June 2026 Rate Forecast: Why This Week’s Economic Data Could Change Your Closing Date

As we enter the first week of June 2026, the mortgage market finds itself at a significant crossroads. Homeowners, real estate investors, and prospective buyers across states like Illinois, Florida, and California are closely monitoring the economic calendar. The transition from May to June often brings a seasonal surge in housing activity, yet this year, the focus remains squarely on the Federal Reserve and the incoming labor data. With mortgage rates hovering in the mid-6% range, even minor shifts in federal policy or consumer sentiment can ripple through the closing process for thousands of transactions.

Understanding the Mid-Year Economic Shift

The mortgage landscape in 2026 has been defined by a "higher-for-longer" environment that continues to test the patience of market participants. While inflation has cooled significantly from the peaks seen in previous years, the path toward a lower rate environment remains uneven. This week is particularly critical because it marks the release of the June employment report, a data point that traditionally serves as a bellwether for bond market activity. When job growth exceeds expectations, it often signals to the Fed that the economy is still running warm, which can prevent the downward movement of interest rates.

Explore the latest trends to understand how these global factors influence your local market. Whether you are looking at a condo in downtown Chicago or a multi-family unit in Atlanta, the cost of financing is the primary variable in your return on investment. Professionals in the industry are advising clients to stay vigilant as the bond market reacts to these early-month updates. Jump in and review your lock-in options before the volatility of the week takes hold.

Dictionary of Key Terms

Basis Point (BPS): A unit of measure used in finance to describe the percentage change in the value or rate of a financial instrument.

Practical Application: A 25-basis point shift in mortgage rates can result in thousands of dollars in interest savings over the life of a loan.

Non-Farm Payrolls (NFP): A monthly report released by the Bureau of Labor Statistics that measures the number of workers in the U.S., excluding farm workers, private household employees, and non-profit organization employees.

Practical Application: A strong NFP report can cause mortgage rates to rise as investors anticipate continued economic strength.

Debt-to-Income Ratio (DTI): A personal financial measure that compares an individual’s monthly debt payment to their monthly gross income.

Practical Application: Higher interest rates can push your DTI over the limit, potentially disqualifying you from certain loan programs if your closing is delayed.

Why This Week’s Jobs Report Is Critical

The labor market is the engine of the American economy, and its performance directly dictates the direction of the 10-year Treasury yield. Historically, mortgage rates track the movement of the 10-year Treasury, making the June 5th employment report a pivotal event for anyone with a pending contract. If the report shows that hiring is slowing, we may see a modest dip in rates as investors pivot toward bonds. Conversely, a "hot" jobs report could send yields higher, forcing lenders to adjust their pricing upward before the weekend.

Investors should note that the labor market's strength affects more than just residential purchase loans. It also impacts the pricing for commercial real estate and landlord loans, where risk premiums are often tied to broader economic stability. For those managing Airbnb or short-term rental portfolios in vacation markets like Florida or the Virginia coast, these shifts can alter the feasibility of a cash-out refinance. Accessing your home equity requires timing the market correctly to ensure your monthly debt service remains manageable.

Regional Market Highlights: From Chicago to Miami

The impact of shifting rates is felt differently across various metropolitan areas. In Chicago, where the housing market has shown resilient demand despite pricing pressures, a sudden rate hike can cause a "cooling effect" on pending sales. Realtors in Georgia and Alabama are seeing a similar trend, where buyers are increasingly sensitive to monthly payment fluctuations. In high-cost areas like California, even a 0.125% increase in interest can remove a significant number of buyers from the qualification pool for jumbo loans.

Compare the activity in these markets to your own local neighborhood to find the best opportunities. While national averages provide a baseline, regional inventory levels and local economic drivers also play a role in your closing timeline. If a lender sees a spike in volatility, they may slow down the underwriting process to ensure all risk parameters are met. This is why having a proactive mortgage strategist is essential during weeks with high-impact economic releases.

