Late-Day Market Shifts: Why Today’s Mortgage News Impacts Your Closing Strategy

Navigating the mortgage market requires more than just checking a weekly average; it demands a real-time understanding of daily shifts. On this Friday, May 22, 2026, we are witnessing significant late-day movement in the bond market that directly influences the cost of your home loan.

Whether you are a first-time homebuyer in Chicago, a seasoned real estate investor in Florida, or a homeowner in Virginia looking to tap into equity, these intraday fluctuations dictate your final numbers. Staying ahead of these shifts allows you to lock in a rate before a mid-day repricing for the worse occurs.

Explore the mechanics of today’s market to ensure your financing strategy remains aligned with your long-term wealth goals. Jump in to understand how the latest data from the bond market is shaping mortgage opportunities across the country.

Understanding the Intraday Repricing Phenomenon

Most borrowers assume that mortgage rates are set once a day and remain static until the next morning. In reality, mortgage lenders monitor the bond market continuously and may issue new rate sheets at any hour.

Repricing for the Better: A scenario where bond prices rise, leading lenders to lower mortgage rates or reduce closing costs during the business day.

This occurs when economic data suggests a slowing economy, causing investors to seek the safety of bonds.

Repricing for the Worse: A sudden increase in mortgage rates or costs issued by a lender in response to falling bond prices.

If a late-morning economic report is stronger than expected, lenders often hike rates immediately to protect their margins.

Accessing real-time updates is essential for anyone currently in the "float" stage of their loan application. A shift of even 0.125% in the late afternoon can result in thousands of dollars in additional interest over the life of a thirty-year loan.

The Bond Market Ripple Effect

The mortgage industry does not operate in a vacuum; it is tethered to the performance of Mortgage-Backed Securities (MBS) and the 10-year Treasury yield. When you see news about the Treasury market shifting late in the day, you should anticipate a reaction in the mortgage space.

MBS (Mortgage-Backed Securities): An investment vehicle consisting of a bundle of home loans and other real estate debt bought from the banks that issued them.

The price of these securities moves inversely to mortgage rates; when MBS prices fall, mortgage rates typically rise.

10-Year Treasury Yield: The interest rate the U.S. government pays to borrow money for a decade, which serves as a primary benchmark for long-term mortgage rates.

Investors watch this yield closely because as it climbs, mortgage rates almost always follow suit within hours.

Today’s late-day shift is a reminder that the window to capture a favorable rate can close in a matter of minutes. Compare your current quote with the latest market averages to determine if a lock-in is your best move right now.

Regional Housing Activity and Investment Trends

The impact of late-day market shifts is felt differently depending on the local housing inventory and buyer demand in your specific region. We are currently observing unique trends in several key states where Home Loans Network provides expert guidance.

Illinois and the Chicago Metro Area

In Chicago, the market remains competitive for multi-unit properties and single-family homes in established neighborhoods. Buyers are utilizing conventional loans and FHA financing to navigate the current rate environment while inventory remains tight.

Florida and the Southeast

Cities across Florida, including Orlando and Tampa, continue to see high demand for Airbnb and short-term rental financing. Investors in Florida often utilize DSCR loans to acquire properties based on projected rental income rather than personal debt-to-income ratios.

California and Virginia

High-balance markets in California and Northern Virginia require sophisticated financing solutions such as Jumbo loans and Non-QM mortgage products. These borrowers are particularly sensitive to rate shifts, as a small percentage move has a massive impact on large loan balances.

Arkansas, Indiana, and Michigan

In these states, we see a surge in first-time homebuyer activity supported by down payment assistance programs. These buyers rely on stable rates to meet strict debt-to-income (DTI) requirements for qualification.

Strategy: Accessing Home Equity via HELOC

Homeowners in states like Alabama, Kentucky, and Missouri have seen significant property appreciation over the last few years. One of the most effective ways to utilize this wealth is through a Home Equity Line of Credit (HELOC).

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home as needed.

This is a flexible tool for home renovations, debt consolidation, or as a down payment for a second investment property.

