June 2nd Mortgage Update: Why Today’s Rate Movement Will Change the Way You Invest in Florida and California

As we enter the first week of June 2026, the mortgage landscape is presenting a unique set of challenges and opportunities for those monitoring the housing markets in Florida and California. For the past several months, interest rates have hovered in a tight range, forcing investors to look beyond the headline numbers and focus on specialized financing vehicles. Today’s update is designed to help you navigate these shifts with the precision of an experienced strategist. By understanding the current interplay between national inflation data and local inventory levels, you can position your real estate portfolio for long-term growth regardless of the noise in the daily news cycle.

The national mortgage rate environment remains the primary driver of homebuyer sentiment and investor activity across the country. As of June 2nd, 30-year fixed-rate mortgages are averaging approximately 6.87%, a slight cooling from the peaks we saw in previous quarters. This stabilization suggests that the initial shock of higher debt costs has finally been absorbed by the market, shifting the focus from "when will rates drop" to "how do I make the math work now." According to the Freddie Mac Primary Mortgage Market Survey, consistent rate plateaus often precede a shift in seller behavior, which we are beginning to see in several key metropolitan areas.

Understanding the National Landscape and Economic Drivers

The current rate trajectory is largely a response to recent consumer price index reports and the Federal Reserve’s commitment to maintaining a restrictive monetary policy until inflation targets are firmly met. For homeowners and investors in states like Alabama, Arkansas, and Virginia, this means that the "wait and see" approach is becoming increasingly expensive in terms of lost opportunity and rising property values. While the cost of capital is higher than the historic lows of the early 2020s, it is important to remember that real estate remains a hedge against inflation. Successful participants in today’s market are those who utilize innovative loan structures to offset these baseline interest rates.

When analyzing today’s movement, you must look at the spread between the 10-year Treasury yield and current mortgage offerings. Typically, this spread tightens as market volatility decreases, which could lead to better pricing on specialized products like Non-QM loans or bank statement programs for the self-employed. Even if the headline 30-year rate remains elevated, these niche products are becoming more competitive as lenders vie for the business of sophisticated borrowers. We encourage all our clients to explore our full range of available loan programs to find the specific solution that fits their unique financial profile and property type.

The California Strategy: Unlocking Equity and Driving Density

California’s real estate market continues to be defined by high entry prices and significant equity growth for existing homeowners. In cities like Los Angeles, San Diego, and San Jose, the strategy for 2026 has shifted heavily toward "density as an investment." This often involves the construction of Accessory Dwelling Units (ADUs) or the conversion of existing structures to maximize rental income on a single lot. Financing these projects requires a sophisticated understanding of how to tap into current equity without losing a low-interest primary mortgage, which is where a HELOC (Home Equity Line of Credit) often becomes the superior tool.

For many California residents, a cash-out refinance is a viable path if the existing rate on the primary mortgage is already close to current market levels. By extracting equity, you can fund the construction of a backyard cottage that significantly increases the total cash flow of the property. This "forced equity" play is one of the most reliable ways to achieve a high return on investment in a high-cost environment. We are seeing a surge in investors using California equity to fund acquisitions in lower-cost states like Georgia and Indiana, effectively diversifying their portfolios while keeping their primary residence intact.

Navigating the Florida Market: DSCR and The Buyer’s Pivot

In Florida, the narrative for June 2nd is centered on a transition toward a buyer’s market in several key regions. Inventory levels in metros such as Tampa, Orlando, and parts of Southwest Florida have risen, giving investors more leverage during negotiations. However, the rise in property insurance premiums and taxes has made traditional financing more difficult for some. This is where DSCR (Debt Service Coverage Ratio) loans become essential, as they allow investors to qualify based on the rental income of the property rather than their personal income or tax returns.

DSCR Investor Loans: A mortgage product where qualification is based on the property’s ability to generate enough rental income to cover the monthly debt service.