The Financial Impact of Rate Shifts

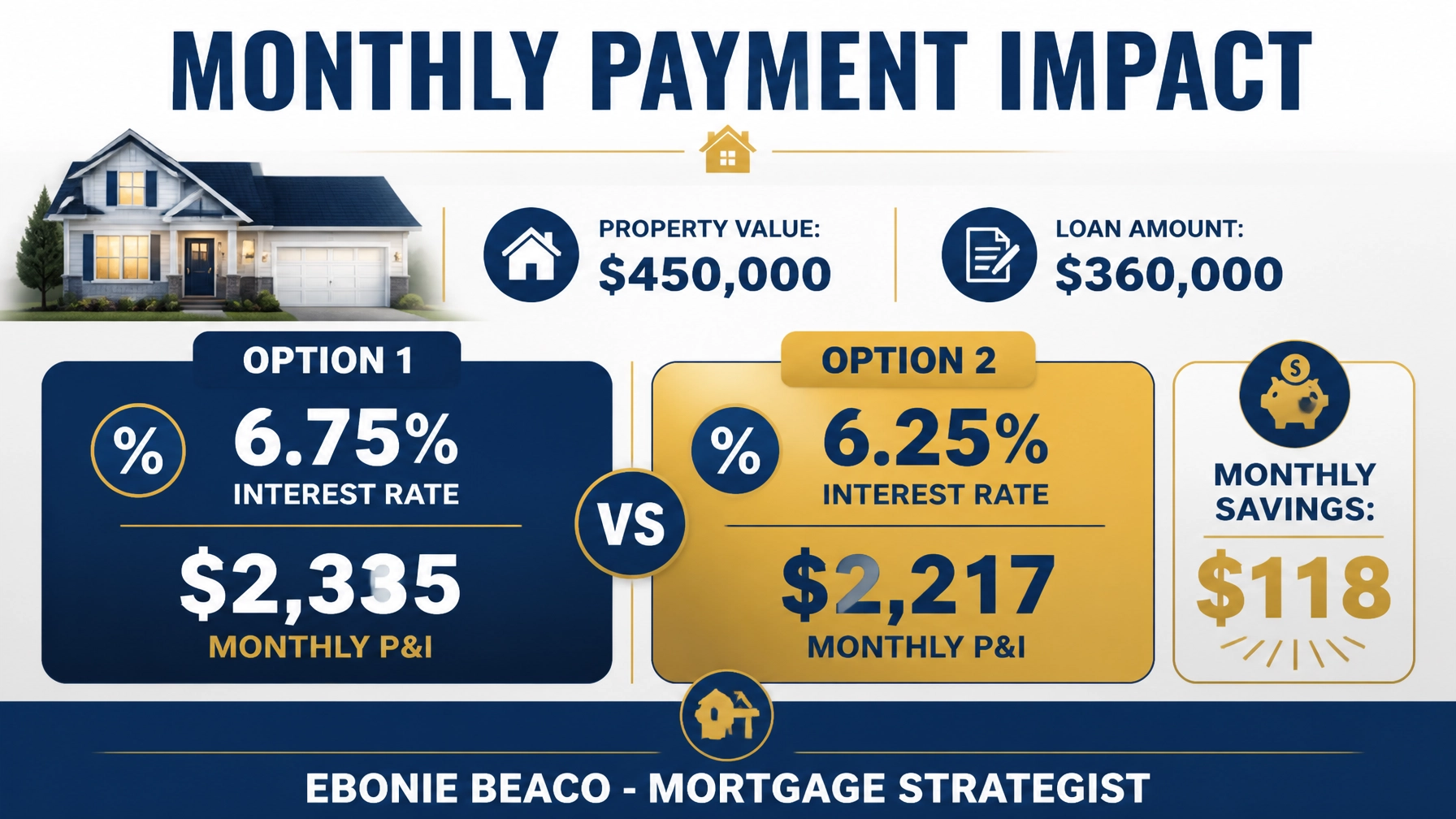

To illustrate how these economic shifts translate into real-world costs, let’s look at a common scenario for a home purchase in 2026. Consider a property valued at $450,000 with a standard 20% down payment, resulting in a loan amount of $360,000. If the economic data this week pushes rates from 6.25% to 6.75%, the monthly principal and interest payment changes noticeably. This seemingly small difference can determine whether a first-time homebuyer stays within their comfortable budget or if an investor maintains a positive cash flow on a rental property.

In this example, the difference of 0.50% in the interest rate leads to a monthly payment increase of $118. Over a 30-year term, that adds up to $42,480 in additional interest payments. For a real estate investor utilizing a DSCR (Debt Service Coverage Ratio) loan, this increase could drop the ratio below the required threshold, necessitating a larger down payment to close the deal. Calculating these scenarios in advance allows you to prepare for various market outcomes and avoid surprises at the closing table.

Strategies for Homeowners and Investors

If you are currently under contract or considering a refinance, the current week requires a strategic approach. Homeowners looking to access cash through a HELOC or a cash-out refinance should evaluate whether locking their rate now is preferable to waiting for the post-jobs report reaction. Often, the market "prices in" expected data before it is even released, meaning the best time to act might be prior to the news cycle hitting the mainstream media. Investors focusing on fix-and-flip projects or bridge loans should also keep a close eye on these trends to manage their carrying costs effectively.

According to industry analysis from The Mortgage Reports, the forecast for June remains cautiously optimistic, but dependent on cooling inflation. Additional data from Norada Real Estate suggests that while "wiggles" in rates are expected, the long-term trend for 2026 is toward stabilization. Use these insights to guide your decision-making and stay ahead of the competition in your local real estate market.

Ready to navigate the June 2026 market with confidence?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664