June 4 Mortgage Rate Trends Explained in Under 3 Minutes: What Buyers in FL, IL, and CA Need to Know

As we enter the first week of June 2026, the mortgage market continues to present a landscape of stability rather than volatility. National averages for a 30-year fixed-rate mortgage have settled into a predictable groove, hovering around the 6.5 percent mark. This consistency offers a unique window of opportunity for buyers and investors in active markets like Florida, Illinois, and California to plan their next moves with a degree of certainty. While the rapid fluctuations of previous years have largely subsided, understanding the underlying economic drivers is essential for anyone looking to navigate the current housing environment effectively. We are seeing a market that is finding its equilibrium, providing a clearer path for those ready to engage in real estate transactions.

The Macro Economic Landscape and National Averages

The broader economic picture for early June indicates that inflation data and labor market reports are the primary steering forces for interest rates. Most analysts agree that the Federal Reserve remains cautious, waiting for more definitive signs of cooling inflation before considering significant rate cuts. This has kept the 10-year Treasury yield, which is a major benchmark for mortgage pricing, anchored in the 4.3 to 4.4 percent range. Consequently, mortgage rates have followed suit, with daily movements remaining relatively minor as the market digests the latest economic signals. For homeowners and buyers, this means that the "wait and see" approach may not yield drastically different results in the immediate future.

To help you understand the technical side of these movements, let's look at some key industry terms and their practical application in today’s market:

- 10-Year Treasury Yield: This is the interest rate paid by the U.S. government on its ten-year debt obligations, which serves as a leading indicator for long-term mortgage rates.

- Practical Application: When the yield on the 10-year Treasury rises, lenders typically increase mortgage rates to maintain their profit margins.

- Conforming Loan: A mortgage that meets the dollar limits set by the Federal Housing Finance Agency (FHFA) and the funding criteria of Fannie Mae and Freddie Mac.

- Practical Application: These loans often offer lower interest rates than jumbo loans, making them a popular choice for buyers in standard price brackets.

- Basis Points (BPS): A unit of measure used in finance to describe the percentage change in the value of financial instruments, where one basis point equals 0.01 percent.

- Practical Application: Understanding basis points helps you compare small but significant differences in loan offers from various lenders.

- Lock-In Period: A specified window of time during which a lender guarantees a specific interest rate to a borrower.

- Practical Application: In a stable market, a 30-day or 60-day lock can protect you from any sudden, unexpected spikes in rates during your home-closing process.

