Late-Day Market Volatility: Why Today’s 4:00 PM Mortgage News Update Is Crucial

Navigating the mortgage landscape requires more than just a passing glance at weekly averages. In a financial environment defined by rapid shifts, the closing bell of the bond market often dictates the lending terms you receive the following morning. As of Thursday, May 21, 2026, we are witnessing a unique intersection of geopolitical tension and domestic economic data that makes the 4:00 PM market update essential for every real estate investor and homeowner.

The current mortgage climate is heavily influenced by the Federal Reserve’s third consecutive rate freeze in 2026. While inflation figures have shown some resilience with the April CPI coming in at 3.8% year-over-year, the market is bracing for a "higher for longer" policy stance. For those operating in states like Illinois, Florida, and Virginia, understanding these intraday fluctuations is the difference between securing a viable deal or missing a window of opportunity.

The Impact of Geopolitics on Mortgage Rates

Global events frequently trigger immediate reactions in the U.S. Treasury market, which directly correlates to mortgage pricing. Recent developments in the Middle East, specifically involving energy supply chains, have created upward pressure on oil prices, feeding directly into inflationary fears. When bond yields spike in response to these headlines, mortgage lenders often adjust their rate sheets multiple times in a single afternoon.

Market Volatility: The frequency and magnitude of price changes in a financial instrument over a specific period. In practical application, high volatility means a rate quoted at 10:00 AM in Chicago might be obsolete by the time the West Coast markets close at 4:00 PM.

Analyzing Today's National Rate Environment

As we look at the data for late May 2026, the 30-year fixed-rate mortgage is hovering in the 6.5% to 6.7% range. While this is a significant improvement from the peaks seen in mid-2024, it remains elevated compared to the historic lows of the early 2020s. Freddie Mac reports a weekly average of 6.51%, though intraday trading has shown moments of downward movement when peace process headlines emerge.

Explore the latest trends through Freddie Mac’s Primary Mortgage Market Survey to compare how today’s figures align with historical data. You will find that while rates are higher than the 2021 floor, the moderate volatility index (currently 3 out of 10) provides a level of predictability that was absent last year. This stability allows landlords and developers in Alabama and Michigan to plan their acquisitions with greater confidence.

Strategic Financing for Real Estate Investors

For those looking to scale a portfolio, traditional financing is not always the most efficient path. Non-QM Mortgage Loans and DSCR Investor Loans have become the primary tools for sophisticated buyers in high-demand markets like Atlanta or Miami. These programs allow you to qualify based on the property’s performance rather than your personal debt-to-income ratio.

DSCR (Debt Service Coverage Ratio): A financial metric used to measure a property's ability to cover its debt obligations with its own rental income. Investors use this to acquire properties without providing tax returns or W-2s, focusing instead on the net operating income of the asset.

