June Rates Update: How This Morning’s News Affects Florida and California Investment Loans

The mortgage market experienced a sharp reaction this morning following the release of the June employment report. Data showing stronger than expected job growth and wage increases has immediately influenced bond yields, creating upward pressure on mortgage interest rates across the country. For real estate investors in high-price markets like California and Florida, these shifts require immediate attention as they directly impact the affordability and cash flow of upcoming acquisitions. While the Federal Reserve remains cautious, the secondary market is pricing in a "higher for longer" environment that changes the math for rental property financing.

Home Loans Network closely monitors these daily fluctuations to provide clarity for homeowners and professional investors navigating the lending landscape. Understanding how national economic data translates into local borrowing costs is essential for maintaining a competitive edge in states like Alabama, Arkansas, and Michigan. When the economy shows unexpected strength, mortgage backed securities often face sell-offs, which leads to higher rates for conventional, jumbo, and Non-QM loan programs. This morning's news serves as a reminder that the window for securing lower-cost capital can shift within hours based on a single government report.

Decoding Today’s Economic Impact

The relationship between employment data and mortgage rates is often counterintuitive for those outside the finance industry. A "hot" jobs report, characterized by high hiring numbers, suggests that the economy is still growing at a pace that could sustain or increase inflation. Since inflation erodes the value of fixed-income investments, lenders demand higher yields to compensate for the risk, which results in the higher mortgage rates we are seeing today. According to the Mortgage News Daily gauge, the 30-year fixed rate is currently testing the highest levels seen so far in 2026.

Investors should note that the impact of this volatility is not distributed equally across all loan types or geographic regions. Markets in California and Florida, where loan balances are frequently in the jumbo or super-jumbo range, feel the weight of even a small increase in basis points more heavily than lower-cost markets. A 0.25% increase on a $1,200,000 investment loan in Los Angeles or Miami represents a significantly larger monthly payment increase than the same move on a property in Indiana or Kentucky. Staying informed on these trends allows you to decide whether to lock in a rate now or wait for potential stabilization later in the month.

Key Financial Definitions for Investors

Basis Points (BPS)

Definition: A unit of measure used in finance to describe the percentage change in the value of financial instruments or the rate of return on investments.

Application: One basis point is equal to 0.01%, meaning 100 basis points equals 1%, and lenders often use this term to describe small daily movements in mortgage interest rates.

Debt Service Coverage Ratio (DSCR)

Definition: A financial metric used to evaluate a property's ability to cover its debt obligations with its rental income.

Application: Investors use the DSCR to qualify for specialized rental property loans without having to provide personal income tax returns or employment verification.

Loan-to-Value (LTV)

Definition: The ratio of a loan amount to the appraised value of the property, expressed as a percentage.

Application: Lenders use LTV to assess risk levels, where a higher LTV typically results in higher interest rates or more stringent qualification requirements for the borrower.