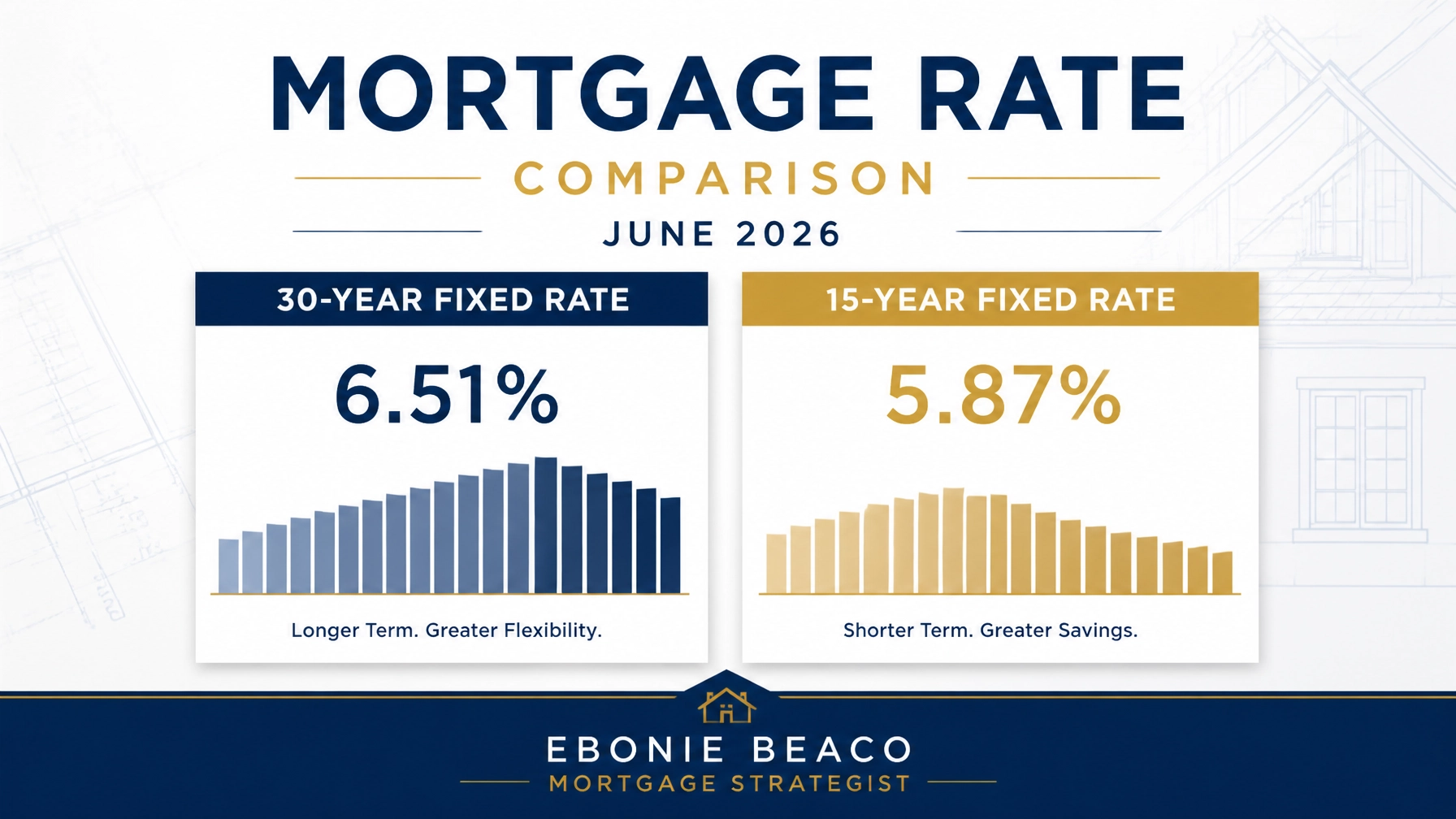

For those tracking the current figures, a recent Bankrate survey confirms that the 30-year fixed rate is currently averaging approximately 6.51 percent. Similarly, the 15-year fixed rate has remained competitive, sitting near 5.87 percent for well-qualified borrowers. These numbers suggest that while we are far from the historic lows of the past decade, the current rates are manageable for those with strong financial profiles and a clear investment strategy. Exploring various loan programs is the best way to determine which structure fits your specific goals.

Regional Deep Dive: Florida, Illinois, and California

In Florida, the real estate market is reacting to these stable rates with a steady flow of inventory in popular metropolitan areas like Miami, Orlando, and Tampa. Buyers are finding that while prices remain firm, the lack of dramatic rate hikes is allowing for more thoughtful negotiations. Florida investors are particularly active in the short-term rental space, often utilizing DSCR investor loans to expand their portfolios without relying on personal income verification. The state's continued growth and attractive climate keep demand high, even as rates remain in the mid-6 percent range.

The Illinois market, particularly in Chicago and its surrounding suburbs, shows a resilient trend where inventory remains the primary challenge for buyers. Many homeowners in Illinois are choosing to stay in their current properties rather than trading up, which keeps the supply of available homes relatively tight. However, those who are entering the market benefit from the predictability of June's rate trends, allowing them to calculate their monthly payments with confidence. For many Chicago residents, accessing home equity through a HELOC or cash-out refinance is becoming a preferred way to fund renovations or consolidate high-interest debt.

