Legally Legit: Navigating Wholesaling Contracts & Compliance

Wholesaling real estate is a powerful way to enter the investment world with limited capital. You find a distressed property, put it under contract, and then assign that contract to a cash buyer for a fee. While the concept is simple, the execution requires a deep understanding of legal boundaries. Regardless of your experience level, staying compliant is the only way to build a sustainable business.

In this course-style guide, we will break down the essential components of wholesaling contracts and the compliance rules you must follow in markets like Chicago, Florida, and California.

Module 1: Understanding Equitable Interest

The core of legal wholesaling is Equitable Interest. When you sign a purchase agreement with a seller, you do not own the bricks and mortar yet. Instead, you own a legal interest in the property defined by the contract.

Equitable Interest: A legal right to acquire legal title to a property under a signed purchase agreement. This interest is what allows you to sell the contract without being a licensed real estate agent in most jurisdictions.

If you attempt to sell the house itself without a license, you are practicing real estate brokerage without a license. This is a major legal issue. You are selling your rights to the contract, not the physical real estate.

Explore our Mortgage Basics to see how these ownership structures impact future financing for your buyers.

Module 2: The Anatomy of a Wholesaling Contract

A standard purchase agreement needs specific language to be "wholesaler friendly." Without these clauses, your deal might be dead on arrival when you try to assign it.

The "And/Or Assigns" Clause

Your contract should list the buyer as "Your Name and/or Assigns." This phrase explicitly informs the seller that you may pass the purchase rights to another party. Some state-specific contracts in places like Virginia or Georgia have pre-printed anti-assignment clauses, so you must read every line.

The Inspection Contingency

This is your exit strategy. It provides a specific timeframe (usually 7 to 14 days) to inspect the property. If your end buyer walks away or you find structural issues that kill the numbers, this clause allows you to cancel the contract and receive your Earnest Money Deposit (EMD) back.

Disclosure of Profit

Transparency is the best policy. While not required in every state, disclosing that you intend to make a profit is a best practice. In California, wholesalers must explicitly inform sellers they do not intend to purchase the property themselves in many scenarios.

Visual: A checklist of essential contract clauses for wholesalers. Text on image: Ebonie Beaco - Mortgage Strategist

Visual: A checklist of essential contract clauses for wholesalers. Text on image: Ebonie Beaco - Mortgage Strategist

Module 3: Marketing Rules and Transparency

How you talk about your deals is just as important as the contract itself. In Florida, specifically under Chapter 475.41, the law is very clear about marketing. Unlicensed wholesalers cannot market the property as if they own it.

Marketing Compliance: The practice of advertising the "assignment of contract" rather than the physical property to avoid illegal brokerage activity.

When posting on social media or sending emails to your buyers' list, use phrases like:

- "Assignment of contract for sale"

- "Purchasing the equitable interest in [Address]"

- "Contract for sale at [Price]"

Avoid saying "I have a house for sale." You don't have a house; you have a contract. This distinction is vital for staying within the law in Alabama and Michigan.