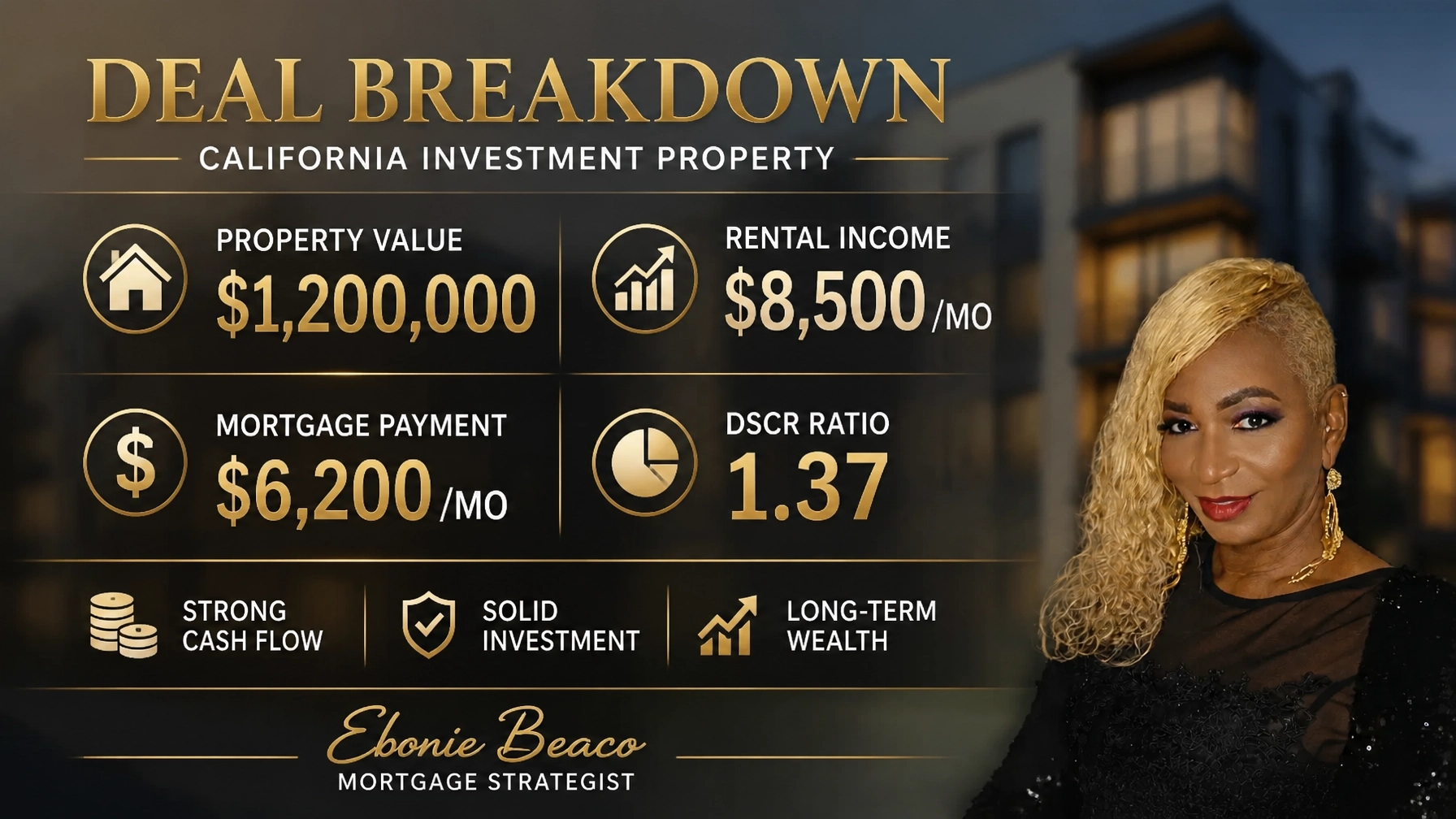

Assessing the California Multi-Unit Market

Investors in California often utilize DSCR loans to acquire small multifamily properties, such as duplexes and four-unit buildings. These loans are particularly popular in cities like Los Angeles, San Diego, and San Francisco because they focus on the property's performance rather than the investor's debt-to-income ratio. However, as interest rates rise, the income generated by the property must also be higher to maintain a healthy DSCR. If the rental income does not increase at the same pace as the financing costs, you may find that the maximum loan amount you can qualify for begins to decrease.

As demonstrated in the calculation above, a property valued at $1,200,000 with a monthly rental income of $8,500 requires a specific mortgage payment to remain viable for most lenders. At today’s updated rates, if the mortgage payment rises to $6,200, the DSCR would sit at approximately 1.37. While this remains a strong ratio for most programs, a further increase in rates could push that payment higher, potentially lowering the DSCR toward the 1.20 or 1.25 threshold that many lenders require as a minimum. For California investors, this morning's news might mean the difference between a 75% LTV and a 70% LTV on your next acquisition.