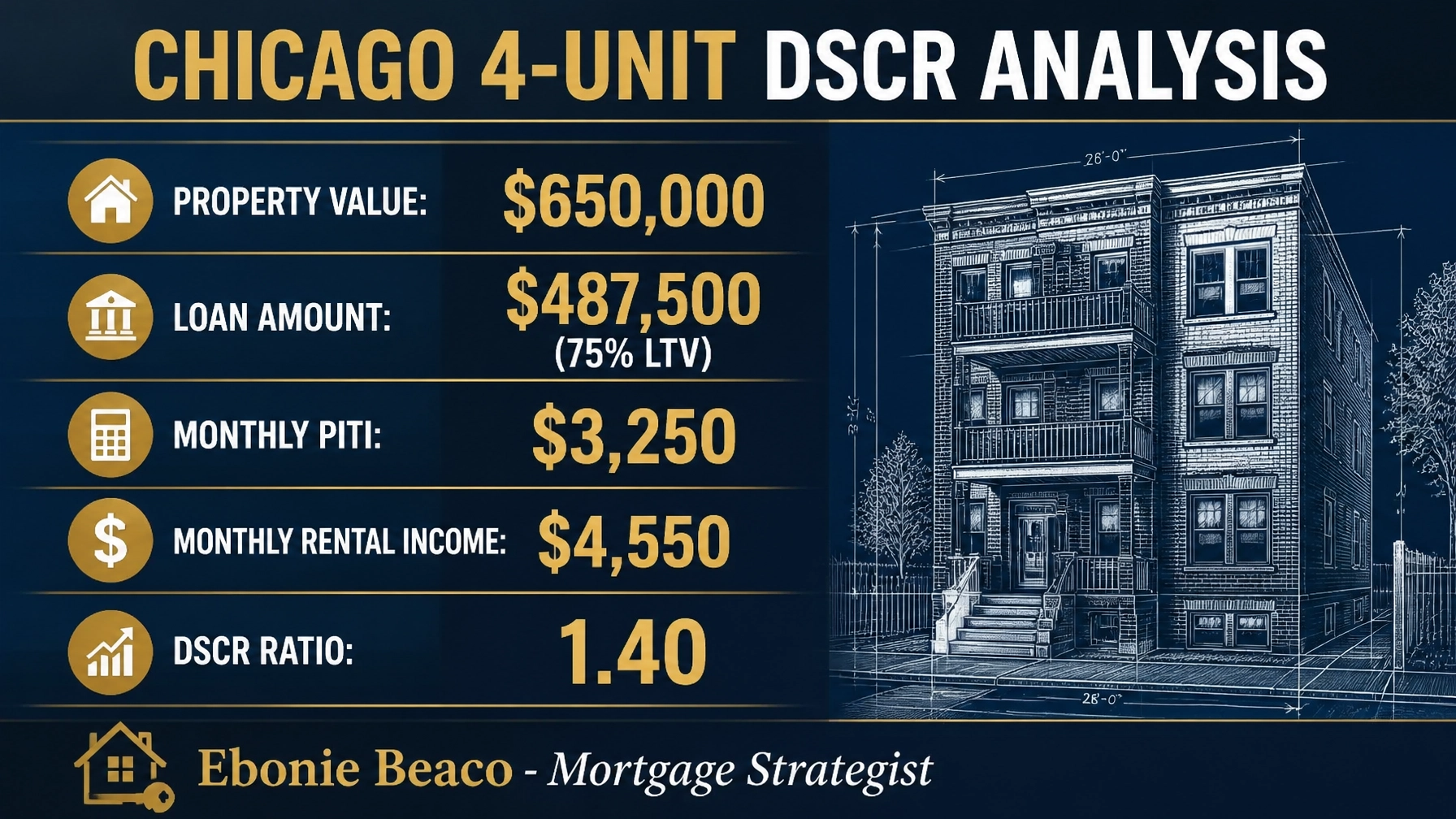

Chicago 4-Unit Investment Scenario

Jump into a practical example of how a DSCR loan functions in a market like Chicago. Imagine a multi-unit building with a property value of $650,000. If you secure a loan at 75% LTV ($487,500), your monthly principal, interest, taxes, and insurance (PITI) might total $3,250. If the gross monthly rental income is $4,550, your DSCR ratio is 1.40.

A ratio above 1.25 is typically considered strong, often unlocking better interest rate tiers. This strategy is particularly effective for Airbnb and short-term rental financing, where the income potential often far exceeds traditional long-term lease rates. By focusing on the asset's cash flow, you can continue to expand your portfolio even when personal income documentation might limit your borrowing capacity at a traditional bank.

Tapping into Home Equity in 2026

Homeowners in high-appreciation states like California and Florida are sitting on record levels of equity. Even with current rates in the 6% range, a Cash-Out Refinance or a HELOC remains a powerful tool for debt consolidation or funding your next down payment. Accessing these funds requires a clear understanding of your current Loan-to-Value (LTV) limits.

Cash-Out Refinance: A mortgage refinancing option where the new loan is for a larger amount than the existing mortgage, and the difference is paid to the borrower in cash. This allows you to extract liquid capital for renovations or to purchase additional investment properties.

