed-rate lock" option. This allows you to convert a portion of your outstanding HELOC balance into a fixed-rate loan with a set term. This strategy is excellent for those using equity for a large, one-time expense like a kitchen remodel.

5. Atlanta Home Appraisals in a Shifting Market

To finalize your HELOC, a lender must verify your home's value. In fast-moving markets like Atlanta, Decatur, or Brookhaven, traditional appraisals can sometimes lag behind real-time sales data.

Many modern lenders now use Automated Valuation Models (AVMs) or "drive-by" appraisals to speed up the loan process. If you believe your home has unique upgrades that an automated system might miss, you might request a full interior appraisal to maximize your borrowing limit.

6. The Draw Period vs. The Repayment Period

A HELOC typically functions in two distinct phases.

- The Draw Period: Usually the first 10 years. During this time, you can take money out as needed and often have the option to make interest-only payments.

- The Repayment Period: Usually the following 15 to 20 years. You can no longer draw funds, and you must pay back both principal and interest.

Understanding this structure is vital for long-term financial planning. If you are a real estate investor using a HELOC for a fix and flip project, you likely plan to pay back the draw as soon as the property sells, avoiding the repayment phase entirely.

7. Closing Costs and Georgia Recording Fees

While many national banks advertise "no-cost" HELOCs, it is important to read the fine print. In Georgia, there are specific recording taxes and fees associated with securing a lien against your property.

Compare offers carefully. Some lenders may waive closing costs but require you to keep the line open for at least 24 to 36 months. If you close the account early, you might have to reimburse those costs. Always check the legal disclosures for any "early termination fees."

8. Strategic Use: Renovations and ROI

Atlanta homeowners often use HELOCs to improve their properties. With the cost of moving being so high, adding an ADU (Accessory Dwelling Unit) or finishing a basement is often a smarter financial move.