Application: In the current Florida market, using a DSCR loan allows an investor to bypass the rigorous DTI (Debt-To-Income) checks required for conventional loans, making it easier to scale a portfolio of short-term or long-term rentals.

The example above illustrates the power of the DSCR approach. If you are purchasing a property in Florida for $500,000 with a rental income of $4,500 and a total mortgage payment (including taxes and insurance) of $3,200, your DSCR ratio would be 1.40. Most lenders look for a ratio above 1.20, meaning this property would easily qualify for financing even if the investor has a complex personal tax situation. Exploring these options through our mortgage calculators can help you determine the feasibility of a deal before you even step foot on the property.

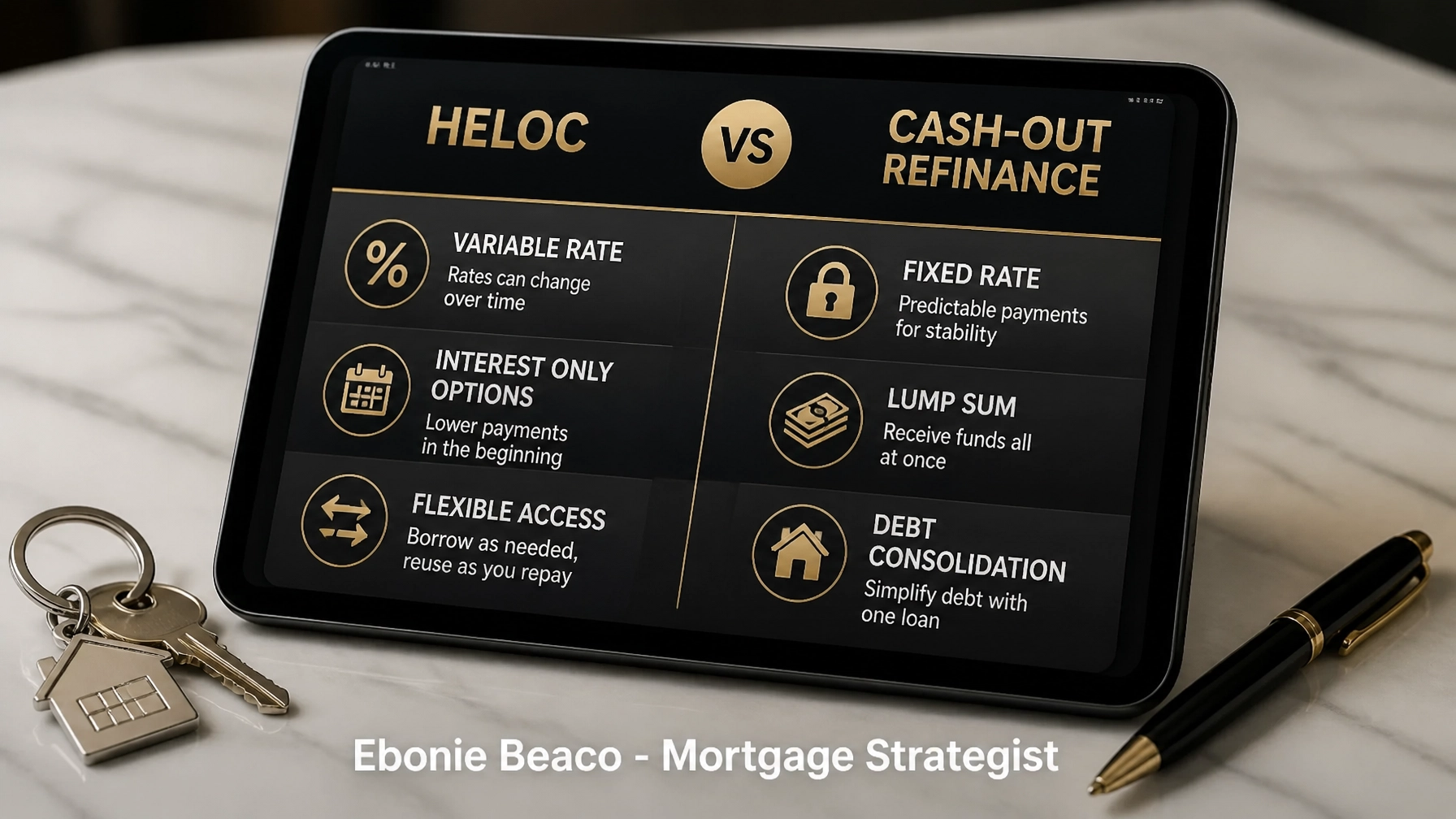

Financial Comparison: HELOC vs. Cash-Out Refinance

Choosing between a HELOC and a cash-out refinance is one of the most critical decisions a homeowner or investor will make this year. A HELOC functions similarly to a credit card secured by your home; you only pay interest on the amount you actually draw, and the rates are typically variable. This is often the preferred choice for those who have a very low interest rate on their first mortgage and only need funds for short-term projects or as an emergency reserve. It offers flexibility without resetting the terms of your primary financing.

On the other hand, a cash-out refinance replaces your existing mortgage with a new, larger loan, and you receive the difference in cash. This is a "lump sum" strategy that provides a fixed interest rate, which is advantageous for long-term debt consolidation or major renovations where you want the security of a predictable monthly payment. In the current June 2nd environment, if your existing rate is above 5.5%, the gap between your current rate and today’s market rate may be small enough that a total refinance is more cost-effective than adding a second lien with a higher variable rate.

| Feature | HELOC (Home Equity Line of Credit) | Cash-Out Refinance |

|---|---|---|

| Loan Structure | Second mortgage / Line of credit | New first mortgage |

| Interest Rate | Usually variable | Fixed or adjustable |

| Payment Options | Often interest-only for a set period | Principal and interest |

| Best For | Ongoing costs, ADUs, emergency funds | Large one-time purchases, debt consolidation |

