Lease-Option vs. Land Contract: Financing Real Estate Deals

Finding the right way to close a deal when traditional bank financing isn't an immediate option is a skill every savvy investor and homeowner needs. Whether you are navigating the high-demand markets of Florida, looking for multi-unit opportunities in Chicago, or scaling a portfolio in Virginia, understanding creative financing is a game changer.

Two of the most common strategies you will encounter are the Lease-Option and the Land Contract. While they might seem similar on the surface: both involve staying in a home while working toward full ownership: they function very differently under the hood.

This guide breaks down the structural differences, financial implications, and risk profiles of each so you can decide which path aligns with your investment goals.

What is a Lease-Option?

A Lease-Option (often called rent-to-own) is a legal agreement where a tenant leases a property for a specific period and pays for the right to purchase the property at a predetermined price in the future.

The Mechanics of the Deal

In this scenario, you are a tenant first. You pay an upfront Option Fee, which is typically non-refundable. This fee grants you the exclusive right to buy the home before the lease expires.

Why Use a Lease-Option?

Jump in on a lease-option if you need time to polish your credit or wait for a cash-out refinance window. It provides flexibility without the immediate legal burdens of ownership.

What is a Land Contract?

A Land Contract (also known as a Contract for Deed) is a seller-financing agreement where the buyer makes payments directly to the seller until the purchase price is paid in full or the buyer refinances.

The Mechanics of the Deal

Unlike a lease, a land contract conveys equitable title to the buyer. You are essentially the "owner" in the eyes of the law for many purposes, even though the seller holds the deed until the final payment is made.

Why Use a Land Contract?

Explore land contracts if you are a self-employed borrower in Michigan or Indiana who has the down payment but needs to bypass traditional mortgage basics for a few years while documenting higher income.

Ownership and Equity: Who Really Owns the Property?

Understanding who holds the rights to the property is vital for your long-term strategy.

Equitable Interest vs. Possession

In a Land Contract, you gain an equitable interest from day one. This means you can often claim mortgage interest deductions on your taxes and benefit directly from property appreciation.

In a Lease-Option, you are a tenant. You have no legal ownership rights until you exercise the option and close on the sale. If you decide not to buy, you simply walk away at the end of the lease, though you lose your option fee.

Building Equity

- Land Contract: 100% of your principal payments typically go toward the purchase price, helping you build equity over time.

- Lease-Option: Monthly rent is usually just rent. Occasionally, a "rent credit" is negotiated where a portion of the monthly payment applies to the purchase price, but this is less common in today's market.

Image Instructions: Create a professional comparison table titled 'Lease-Option vs. Land Contract' showing 'Ownership', 'Equity Building', and 'Responsibility'. Ensure 'Ebonie Beaco - Mortgage Loan Officer' is at the bottom. Do not include money or cash.

Image Instructions: Create a professional comparison table titled 'Lease-Option vs. Land Contract' showing 'Ownership', 'Equity Building', and 'Responsibility'. Ensure 'Ebonie Beaco - Mortgage Loan Officer' is at the bottom. Do not include money or cash.

Maintenance and Repairs: The Hidden Costs

The responsibility for property upkeep is a major point of divergence between these two methods.

The Landlord-Tenant Relationship

In a Lease-Option, the seller remains the landlord. In most states like Illinois or California, the landlord is still responsible for major structural issues, roofing, and mechanical systems (HVAC, plumbing). As the tenant, you might handle minor repairs, but the big-ticket items stay with the owner.

The "Owner-in-Waiting"

In a Land Contract, the buyer usually takes on full responsibility for the property. If the furnace dies in a Chicago winter, it is your problem, not the seller's. This makes the land contract riskier for buyers who are not financially prepared for emergency maintenance.