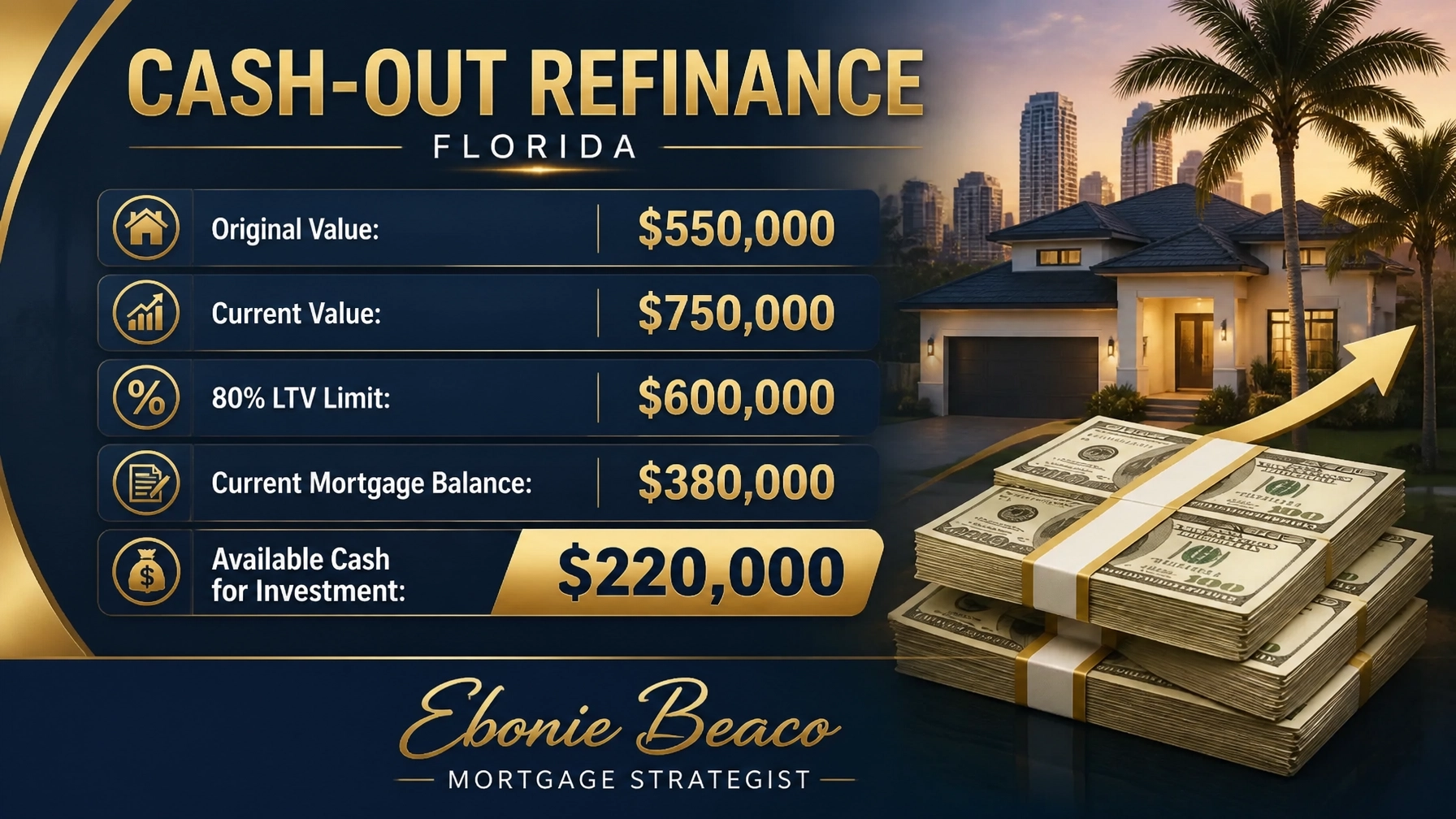

Florida Equity Extraction Example

Compare your current position to a typical scenario in Orlando or Tampa. If your home is valued at $750,000 and you have a current mortgage balance of $380,000, you have significant untapped wealth. Most lenders allow an 80% LTV limit, which in this case is $600,000. By refinancing, you could potentially access $220,000 in available cash to fuel your next business venture or investment.

Fix and Flip Financing Strategies

The "Fix and Flip" market continues to thrive in suburban areas of Indiana and Missouri, where inventory remains tight. For these projects, speed is often more vital than the interest rate. Fix and Flip Loans and Bridge Loans provide the short-term capital needed to acquire distressed assets and fund renovations quickly.

Bridge Loan: A short-term loan used until a person or company secures permanent financing or removes an existing obligation. This is the go-to solution for investors who need to close on a new property before their current one sells or before a long-term DSCR loan can be finalized.

In a typical fix-and-flip deal, an investor might purchase a property for $300,000 with a renovation budget of $100,000. If the After Repair Value (ARV) is projected at $550,000, the financing is structured around the future value rather than the current condition. This allows you to leverage the lender's capital to maximize your Return on Investment (ROI) while keeping your personal liquidity intact.

Why the 4:00 PM Update Closes the Loop

The final hour of the trading day is when the most significant re-pricing occurs. When positive economic news drops late in the afternoon, lenders may offer an "intraday gift," allowing you to lock in a rate that is lower than the morning's opening quotes. Conversely, if inflation data surprises to the upside, rates can climb before the day ends.

Access real-time updates and market analysis through tools like Bankrate’s Mortgage Rate Index to stay ahead of these shifts. For realtors and wholesalers, being able to advise a client on these late-day moves builds immense trust and ensures that contracts are structured with accurate financial data.

Whether you are a first-time homebuyer in Kentucky or a seasoned portfolio investor in Virginia, the 4:00 PM update is your final opportunity to evaluate the day's trend before the markets reset. Understanding the "why" behind these moves empowers you to make decisions based on data rather than speculation.

Resolve your financing uncertainty today and get the guidance you need for your next transaction.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664