| Impact on 1st Loan | None; stays in place | Replaces 1st loan entirely |

Regional Spotlight: Chicago and the Midwest Resilience

While coastal markets often grab the headlines, the stability of the Midwest market is attracting significant attention this June. Chicago, in particular, remains a stronghold for investors seeking cash flow rather than pure appreciation. The diversity of neighborhoods and the robust demand for rental housing make it a prime location for fix-and-flip financing and landlord loans. Unlike the volatile price swings seen in some Sunbelt metros, Chicago’s market tends to move more predictably, providing a layer of safety for those with a lower risk tolerance.

In states like Michigan and Indiana, we are seeing a high demand for Non-QM mortgage loans for self-employed professionals who are purchasing their first or second investment properties. The ability to use bank statements to prove income is a game-changer for entrepreneurs who may have significant business expenses that reduce their net income on paper. As your mortgage strategist, I can help you look at the specific nuances of the Chicago market or the suburbs of Indianapolis to ensure your financing is structured to maximize your local competitive advantage.

Building Your Real Estate Wealth in 2026

The complexity of the current market requires more than just a loan officer; it requires a strategist who understands the long-term implications of every financial move. Whether you are navigating the high-stakes environment of California, the evolving buyer’s market in Florida, or the steady cash-flow opportunities in the Midwest, your success depends on access to the right information and the right tools. We are committed to providing the clarity and guidance you need to make confident decisions in an ever-changing economy.

The movement we see today is not a signal to retreat, but a call to refine your approach. By utilizing the diversity of products available at Home Loans Network, from bridge loans for quick acquisitions to construction loans for ground-up development, you can overcome the limitations of traditional lending. We invite you to dive deeper into our resources and begin planning your next move with a clear understanding of the risks and rewards present in today's housing market.

Explore your financing potential and secure your future in real estate.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664