California continues to lead the nation in high-value transactions, where even small shifts in interest rates can have a significant impact on monthly affordability. In cities like Los Angeles and San Francisco, the stability of rates around 6.5 percent has helped buyers adjust their expectations and budgets accordingly. We are seeing an increase in the use of Non-QM mortgage solutions for self-employed professionals and entrepreneurs who require more flexible underwriting standards. Despite the higher price points, the demand for California real estate remains robust as buyers seek to build long-term wealth through property ownership.

Strategies for the Other Ten States

Beyond the three major states mentioned above, we are also monitoring housing activity in Alabama, Arkansas, Georgia, Indiana, Kentucky, Michigan, Missouri, and Virginia. Each of these regions offers unique opportunities, from the affordable suburban developments in Georgia and Virginia to the strong rental demand in the Midwestern hubs of Michigan and Missouri. Investors in these states are increasingly looking at fix and flip financing to modernize older housing stock and meet the needs of modern tenants. The consistency of mortgage rates across the board allows for more accurate pro-forma projections when evaluating these investment deals.

In markets like Alabama and Arkansas, the lower cost of entry combined with stable financing makes these states ideal for first-time homebuyers and new investors. The current rate environment encourages a focus on long-term cash flow rather than short-term appreciation. By understanding the mortgage basics, residents in these states can position themselves to take advantage of the current stability. Regardless of your location, the goal is to align your financing with your personal financial timeline and wealth-building objectives.

