June 3rd Mortgage Secrets Revealed: What the Big Banks Aren’t Telling Virginia and Michigan Investors

As we cross the threshold of June 3rd, 2026, the mortgage market continues to present a complex landscape for property owners and real estate professionals. National 30-year fixed rates are currently averaging approximately 6.53%, a figure that has remained relatively stable but slightly elevated compared to the early spring dip. For investors in Virginia and Michigan, this "higher for longer" environment has created a unique set of challenges that traditional retail banks are often ill-equipped to handle. While the big banks are focused on rigid debt-to-income (DTI) ratios and tax return stability, a more strategic approach is required to unlock capital in today’s housing economy. You need to look beyond the standard primary residence products to find the leverage that actually moves the needle for a growing portfolio.

The gap between what a traditional bank offers and what a dedicated mortgage strategist can provide has never been wider. Big banks typically prioritize low-risk, high-volume W-2 earners, often turning away seasoned investors or self-employed entrepreneurs who do not fit their narrow underwriting boxes. This systemic "no" is often delivered without explaining that alternative financing paths exist right under your nose. In Virginia and Michigan, where housing demand remains resilient despite the rate environment, these missed opportunities can cost thousands in lost potential equity. Understanding the nuances of non-QM (Qualified Mortgage) lending is the first step toward reclaiming your financial momentum.

The Big Bank Barrier vs. The Strategic Advantage

Traditional financial institutions are currently operating under strict capital requirements that limit their flexibility for investment properties and non-traditional income earners. When you walk into a major retail bank branch, the loan officer is generally restricted to a handful of standard government-backed programs that require exhaustive documentation of your personal income. This approach often ignores the actual profitability of the real estate asset itself, which is a major hurdle for investors trying to scale. If your tax returns show significant write-offs, as many successful entrepreneurs and landlords do, the big bank will likely calculate a DTI that disqualifies you immediately. Compare this to a strategic mortgage approach where we prioritize the asset's performance and your actual cash flow over traditional paper losses.

DSCR Loans: The Investor’s Secret Weapon in Virginia

For those looking to expand their footprint in markets like Richmond, Virginia Beach, or the Northern Virginia corridor, the Debt Service Coverage Ratio (DSCR) loan is a game-changer. A DSCR loan is a type of investor-focused mortgage where the qualification is based entirely on the rental income generated by the property rather than your personal employment history. This allows you to close deals without submitting tax returns, W-2s, or pay stubs, which significantly streamlines the acquisition process. As long as the property's gross rent covers the monthly mortgage, taxes, insurance, and HOA fees (the "debt service"), the loan can move forward. Explore our various loan programs to see how this fits your specific investment goals.