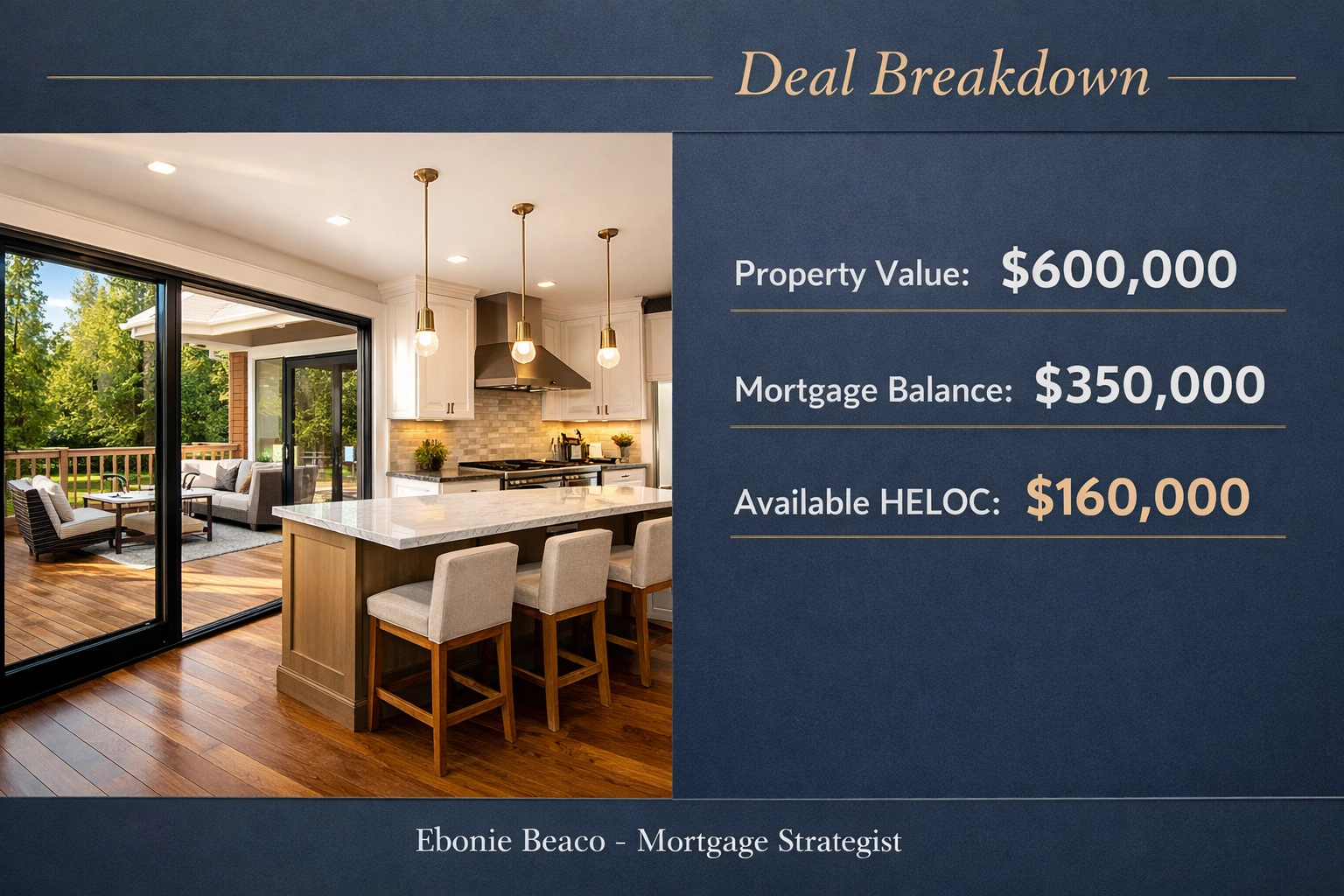

Example Scenario: Tapping Equity for an Atlanta Renovation

Let's look at how a homeowner in the North Druid Hills area might structure this.

- Current Home Value: $600,000

- Current Mortgage Balance: $350,000

- Max CLTV (85%): $510,000

- Available HELOC Limit: $160,000

The homeowner decides to draw $80,000 to renovate their kitchen and deck. Because they only pay interest on the amount they draw, their monthly cost during the renovation is significantly lower than a traditional personal loan or a fixed-rate mortgage.

9. Debt Consolidation in the Peach State

With credit card interest rates often exceeding 20%, using a HELOC to consolidate high-interest debt is a common strategy for Georgia residents. Because a HELOC is secured by your home, the interest rate is typically a fraction of what credit card companies charge.

By consolidating $40,000 of credit card debt into a HELOC, a homeowner could potentially save hundreds of dollars a month in interest charges alone. This improves monthly cash flow and helps pay down the principal balance faster.

10. HELOCs for Real Estate Investors

Georgia is a hub for real estate investment. Many landlords use a HELOC on their primary residence to fund the down payment on a DSCR rental property or a short-term rental in the North Georgia mountains.

Using your equity as a "bridge" allows you to move quickly on deals without needing to wait for a traditional cash-out refinance. Once the investment property is stabilized, you can refinance that property and pay back your HELOC, resetting your line of credit for the next opportunity.

Why Choosing a Local Strategy Matters

The Georgia real estate market has nuances that national call-center lenders often overlook. From understanding local property tax assessments to navigating Georgia’s specific closing customs, working with a strategist who understands the local landscape is a significant advantage.

Whether you are looking to tap into your equity for a home project in California, a vacation home in Florida, or a rental portfolio in Atlanta, the strategy remains the same: use your equity as a tool, not just a safety net.

Access our online forms to begin exploring how your home’s value can work for you. We provide transparent guidance to help you navigate the complexities of home equity and mortgage financing.

If you are ready to see what your Atlanta equity can do for your financial future, let's talk about your specific scenario.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664