June 7 Mortgage News: How Today’s Interest Rate Volatility Impacts Your 2026 Buying Power

Navigating the mortgage market on June 7, 2026, requires a clear understanding of how small shifts in interest rates influence long-term financial outcomes.

Today’s data reflects a landscape defined by stability, yet the "choppy but contained" nature of rate movements continues to be a focal point for buyers and investors.

Whether you are looking to acquire a primary residence in Chicago or a short-term rental in Florida, staying informed on these fluctuations is essential for protecting your purchasing capacity.

This update provides a deep dive into current rate trends, regional market activity across several states, and strategies to maximize your real estate portfolio in the current economic climate.

Understanding the Mechanics of the 2026 Market

Before analyzing the daily shifts, it is important to define the core concepts currently driving the mortgage industry.

Volatility: The frequency and magnitude of price or interest rate movements over a specific period.

In practical terms, volatility dictates whether the rate you are quoted in the morning will still be available by the afternoon.

Buying Power: The total value of assets or property you can afford to purchase with a specific amount of money or credit.

High interest rates typically reduce your buying power because a larger portion of your monthly payment is dedicated to interest rather than the principal balance.

According to the latest mortgage rate forecasts from Norada Real Estate, rates are currently holding in the low-to-mid 6% range, creating a predictable yet competitive environment for active borrowers.

Regional Market Shifts Across the United States

The impact of rate volatility varies significantly depending on your geographic location and the specific property type you are targeting.

In markets like California and Florida, high demand for coastal properties remains resilient even as national rates experience minor daily "wiggles."

Midwestern hubs, including Chicago, Illinois, and various cities in Michigan and Indiana, are seeing a steady increase in inventory as the "lock-in effect" from previous years begins to soften.

Investors in Georgia and Virginia are focusing heavily on DSCR investor loans to acquire rental properties without the need for traditional income verification.

Meanwhile, states such as Alabama, Arkansas, Kentucky, and Missouri continue to offer some of the most accessible entry points for first-time homebuyers looking to maximize their initial investment.

Strategic Financing for Modern Homeowners and Investors

Choosing the right loan program is just as important as timing the market, as different solutions cater to different financial profiles.

DSCR (Debt Service Coverage Ratio) Loan: A mortgage specifically for real estate investors that uses the rental income of the property to qualify for the loan rather than the borrower’s personal income.

This is a primary tool for landlords looking to scale their portfolios quickly in states like California and Florida.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows homeowners to borrow against the equity they have built in their property.

Many homeowners in high-appreciation areas are currently using HELOCs to fund renovations or provide down payments for their next investment property.

Non-QM Mortgage Loans: Financing options that do not fit the strict criteria of government-backed loans, often used by self-employed borrowers or those with unique financial situations.

Explore our full range of loan programs to see which path aligns with your specific goals.

