June 2026 Rate Shifts: How Today’s Economic Data Impacts Your Florida Jumbo Loan

As we enter the second day of June 2026, the mortgage market is reacting swiftly to fresh economic indicators that directly influence high balance financing. For homeowners and investors navigating the luxury real estate sectors in Florida, California, and Virginia, understanding these daily shifts is essential for timing a purchase or a strategic refinance. Jumbo loans, which currently cover financing amounts exceeding $832,750 in most regions, operate on a different set of market mechanics compared to standard conforming loans. Today’s data suggests a landscape of stabilization, yet subtle volatility remains as the market interprets the latest labor and inflation reports.

Navigating the complexities of high value property financing requires a clear view of how national economic policy filters down to local markets like Miami, Tampa, and Orlando. Whether you are looking to acquire a primary residence or expand a rental portfolio, the cost of capital is the primary variable in your long term strategy. We are seeing a mid-year environment where lender competition remains high, but pricing is sensitive to every basis point move in the bond market. This guide breaks down the current data and explains how you can position yourself to take advantage of current market opportunities.

Defining Key Financial Terms

- Jumbo Loan: A mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency. In 2026, this typically applies to any loan amount above $832,750, requiring more stringent credit and reserve requirements for the borrower.

- Consumer Price Index (CPI): A measure that examines the weighted average of prices of a basket of consumer goods and services. Investors watch this closely because rising inflation usually leads to higher mortgage rates to offset the eroding value of future payments.

- Debt-to-Income Ratio (DTI): The percentage of your gross monthly income that goes toward paying debts. For jumbo financing, lenders often look for a DTI below 43 percent to ensure you have the financial capacity to manage a larger monthly obligation.

- 10-Year Treasury Yield: The interest rate the U.S. government pays on its debt with a ten-year maturity. Mortgage rates often track this yield closely, meaning when treasury yields rise, your potential mortgage rate usually follows.

- Loan-to-Value (LTV): The ratio of a loan to the value of an asset purchased. High value properties often require a lower LTV, frequently between 70 percent and 80 percent, to secure the most competitive interest rates.

The Economics of June 2026: Jobs, Inflation, and the Fed

Today’s economic reports provide a mixed signal for the housing market, as job growth remains resilient while inflationary pressures show signs of a slow cooling trend. For the jumbo market in Florida and Georgia, this means that while rates have pulled back from their recent peaks, they remain in a narrow band around the 6.5 percent mark. The Federal Reserve has maintained its policy rate near 3.50 percent, signaling that they are in a wait and see mode before considering further adjustments. This higher for longer stance by the central bank keeps the 10 year Treasury yield elevated, which serves as the primary benchmark for pricing long term fixed rate jumbo mortgages.

When employment data comes in stronger than expected, it often creates upward pressure on rates because a robust economy can sometimes reignite inflation. Conversely, the cooling inflation data we are seeing this week provides some relief for borrowers who have been waiting for a window of opportunity to lock in a lower rate. In states like Michigan, Indiana, and Illinois, where the housing market is currently seeing a surge in activity, these daily fluctuations can mean the difference of thousands of dollars in total interest over the life of the loan. According to recent reports from Fortune and Bankrate, the stability in the bond market is a welcome sign for those looking to close deals before the mid-summer heat.

Understanding the Jumbo Loan Spread

Jumbo loans are not backed by government sponsored entities like Fannie Mae or Freddie Mac, which means they are held on bank balance sheets or sold to private investors. This lack of government backing often results in a "spread" or a difference in the interest rate compared to conforming loans. In the current June 2026 market, jumbo rates are hovering approximately 0.1 to 0.2 percentage points higher than standard 30 year fixed mortgages. This relationship can shift based on how much cash banks have on hand and how hungry private investors are for high quality mortgage debt.

For a borrower in Florida, this means your credit profile and the amount of equity you put into the deal are more influential than ever. Lenders are currently prioritizing high net worth individuals who can demonstrate significant liquidity and a pristine repayment history. If you are exploring options for a Jumbo Loan, you should be prepared to provide detailed documentation of your assets and income sources. Because these loans are manually underwritten, there is often more room for a mortgage strategist to structure a deal that fits your specific financial profile, especially if you are self-employed or have a complex income stream.