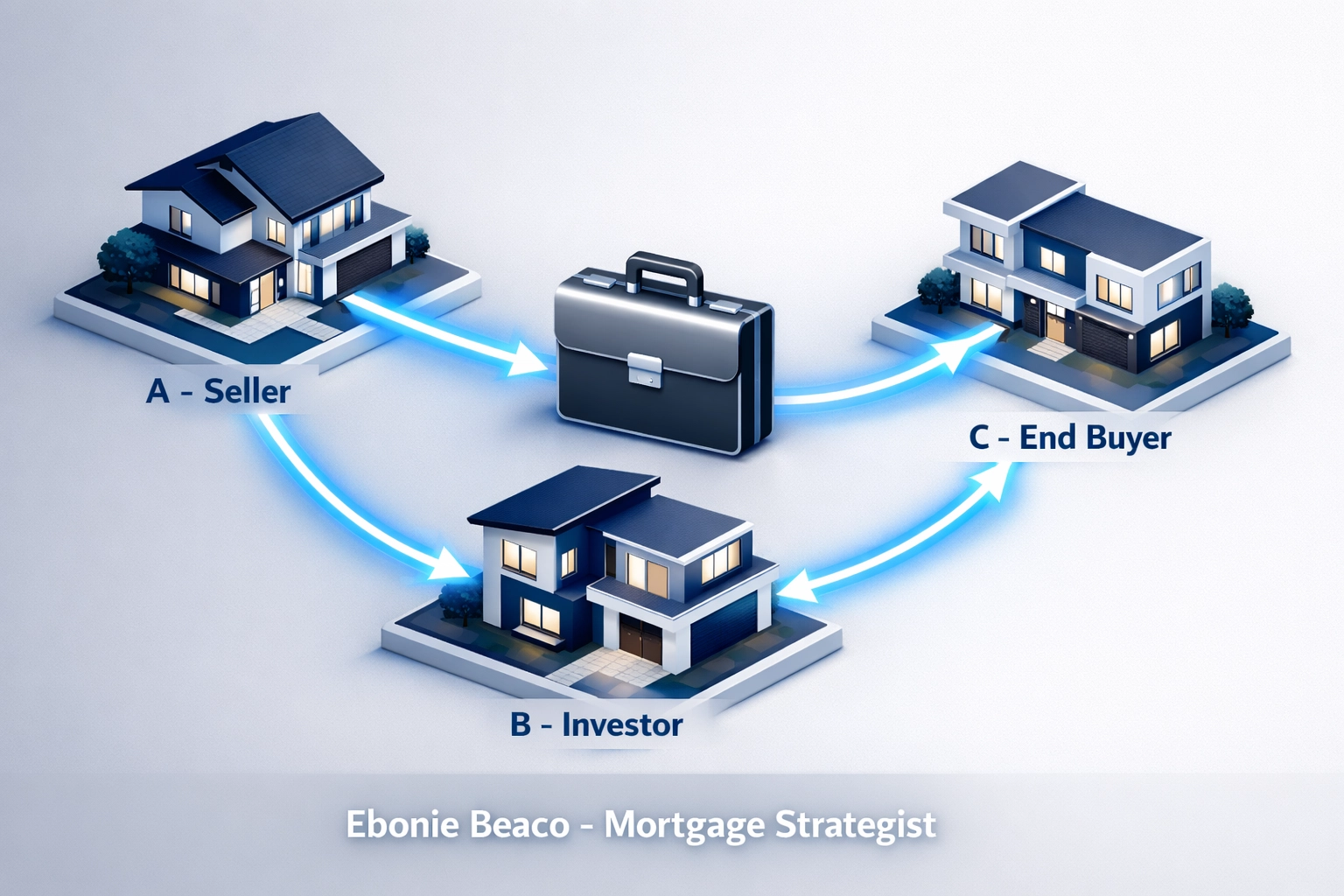

Module 4: The Role of Earnest Money (EMD)

To make a contract legally binding, there must be "consideration." In real estate, this is your Earnest Money Deposit. A contract with $0 EMD is often viewed as "illusory" and may not hold up in court if a seller tries to back out.

Consideration: Something of value exchanged between parties to form a binding contract.

In a typical wholesale deal:

- A-B Contract: You (B) provide $500 - $2,000 EMD to the Seller (A).

- B-C Assignment: Your Cash Buyer (C) provides a larger EMD (e.g., $5,000) to the title company or attorney.

This protects you. If your buyer (C) flakes, you can often use their EMD to cover your loss or your obligation to the seller. Check out our Loan Process page to understand how these funds are tracked during the closing sequence.

Visual: An infographic showing the flow of EMD from Wholesaler to Seller and End Buyer to Wholesaler. Text on image: Ebonie Beaco - Mortgage Strategist

Visual: An infographic showing the flow of EMD from Wholesaler to Seller and End Buyer to Wholesaler. Text on image: Ebonie Beaco - Mortgage Strategist

Module 5: Double Closings vs. Assignments

Depending on the state and the profit margin, you might choose a Double Closing instead of an assignment.