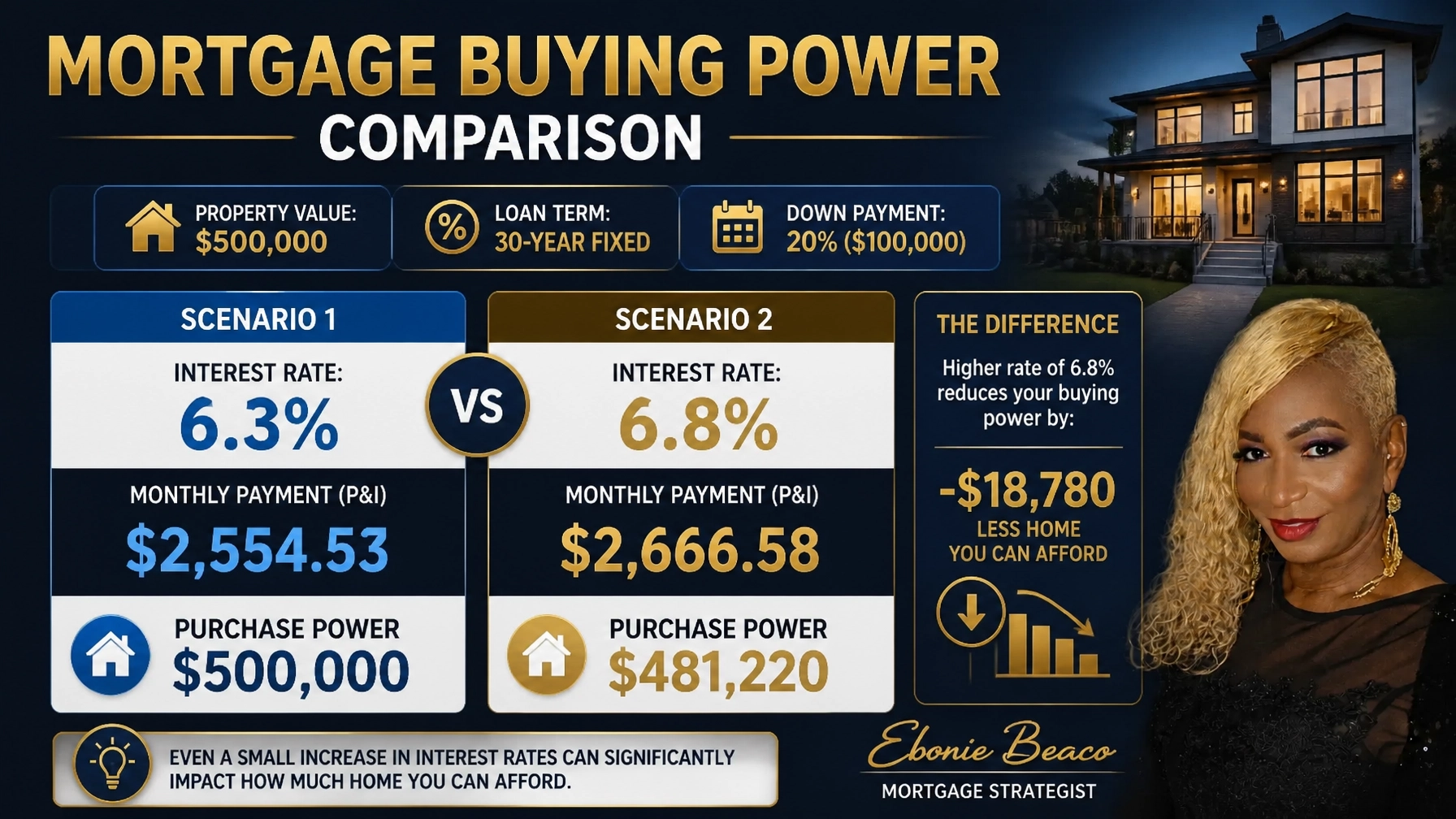

Practical Impact: The Buying Power Calculation

To illustrate how today’s rate volatility affects your bottom line, consider a common purchase scenario for a $500,000 property.

If you are looking at a 30-year fixed mortgage with a 20% down payment ($100,000), your loan amount would be $400,000.

At a rate of 6.3%, your monthly principal and interest payment would be approximately $2,476.

However, if daily volatility pushes that rate up to 6.8%, your monthly payment increases to $2,608.

This seemingly small 0.5% shift results in an additional $132 per month, which adds up to nearly $47,520 over the life of the 30-year loan.

Understanding these numbers helps you decide when to lock in a rate and how much house you can realistically afford in today’s market.

Scaling Your Portfolio with Multi-Unit and STR Financing

The 2026 market presents unique opportunities for those interested in multi-unit buildings and short-term rentals (STRs).

With Bankrate reporting steady rates in the mid-6% range, investors are finding that cash flow remains viable for well-located properties.

Short-term rental operators in vacation destinations across Florida and California are utilizing bridge loans to secure properties before transitioning into long-term DSCR financing.

Fix-and-flip investors in urban centers like Chicago are also finding value in renovation-focused loans to capitalize on the aging housing stock.

Whether you are a seasoned landlord or an aspiring investor, these strategies provide the flexibility needed to navigate current market conditions.

Jump in and compare your options to ensure you are utilizing the most efficient funding available for your next acquisition.

Guidance for Your Real Estate Journey

The complexity of the current mortgage landscape underscores the value of expert guidance and a clear strategy.

As market data continues to evolve, our commitment to transparency and education ensures that you have the tools to make confident decisions.

Whether you are researching home purchase options or looking to tap into your equity, we are here to support your goals across AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA.

Access the clarity you need to move forward with your real estate plans.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664