Strategies for Florida Real Estate Portfolios

In Florida, the real estate market continues to attract significant interest from both long-term rental investors and short-term rental operators in coastal areas. Many of these investors rely on cash-out refinance strategies to unlock equity from their existing properties to fund new purchases or renovations. When mortgage rates jump following a strong jobs report, the cost of that equity becomes more expensive. It is important to compare the benefits of a cash-out refinance against other options like a Home Equity Line of Credit (HELOC) to determine which path provides the most efficient access to capital.

For example, consider a Florida rental property currently valued at $650,000 with a remaining mortgage balance of $300,000. Under a 75% LTV cash-out refinance program, you could potentially access a new loan of $487,500, providing $187,500 in liquid cash for your next investment. Even with the slight rate increase seen today, this strategy often remains more effective than selling a property and paying capital gains taxes. Home Loans Network helps investors across Florida, from Jacksonville to Miami, analyze these scenarios to ensure your equity is working as hard as possible for your long-term wealth goals.

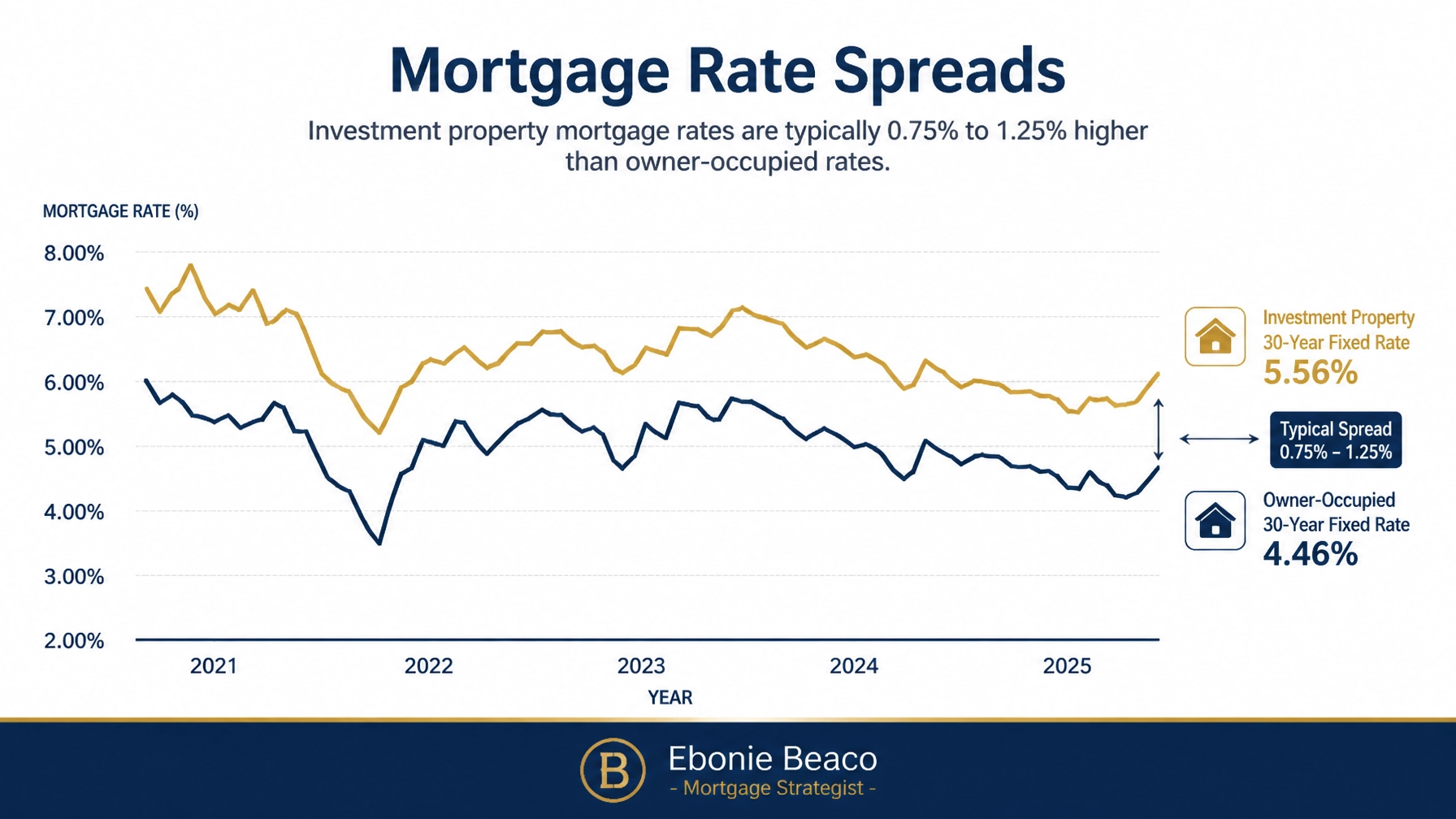

Navigating Rate Spreads for Investment Loans

It is a common observation in the mortgage industry that investment property loans carry higher interest rates than owner-occupied mortgages. This difference, often referred to as the "rate spread," exists because lenders perceive investment properties as carrying higher risk than a borrower's primary residence. During periods of economic uncertainty or rapid rate movements, these spreads can widen as secondary market investors become more conservative. Understanding this gap is crucial when you are researching national averages, as the rates quoted in mainstream news are almost exclusively for prime, owner-occupied borrowers.

Current data suggests that investment rates are typically 0.75% to 1.25% higher than their owner-occupied counterparts. When news like this morning's jobs report pushes the standard 30-year fixed rate toward 6.50% or higher, investors should be prepared to see quotes in the 7.25% to 8.00% range depending on the specific loan program. According to Freddie Mac’s weekly survey, the trend line for these spreads has remained relatively consistent, but the absolute cost of borrowing continues to climb. We encourage investors in Georgia, Virginia, and Missouri to factor these spreads into their pro-forma projections before submitting offers on new properties.