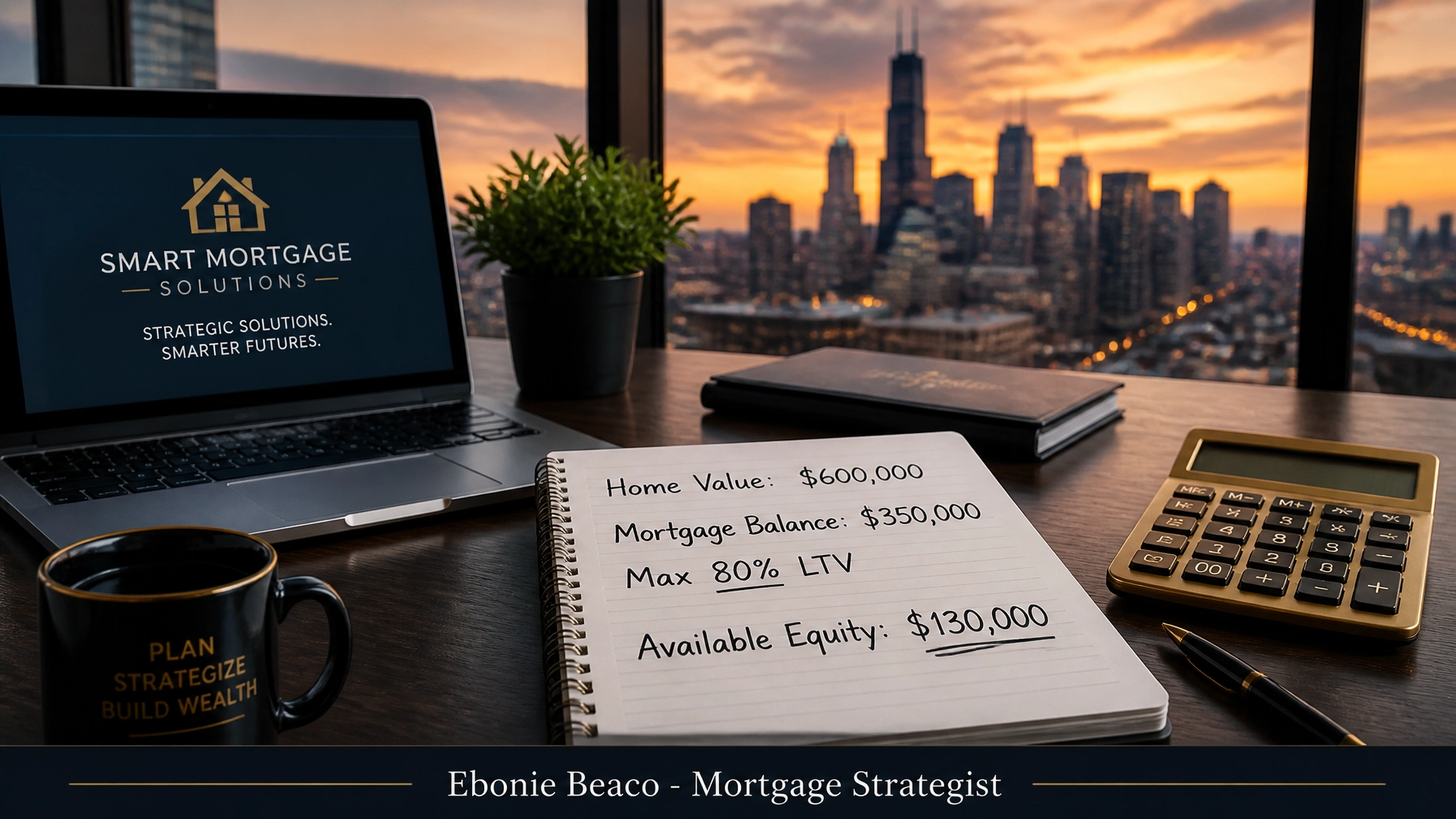

Financial Example: HELOC Equity Extraction

Consider a homeowner in Georgia with a primary residence valued at $600,000. They have an existing mortgage balance of $350,000 and want to access cash for a renovation.

- Property Value: $600,000

- Max Loan-to-Value (LTV): 80% ($480,000)

- Current Mortgage: $350,000

- Available HELOC Limit: $130,000

By establishing a HELOC, this homeowner gains access to $130,000 without disturbing their low interest rate on the primary $350,000 mortgage.

Strategy: Scaling Portfolios with DSCR Loans

Real estate investors in markets like St. Louis, Missouri or Indianapolis, Indiana are increasingly moving away from traditional bank financing. They are choosing DSCR (Debt Service Coverage Ratio) investor loans to scale their portfolios quickly.

DSCR (Debt Service Coverage Ratio): A metric used by lenders to determine a property's ability to cover its own debt based on rental income.

Unlike traditional loans, DSCR financing does not require tax returns or employment verification, making it ideal for self-employed investors.

Financial Example: DSCR Rental Acquisition

An investor is looking to purchase a four-unit building in a growing Florida neighborhood for $500,000. The lender requires the property to generate enough income to cover the mortgage, taxes, and insurance.

- Gross Monthly Rent: $4,500

- Monthly Mortgage Payment (PITI): $3,200

- DSCR Calculation: $4,500 / $3,200 = 1.40

A DSCR of 1.40 is considered strong, as most lenders only require a 1.20 or 1.25 ratio. This allows the investor to secure the property based on the asset's performance.

Navigating Late-Day News for Your Closing

When a major economic report or Federal Reserve announcement drops in the afternoon, it can trigger a wave of market activity. For those with a closing date on the horizon, these moments are critical for your financial outcome.

Today's news highlights the importance of working with a mortgage strategist who monitors these technical shifts. According to the Mortgage News Daily data for May 22, 2026, 30-year fixed rates are hovering near 6.65%, showing the volatility we have come to expect this season.

Furthermore, Freddie Mac’s economic research suggests that while growth has moderated, the bond market remains highly reactive to inflation data. This means that a "wait and see" approach can sometimes lead to missing the optimal window to lock your rate.

Final Expert Guidance

Do not let intraday volatility derail your homeownership or investment goals. By understanding how late-day shifts influence your mortgage quote, you can make informed decisions with confidence.

Explore your options for cash-out refinancing if you have built substantial equity, or look into fix-and-flip financing if you are targeting distressed properties in Michigan or Indiana. Every market shift creates a new opportunity for those who are prepared to act.

Compare different loan programs and structure your deal to maximize your cash flow and long-term equity. Whether you are buying a condo in Chicago or a commercial building in Virginia, your financing strategy is the foundation of your real estate success.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664