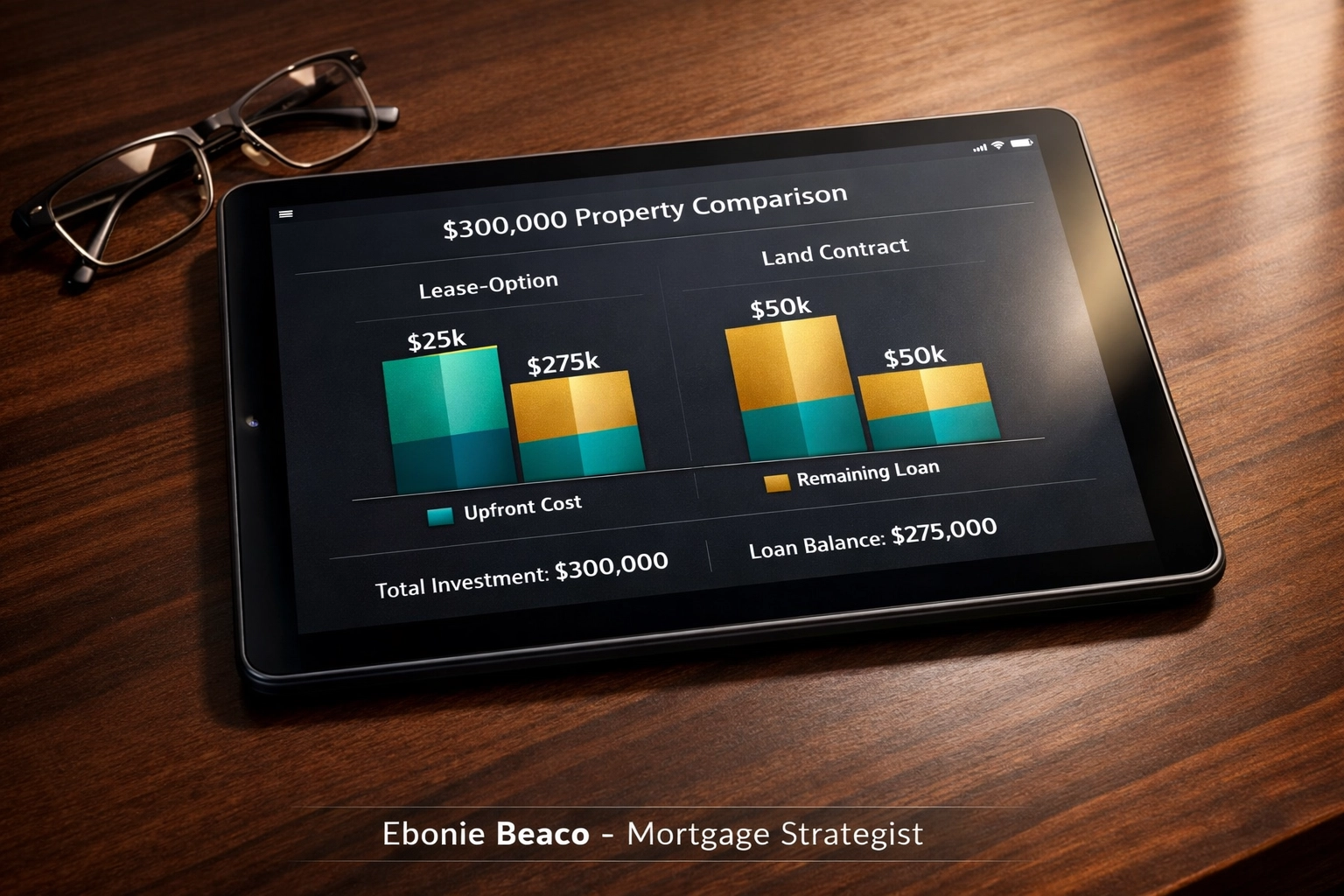

Financial Breakdown: A Real-World Scenario

Let’s look at how the numbers play out for an investor purchasing a single-family rental in Florida valued at $300,000.

Scenario A: Lease-Option

- Purchase Price: $300,000

- Option Fee (5%): $15,000

- Monthly Rent: $2,500

- Term: 24 Months

- Outcome: After 24 months, the buyer needs to secure a home purchase loan for the remaining $285,000 ($300k minus the $15k option fee).

Scenario B: Land Contract

- Purchase Price: $300,000

- Down Payment (10%): $30,000

- Monthly Payment (Interest Only at 7%): $1,575

- Term: 24 Months

- Outcome: The buyer has already paid $30,000 toward the price. After 24 months, they owe $270,000. Because they have equitable title, they may find it easier to use a DSCR investor loan to pay off the seller.

Image Instructions: A professional financial breakdown chart showing the Florida $300k scenario. Compare the Lease-Option (Option Fee $15k, Loan needed $285k) vs Land Contract (Down payment $30k, Loan needed $270k). Include labels for 'Property Value', 'Upfront Cost', and 'Remaining Balance'. Title: 'Lease-Option vs. Land Contract'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer'. No money or cash.

Image Instructions: A professional financial breakdown chart showing the Florida $300k scenario. Compare the Lease-Option (Option Fee $15k, Loan needed $285k) vs Land Contract (Down payment $30k, Loan needed $270k). Include labels for 'Property Value', 'Upfront Cost', and 'Remaining Balance'. Title: 'Lease-Option vs. Land Contract'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer'. No money or cash.

Risk of Default and Exit Strategies

What happens if you can't make the payments? The answer depends heavily on which contract you signed.

Ease of Eviction

For a Lease-Option, if you miss your rent, the owner can typically file for a standard eviction. The process is relatively fast, and you lose your option fee and any rent credits.

The Foreclosure Process

In a Land Contract, because you have equitable title, many states (like Kentucky or Arkansas) require the seller to go through a formal foreclosure process to get you out. This takes much longer than an eviction and provides the buyer more time to catch up or sell the property to satisfy the debt.

Accessing Permanent Financing

The ultimate goal for most people using these strategies is to eventually move into a permanent mortgage.

Refinancing a Land Contract

Lenders often view a land contract payoff as a "rate and term refinance" rather than a new purchase if you have been on title for at least 12 months. This can sometimes lead to better rates or lower down payment requirements.

Financing a Lease-Option Purchase

A lease-option exercise is treated as a standard home purchase transaction. You will need to meet all standard underwriting guidelines, including appraisal and credit requirements, at the time you exercise the option.

If you are a self-employed investor, you might look into Non-QM Mortgage Loans or bank statement loans to bridge the gap when your tax returns don't show enough income for traditional qualifying.

Which Strategy Fits Your Portfolio?

The "better" option depends entirely on your specific situation and the local market activity.

- Choose a Lease-Option if: You want a lower upfront commitment, you aren't ready for maintenance responsibilities, or you want the flexibility to walk away if the market dips.

- Choose a Land Contract if: You want to build equity immediately, you intend to keep the property long-term, and you want the tax benefits associated with ownership.

Real estate investors in Alabama, Georgia, and Virginia often use these methods to secure properties that need work before they can qualify for traditional DSCR rental property loans.

Professional Guidance for Creative Deals

Creative financing requires a clear strategy. Navigating the legal nuances of land contracts in the Midwest versus lease-options in the Sunbelt is much easier when you have an expert in your corner. Whether you are a wholesaler looking to move a deal or a first-time investor trying to get your foot in the door, the right loan structure is key.

If you are unsure which path to take, or if you are ready to transition from a creative contract into a permanent mortgage, let's talk about your options. Access professional advice to ensure your deal is structured for success.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

For more information on the loan process and how to prepare for your next investment, visit our FAQ page or explore our mortgage calculators to run your own numbers.