Financial Strategy: The Power of Home Equity

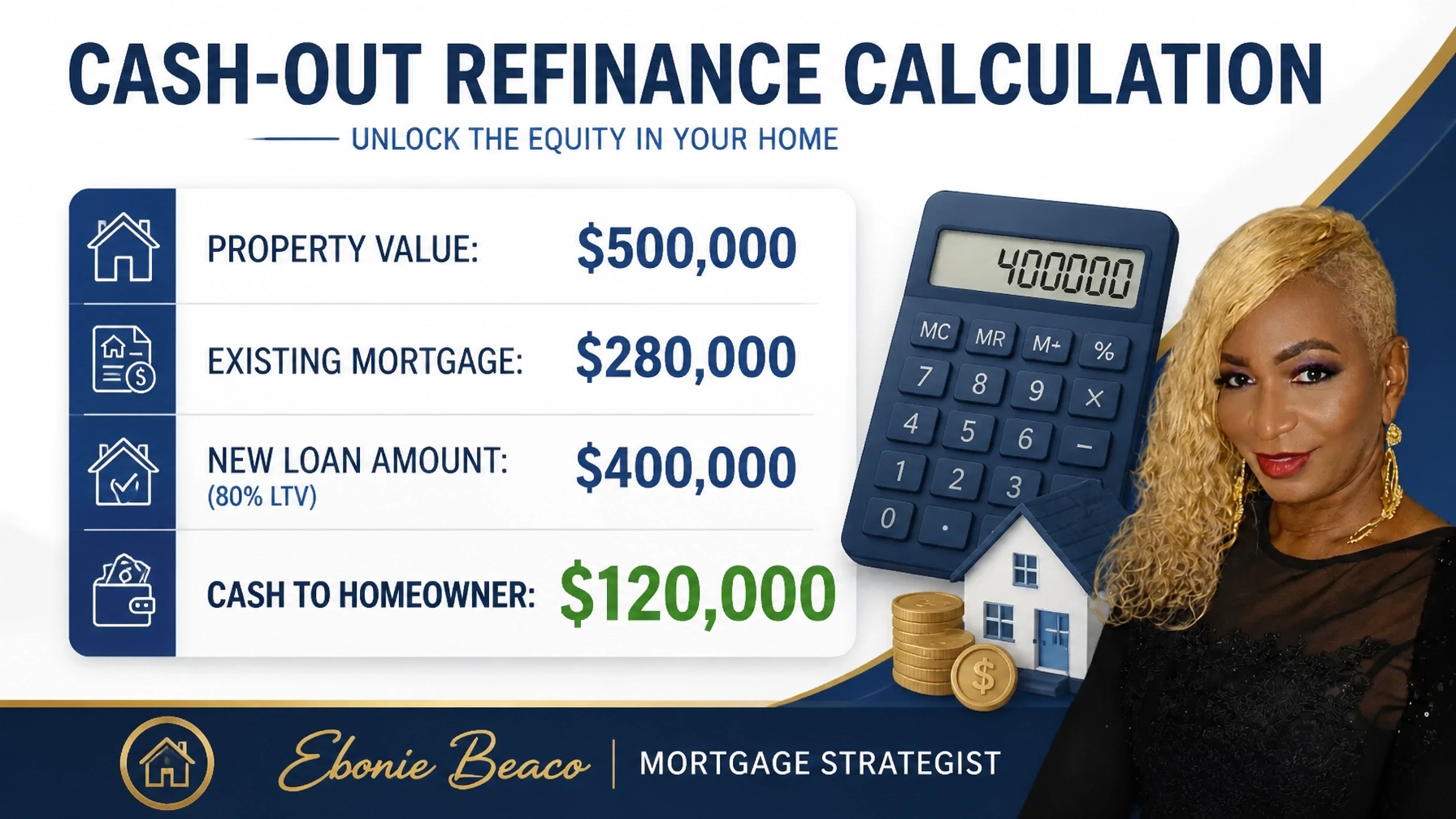

One of the most effective ways to navigate a mid-6 percent rate environment is to leverage the equity you have already built in your property. Many homeowners who purchased their homes several years ago have seen significant appreciation, providing them with a substantial pool of capital. Whether you are looking to renovate your primary residence, purchase an investment property, or consolidate debt, a cash-out refinance or a Home Equity Line of Credit (HELOC) can provide the necessary funds. Let's look at a practical example of how a homeowner might utilize this strategy in today's market.

Consider a homeowner with a property valued at $500,000 and an existing mortgage balance of $280,000. By choosing a cash-out refinance at an 80 percent loan-to-value (LTV) ratio, the homeowner could potentially secure a new loan of $400,000. After paying off the original mortgage, the homeowner would receive $120,000 in cash, which could be used for various investment purposes. This strategy allows the homeowner to turn their "dormant" equity into an "active" tool for wealth creation.

| Metric | Value |

|---|---|

| Current Property Value | $500,000 |

| Existing Mortgage Balance | $280,000 |

| Max Loan-to-Value (80%) | $400,000 |

| Available Cash to Homeowner | $120,000 |

This type of calculation is essential for understanding the true potential of your real estate portfolio. While the interest rate on the new loan might be higher than the original rate from years ago, the ability to access $120,000 can often lead to greater returns through strategic reinvestment. Many investors use these funds to provide down payments on new rental properties or to execute the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy. You can find more details on these strategies by visiting our home refinance section.

Looking Ahead: The Forecast for Late 2026

As we look toward the second half of the year, major institutions like Fannie Mae and the Mortgage Bankers Association (MBA) anticipate a gradual decline in rates. The consensus forecast suggests that we may see the 30-year fixed-rate average drift toward the 6.0 percent mark by the end of 2026. While a return to the 3 percent range is not expected in the near term, this slow and steady improvement in affordability is a positive sign for the housing market. It allows for a more sustainable growth trajectory and helps to prevent the boom-and-bust cycles that can occur when rates move too rapidly.

If you are currently on the fence about buying or refinancing, it is important to remember that you are not just choosing a rate, you are choosing a strategy. The "right" time to move is when the numbers align with your specific financial needs and long-term vision. We are here to help you compare your options and guide you clearly and confidently through the complexities of the current mortgage market. Whether you are a first-time buyer or a seasoned investor, our commitment is to provide the education and transparency you need to succeed.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664