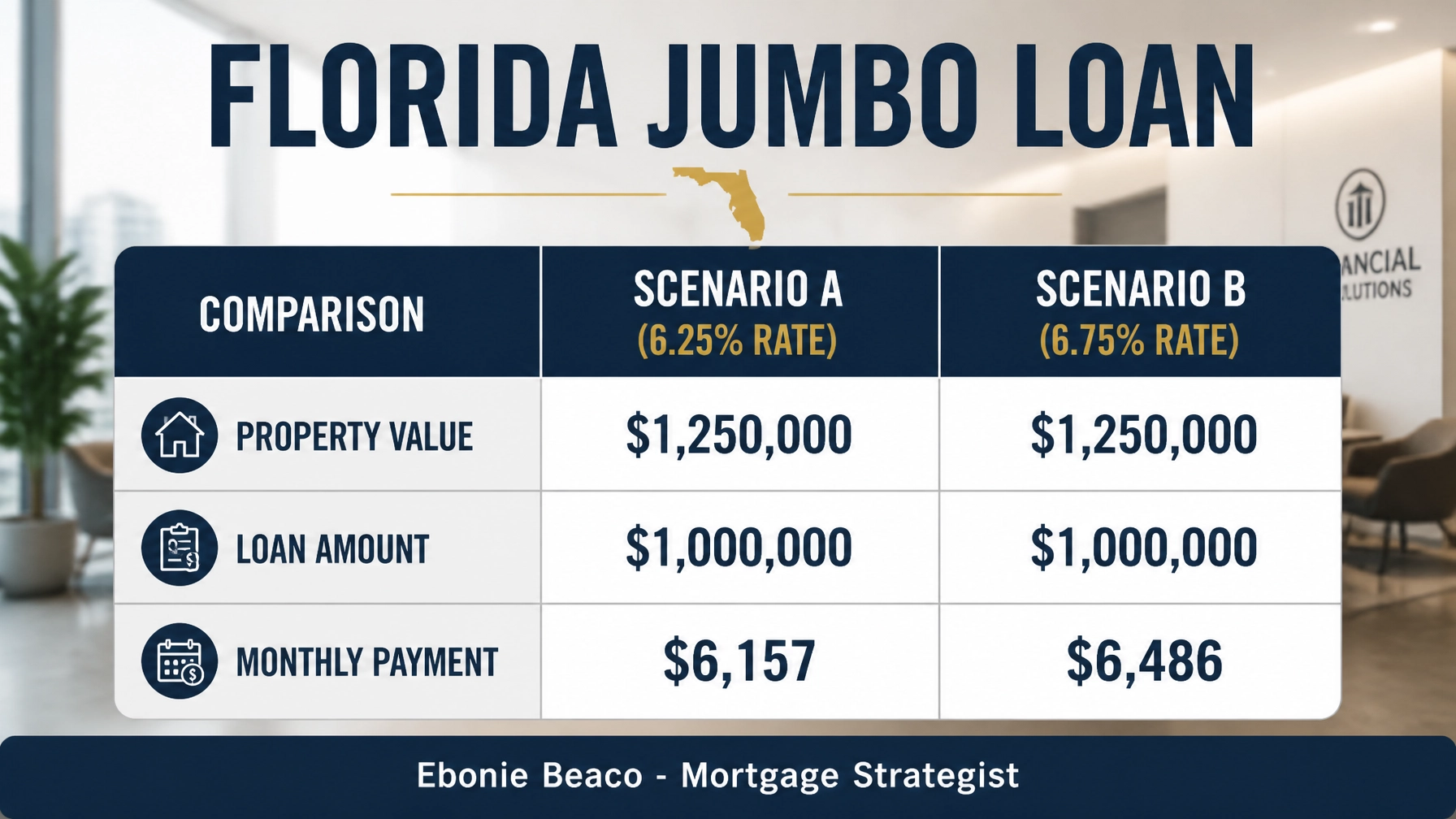

Analyzing the Numbers: A Florida Jumbo Comparison

To see how these daily rate shifts impact your actual budget, let us look at a practical scenario for a luxury purchase in a market like Naples or Boca Raton. Imagine you are purchasing a home for $1,250,000 and planning to put 20 percent down, leaving a loan balance of $1,000,000. Even a small shift in the daily rate can significantly alter your monthly overhead and your long term wealth building potential.