Assignment of Contract

This is the standard wholesale move. You sign a one-page "Assignment Agreement" with the end buyer. They pay you an assignment fee at closing. The seller sees exactly how much you are making on the HUD-1 settlement statement.

Double Closing (Simultaneous Close)

You buy the property from the seller (A-B) and immediately sell it to your buyer (B-C) in a separate transaction on the same day. This is common in Illinois for wholesalers who want to keep their profit private or if the profit is so large it might upset the seller.

Double Closing: Two distinct real estate transactions occurring back-to-back with the wholesaler acting as the bridge.

For a double closing to work, you often need Transactional Funding. This is a short-term loan that covers the A-B purchase for a few hours until the B-C funds arrive. If you are looking for long-term options for your end buyers, such as DSCR Investor Loans, we can help structure those scenarios.

Module 6: State-Specific Compliance Alerts

Legal requirements are not uniform across the country. Recent legislation has changed the landscape for wholesalers in several regions.

- Illinois: If you conduct more than one wholesale transaction within a 12-month period, you are legally required to have a real estate license. This rule is strictly enforced in Chicago.

- Arizona & Oklahoma: These states have recently introduced "Wholesaler Disclosure" requirements that mandate specific language in every contract.

- Florida: As mentioned, marketing is the primary focus. You must be careful not to trigger "unlicensed brokerage" flags.

Jump in and review our FAQ for more details on how these regional rules affect property financing.

Module 7: Disclosure Best Practices

Transparency builds trust and prevents lawsuits. A "Legally Legit" wholesaler provides the following disclosures to all parties:

- License Disclosure: If you have a real estate license, you must disclose it, even if you are acting as a principal.

- Intent Disclosure: Inform the seller that you are an investor and your goal is to make a profit.

- Role Disclosure: Make it clear to the end buyer that you are not the current owner of record, but the contract holder.

Visual: A "Legally Legit" badge next to a list of three key disclosures. Text on image: Ebonie Beaco - Mortgage Strategist

Visual: A "Legally Legit" badge next to a list of three key disclosures. Text on image: Ebonie Beaco - Mortgage Strategist

How to Stay Compliant: A Step-by-Step Checklist

If you want to run your wholesaling business like a pro, follow this workflow:

- Use Localized Contracts: Do not use generic "free" contracts from the internet. Use contracts approved by your state’s bar or real estate commission, and add your assignment addendums.

- Consult a Friendly Title Company: Work with title companies or escrow officers who understand wholesaling. They know how to handle assignment fees and double closings without hiccups.

- Vet Your Buyers: Ensure your end buyer is using cash or Fix and Flip Loans. Traditional conventional loans often have "title seasoning" requirements that prevent them from buying a wholesale deal.

- Keep Records: Save every email, text, and signed document. Compliance is about proving you did things the right way if a question arises later.

Financing the End Deal

While you are the wholesaler, your deal only closes if your buyer can fund it. Many wholesalers partner with a Mortgage Strategist to pre-vett their buyers' list. By ensuring your buyers have access to Hard Money or bridge financing, you increase your closing rate significantly.

If your end buyer needs to refinance out of a bridge loan into a long-term rental loan, they can explore our Home Refinance options to stabilize their portfolio.

Final Thoughts on Wholesaling Law

Real estate wholesaling is a legitimate business model that provides liquidity to the market and helps sellers solve problems. By focusing on equitable interest, clear disclosures, and state-specific marketing rules, you protect your reputation and your bank account.

Regardless of whether you are working in the suburbs of Indiana or the high-demand markets of California, the rules of transparency remain the same. Stay educated, stay transparent, and stay "Legally Legit."

Ready to scale your investment strategy or need a partner to help your buyers secure funding? Let's talk strategy.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664