Kentucky HELOC Secrets Revealed: How to Fund a Massive Renovation Without Touching Your Low Mortgage Rate

You likely have a mortgage rate that feels like a prize you won years ago.

Many homeowners across Kentucky, Indiana, and Illinois are sitting on interest rates below 4%.

The idea of trading that low rate for a new, higher-rate mortgage just to get some cash for a renovation feels like a step backward.

But your house needs work.

Maybe the kitchen is dated, the basement is unfinished, or you need an extra bedroom for a growing family.

There is a way to access your home's equity without disturbing your primary mortgage.

It is the strategic use of a Home Equity Line of Credit (HELOC).

This financial tool allows you to tap into your home's value while keeping your existing low-rate mortgage exactly where it is.

The Homeowner's Dilemma: The "Golden Handcuffs"

The "Golden Handcuffs" is a term used to describe homeowners who feel trapped by their low interest rates.

You want to move or improve, but the cost of financing a new project through a traditional refinance is too high.

A Cash-Out Refinance replaces your entire mortgage with a new one at current market rates.

If you owe $200,000 at 3% and need $50,000 for a renovation, a refinance would mean paying today's rates on the full $250,000.

That is an expensive way to borrow $50,000.

A HELOC operates differently.

It sits in a second lien position behind your main mortgage.

Your 3% rate stays on your first mortgage, and you only pay the current market rate on the money you actually use from the HELOC.

Explore your options without losing your low rate by speaking with a mortgage strategist.

Defining the HELOC

HELOC (Home Equity Line of Credit): A revolving line of credit secured by the equity in your home that allows you to borrow, repay, and borrow again.

Practical application: Use it like a credit card for your house, drawing only what you need for each phase of a renovation project.

LTV (Loan-to-Value): The ratio between the total amount of loans on a property and its appraised value.

Practical application: Lenders use this to determine how much equity you can actually access.

DTI (Debt-to-Income): A percentage that represents how much of your monthly income goes toward paying debts.

Practical application: Keeping this below 43% generally makes it easier to qualify for a Kentucky HELOC lender's best terms.

Why Renovations and HELOCs are a Perfect Match

Renovations rarely happen all at once.

You pay a contractor a deposit, then a mid-point payment, and a final payment upon completion.

If you took out a traditional home equity loan, you would receive a lump sum and pay interest on the whole amount from day one.

With a HELOC, you only draw the funds as you need to pay your bills.

If your kitchen remodel costs $60,000 but the first installment is only $10,000, you only pay interest on that $10,000.

This flexibility is why many homeowners in Kentucky, Indiana, and Michigan prefer this route for large scale improvements.

It allows for better cash flow management during the construction process.

Jump in and see how much equity you can access for your next project.