In the example above, a move from 6.75 percent down to 6.25 percent represents a monthly savings of $329. Over a five year period, that equates to nearly $20,000 in saved interest that could be redirected into other investments or used to pay down the principal balance faster. This is why staying informed about daily economic data is critical; locking your rate on the right day can have a massive impact on your bottom line. We frequently work with clients to monitor these trends and identify the optimal moment to secure their financing.

Market Activity Across the Sunbelt and Beyond

While Florida remains a primary focus for many luxury buyers, we are seeing similar financing trends across our other service areas, including Alabama, Arkansas, and California. The demand for high quality real estate continues to be driven by individuals looking to relocate to tax friendly states or areas with high lifestyle appeal. In California, where jumbo loans are the norm rather than the exception, borrowers are increasingly looking toward Cash-Out Refinance strategies to tap into existing equity for secondary property purchases or business expansion.

In the Southeast, specifically Georgia and Virginia, the market is seeing a rise in "creative jumbo" scenarios. This includes using asset depletion models or bank statement programs for entrepreneurs who have high cash flow but may not show a high taxable income on their tax returns. Our goal is to bridge the gap between complex financial profiles and the strict requirements of jumbo lenders. By leveraging our network of over 240 lenders, we can often find a solution that traditional big box banks might overlook.

Strategies for Investors: Tapping into Home Equity

Real estate investors are currently utilizing several strategies to grow their portfolios in this 2026 environment. One of the most popular methods is the use of a HELOC (Home Equity Line of Credit) to access the "dead equity" in their primary residence. This capital can then be used as a down payment for a DSCR Investor Loan on a luxury rental property. In Florida’s high demand short term rental markets, a jumbo DSCR loan allows an investor to qualify based on the property's projected income rather than their personal salary.

For those looking to scale quickly, the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy remains a staple. By using short term Fix and Flip Loans to acquire and renovate a property, you can then transition into a long term jumbo loan once the property is stabilized and its value has increased. This allows you to pull your initial capital back out to fund the next deal. Understanding the daily rate trends is vital for the "refinance" portion of this strategy, as it determines your long term cash flow and ROI.

Florida Specific Considerations: Insurance and Valuation

When you are financing a high value home in Florida, the interest rate is only one piece of the puzzle. The state's unique insurance landscape and climate considerations play a significant role in the underwriting process. Lenders will look closely at your wind and flood insurance coverage, as well as the age of the home’s roof and mechanical systems. These costs are factored into your total monthly payment and can affect your qualifying debt to income ratio.

Furthermore, luxury appraisals in Florida can be complex due to the unique features of waterfront properties and high end finishes. A high quality appraisal is necessary to support a jumbo loan, especially in a market where valuations have seen steady appreciation. Working with a strategist who understands these local nuances ensures that your loan process remains smooth from application to closing. Whether you are in a bustling metro area or a quiet coastal town, the combination of national economic data and local market conditions will dictate your best path forward.

Monitoring the Market for Success

As we move further into June 2026, the key to success in the jumbo market is proactive monitoring and readiness. Economic data will continue to shift, and the window for the most competitive rates may only open briefly. By maintaining a clear understanding of your financial profile and the current market drivers, you can act with confidence when the right opportunity arises. We are committed to providing the education and guidance you need to navigate these decisions and align your financing with your wealth building goals.

If you are currently evaluating your options for a high value purchase or looking to restructure your existing debt, now is the time to start the conversation. The market waits for no one, and having a plan in place is the best way to ensure you are not leaving money on the table. Explore our resources or jump in with a specific question about your scenario to see how we can help you achieve your real estate objectives.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664