Financing Solutions Beyond the Conventional Market

While the morning’s news impacts the entire financial sector, different loan programs react with varying levels of sensitivity. Non-QM mortgage loans, including bank statement loans for self-employed borrowers and ITIN mortgage loans, often have different pricing drivers than conventional loans. This means that while Fannie Mae and Freddie Mac rates might jump immediately, some private money or portfolio lenders may adjust their rates on a slightly different schedule. This provides a strategic window for borrowers who are ready to move quickly on a deal.

Explore these popular options for your next real estate transaction:

- DSCR Investor Loans: Focus on rental income for qualification.

- Fix and Flip Loans: Short-term bridge financing for renovation projects.

- Cash-Out Refinance: Extract equity for portfolio expansion.

- Bank Statement Loans: Perfect for entrepreneurs and self-employed borrowers.

- HELOC Loans: Access equity without disturbing your existing low-rate mortgage.

- Bridge Loans: Temporary financing to bridge the gap between transactions.

Whether you are looking to scale your portfolio in Alabama or refinance a commercial building in Illinois, having a clear understanding of these products is the first step toward successful real estate investing. Home Loans Network offers expertise across a wide range of states, including Arkansas, Michigan, and Indiana, ensuring that you have access to the right financing structure regardless of your location. We provide guidance through the complicated mortgage process so you can focus on finding the best deals in your local market.

Actionable Steps for Today’s Market

The volatility triggered by this morning's employment data does not have to stall your investment plans. Instead, it should encourage a more disciplined approach to your financial strategy. Reviewing your current pipeline and communicating with your lending partner can help you identify opportunities to lock in rates before further increases occur. If you are in the middle of a transaction in Chicago or other major metros across the 11 states we serve, now is the time to verify your numbers and ensure your deal still meets your cash flow requirements.

Compare your current options and access professional guidance today. Jumping in with a clear plan is the best way to protect your investments from sudden market shifts. We are committed to helping you compare options and guide you clearly through every stage of the financing process.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664