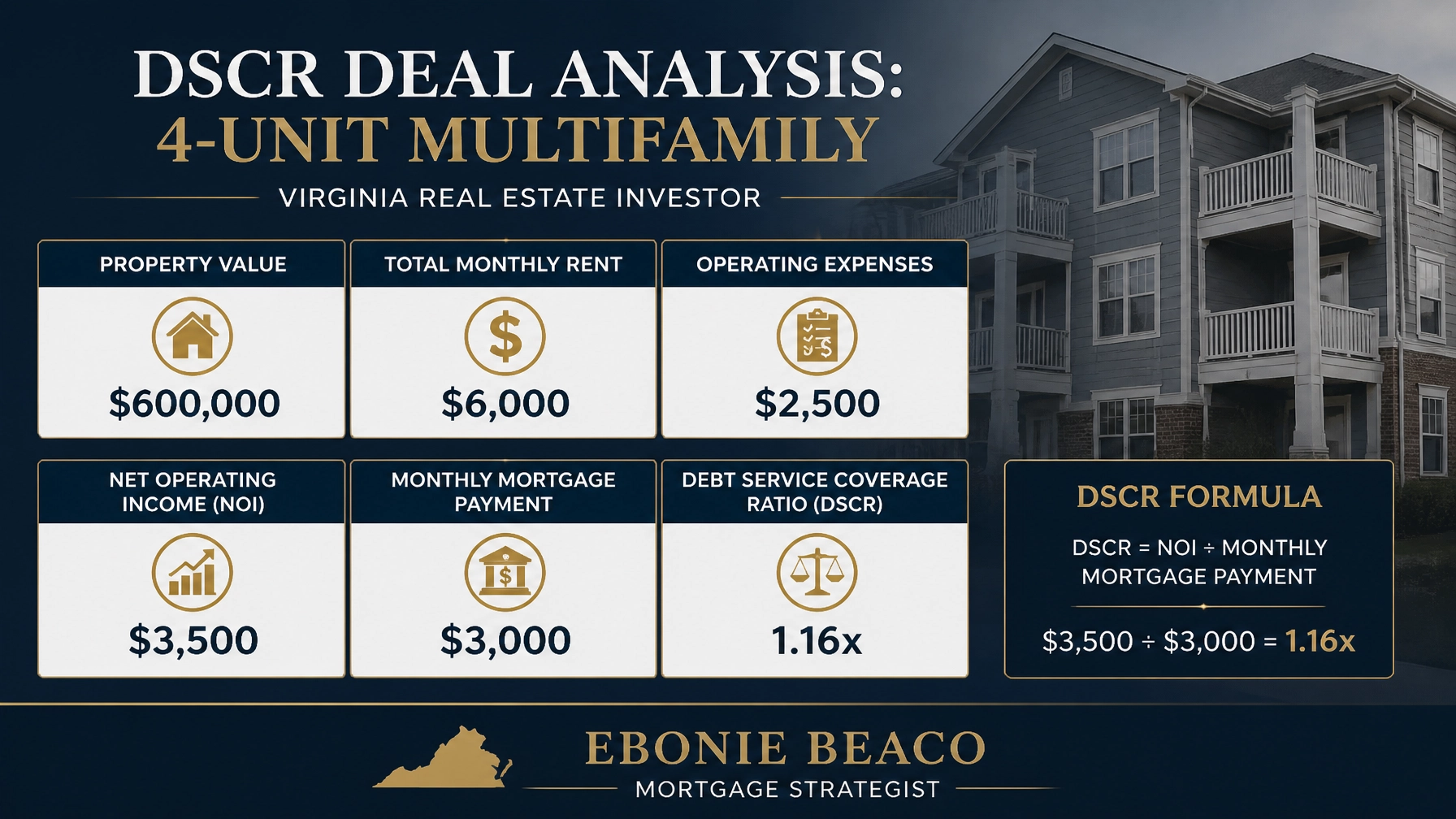

Consider a real-world scenario for a Virginia investor purchasing a four-unit multifamily building in a high-demand area. With a purchase price of $600,000 and a total monthly rental income of $6,000, the property demonstrates strong cash flow potential. After accounting for $2,500 in monthly operating expenses, the property nets $3,500 in income (NOI). With a projected mortgage payment of $3,000, the DSCR lands at 1.16x, which meets the standard threshold for many specialized investor programs. This calculation allows the investor to bypass the personal income scrutiny that a big bank would require, focusing purely on the property's ability to pay for itself.

Unlocking Equity in the Michigan Market

In Michigan, particularly in growing hubs like Grand Rapids and Detroit, many homeowners are sitting on a record amount of "trapped" equity. Traditional banks often push standard home equity lines of credit (HELOCs) that come with variable rates and strict usage requirements. However, a strategic cash-out refinance can often provide more stability and a larger lump sum for those looking to fund a renovation or a new investment property. Accessing this capital allows you to pivot quickly when a deal presents itself, rather than waiting for a bank's lengthy second-mortgage approval process. By restructuring your existing debt, you can often lower your total blended interest rate while freeing up six figures in liquid capital.

Let’s look at a homeowner in Grand Rapids with a property currently valued at $400,000 and an existing mortgage balance of $200,000. Under current guidelines, a cash-out refinance at an 80% loan-to-value (LTV) ratio would allow the owner to take out a new loan of $320,000. After paying off the original $200,000 mortgage, the homeowner is left with $120,000 in available funds to deploy into a new rental property or a major renovation project. This strategy transforms a stagnant asset into a primary driver of wealth, bypassing the restrictive "equity hoarding" advice often given by traditional retail lenders. You can run your own numbers using our mortgage calculators to see how much equity you might be able to tap.

Bank Statement Loans for the Michigan Entrepreneur

The self-employed workforce in Michigan is a major part of the local economy, yet these individuals are frequently penalized by big banks for having complex tax structures. Bank statement loans are designed specifically for these entrepreneurs, allowing them to qualify based on their actual business or personal bank deposits over the last 12 to 24 months. Instead of looking at the bottom-line taxable income, which is often reduced by legitimate business expenses, we look at the gross revenue coming into your accounts. This approach provides a much more accurate picture of your ability to repay a loan while respecting the tax-efficient way you run your business.

Jump in and compare how this works: A business owner might show $300,000 in annual deposits but only $40,000 in taxable income after all deductions are finalized. A big bank would likely reject this borrower, citing insufficient income for a $400,000 home purchase. Under a bank statement program, we can use a percentage of those $300,000 in deposits as qualifying income, often leading to a swift approval. This method is perfect for 1099 contractors, freelancers, and small business owners who are tired of being told "no" by the traditional system despite their healthy cash flow.

Staying Ahead of the June 2026 Shift

As we look toward the second half of 2026, the key to success in Virginia and Michigan is flexibility and speed. According to data from Freddie Mac, while rates may fluctuate, the fundamental demand for housing in these states remains high due to limited inventory. Big banks are often the slowest to react to market shifts, leaving you stuck in a queue while a better-prepared investor snaps up your target property. By working with a mortgage strategist who has access to over 240 different lenders, you gain a competitive edge that the average retail buyer simply does not have. You can access specialized programs like fix-and-flip financing, bridge loans, and ITIN mortgages that are rarely discussed in a bank branch.

The real "secret" isn't that there is no money available: it's that the money is flowing through channels the big banks don't want you to know about. Whether you are a first-time homebuyer in Virginia or a seasoned landlord in Michigan, your financing should be as unique as your financial profile. Stop trying to fit your complex financial life into a simple bank application. Instead, align your financing with your long-term goals by exploring solutions that prioritize your future wealth over your past tax returns. Access the guidance you need to navigate this market with confidence and clarity.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664