Calculating Your Borrowing Power: A Real-World Example

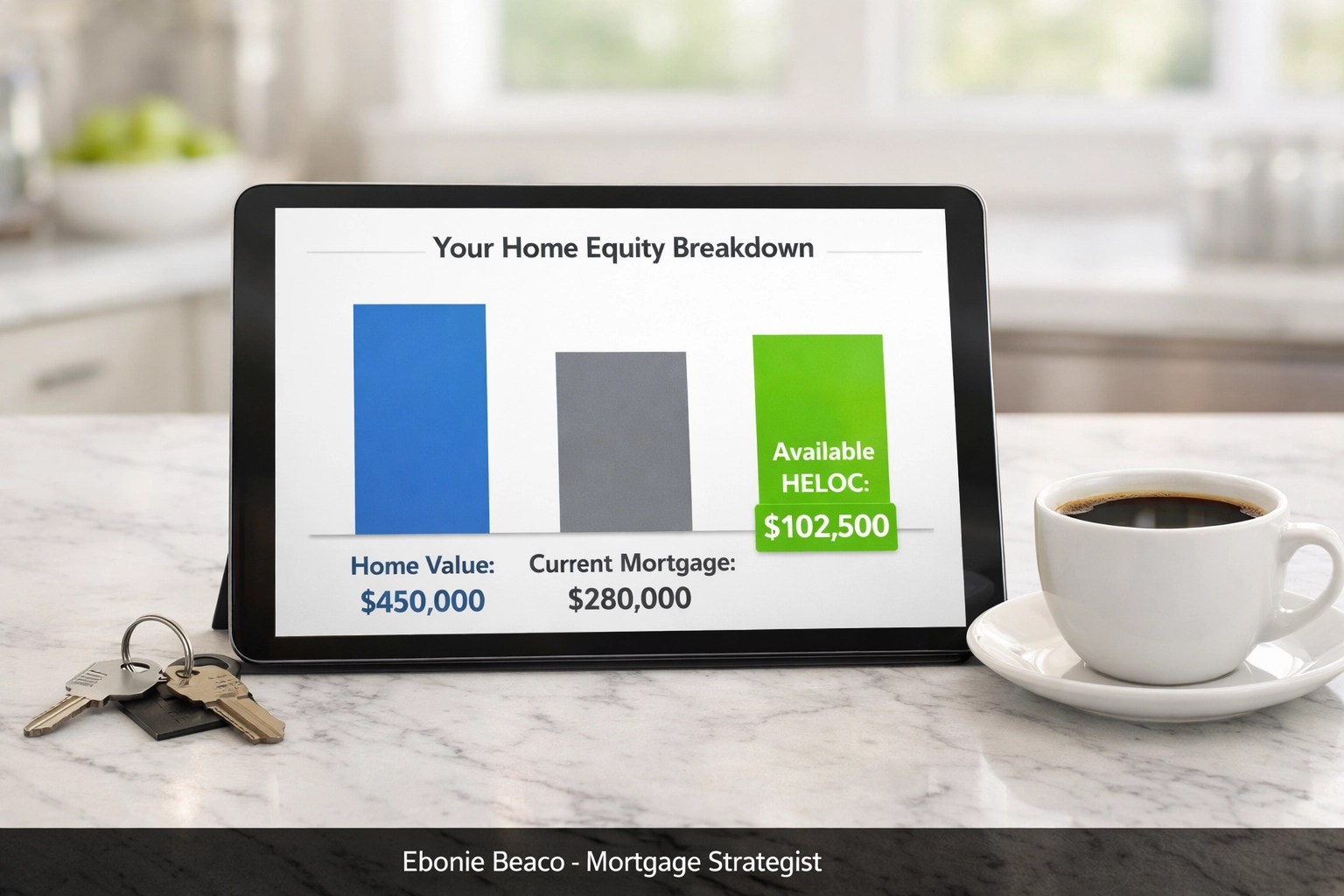

Let's look at a typical scenario for a homeowner in a growing market like Louisville, KY or Indianapolis, IN.

Imagine your home is currently valued at $450,000.

You have a remaining balance on your first mortgage of $280,000 at a 3.25% interest rate.

Most lenders will allow you to go up to an 85% Combined Loan-to-Value (CLTV).

Step 1: Calculate the Maximum Total Debt

$450,000 (Value) x 0.85 (LTV Limit) = $382,500

Step 2: Subtract Your Current Mortgage

$382,500 (Max Debt) - $280,000 (Current Mortgage) = $102,500

In this scenario, you could potentially access a line of credit for $102,500.

You can use this entire amount or just a small portion of it.

Best of all, that $280,000 mortgage stays at 3.25% and remains untouched.

The Kentucky and Indiana Market Advantage

Home values in the Midwest and South have seen steady appreciation over the last few years.

If you bought your home in Virginia, Georgia, or Alabama five years ago, you likely have significantly more equity than you realize.

Cities like Chicago, IL and various metropolitan areas in Florida and California have also seen equity surges.

As a Kentucky HELOC lender, we see homeowners using these funds to add value back into their properties.

Adding a primary suite or finishing a basement doesn't just make the house more livable; it often increases the resale value.

By using a HELOC, you are essentially reinvesting your home's own value back into the asset.

Access local market insights and equity strategies by connecting with our team.

The Structure of a HELOC: Draw vs. Repayment

A HELOC is typically split into two distinct phases.

The first phase is the Draw Period, which usually lasts 10 years.

During this time, you can take money out as needed and usually only have to make interest-only payments.

This keeps your monthly costs low while you are in the middle of a messy and expensive renovation.

The second phase is the Repayment Period, which often lasts 20 years.

Once the draw period ends, you can no longer take money out.

Your monthly payments will then include both principal and interest to pay off the balance over the remaining term.

Understanding this timeline is vital for long-term financial planning.

Compare different HELOC structures to find the one that fits your renovation timeline.

Qualifying for Your Renovation Funds

When you apply with an Indiana HELOC lender or a lender in Missouri or Arkansas, the requirements are similar to a standard mortgage.

Lenders will look at your credit score, with a 680 or higher usually being the threshold for better rates.

They will verify your income and look at your DTI ratio.

An appraisal is often required to confirm the current value of the property.

You can learn more about how appraisals work at https://www.homeloansnetwork.com/mortgage-basics/appraisals.

Because a HELOC is a "second" mortgage, the lender is taking a bit more risk than the first mortgage holder.

This is why they are often more diligent about checking your ability to repay.

Review our application checklist to prepare for your equity draw: https://www.homeloansnetwork.com/mortgage-basics/application-checklist

Strategies for Real Estate Investors

If you are a real estate investor using the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), a HELOC can be a game-changer.

Investors often have significant equity tied up in their primary residences.

You can use a HELOC on your home to provide the down payment or renovation funds for an investment property in California, Florida, or Virginia.

This allows you to scale your portfolio without needing to save up massive amounts of cash from your 9-to-5 income.

Many landlords also use HELOCs as an emergency fund for their rental portfolios.

Having a line of credit available means you can handle a major repair: like a roof replacement or a new HVAC system: without disrupting your cash flow.

Explore investor-specific financing strategies at https://www.homeloansnetwork.com/mortgage-basics.

Tax Considerations and Interest

While we are not tax professionals, it is important to note that the interest on a HELOC may be tax-deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan.

Using the money to pay off credit cards or buy a boat usually does not offer the same tax benefits.

Always consult with a tax advisor to understand how this applies to your specific situation in Kentucky or Indiana.

Transparency in your financial planning is the key to long-term success.

Ask questions about how a HELOC fits into your total financial picture.

Moving Forward With Your Renovation

Renovating your home should be an exciting milestone, not a source of financial stress.

You don't have to sacrifice your low mortgage rate to get the house you’ve always wanted.

By tapping into your equity through a HELOC, you maintain your financial foundation while building for the future.

Whether you are in Louisville, Lexington, Indianapolis, or Chicago, the equity in your home is a powerful tool.

Use it wisely, and it can fund the massive renovation you've been dreaming of.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664