June 1st Mortgage Market Update: Today’s Rate Shifts Explained in Under 3 Minutes

The mortgage market entered June 2026 with a sense of cautious stability as the industry processes the latest signals from the Federal Reserve and inflation indices. Today, the national average for a 30-year fixed-rate mortgage is hovering between 6.4% and 6.6%, a range that has become a baseline for many borrowers in the first half of the year. While we are seeing a narrow trading range for conventional loans, the slight easing of bond yields last week has provided a small window for those looking to lock in purchase rates or explore refinancing options. Understanding these micro-shifts is essential for homeowners and investors who are navigating the current "higher-for-longer" economic environment while waiting for more definitive rate cuts.

Today’s Key Mortgage Definitions and Applications

Basis Point (BPS)

A unit of measure used in finance to describe the percentage change in the value or rate of a financial instrument. One basis point is equal to 0.01%, meaning 100 basis points equals 1%. In today's market, a shift of even 10 to 15 basis points can significantly alter the monthly payment on a high-balance loan in states like California or Virginia.

10-Year Treasury Yield

The interest rate the U.S. government pays to borrow money for a decade, which serves as a primary benchmark for long-term mortgage rates. When investors buy Treasury bonds, yields typically fall, leading to lower mortgage rates for consumers. Today’s yield stability suggests that lenders are maintaining their current pricing structures without immediate pressure to spike or slash rates.

Debt-to-Income Ratio (DTI)

A personal financial measure that compares an individual's monthly debt payments to their monthly gross income. Lenders use this to evaluate your ability to manage monthly payments and repay borrowed money. Maintaining a low DTI is particularly critical now, as higher interest rates naturally increase the debt portion of this equation, making qualification more stringent for conventional loans.

Regional Market Activity: From the Midwest to the Southeast

Housing activity across the primary states I serve: Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia: remains varied based on local inventory levels. In metro areas like Chicago and the high-demand corridors of Northern Virginia, buyers are still facing competitive bidding environments despite the current rate levels. This suggests that the latent demand we have tracked throughout the spring is beginning to manifest as buyers adjust their expectations to the new normal of mid-6% rates. Meanwhile, in markets like Alabama and Arkansas, the lower entry prices for single-family homes are allowing first-time buyers to enter the market more comfortably than in the high-cost coastal regions.

Florida and Georgia continue to see robust interest from real estate investors who are utilizing specialized products to scale their portfolios. Short-term rental operators in Florida are increasingly looking toward Airbnb and short-term rental financing to capitalize on the upcoming summer travel season. Similarly, in Georgia, the "Blended Rate" strategy is gaining popularity among homeowners who want to access equity without touching their low-interest primary mortgage. These regional nuances highlight the importance of localized data when making a financing decision that aligns with your specific wealth-building goals.

Strategic Financing for Real Estate Investors

For professional landlords and real estate investors, the current market requires a shift from traditional qualifying methods to more asset-based approaches. DSCR (Debt Service Coverage Ratio) Loans are currently a primary tool for those acquiring or refinancing rental properties because they qualify the borrower based on the property’s cash flow rather than personal tax returns. This is an ideal solution for self-employed entrepreneurs or investors with complex portfolios who may have high write-offs that impact their traditional DTI. Explore how DSCR rental property loans can help you acquire a multi-unit building or a single-family rental without the hurdles of conventional underwriting.

Hard Money and Bridge Loans are also seeing increased usage in the "fix and flip" sector in cities throughout Michigan and Indiana. Investors use these short-term financing solutions to acquire distressed properties, fund renovations, and then transition into long-term financing or sell for a profit. According to The Mortgage Reports, while national averages are stable, the speed of your financing can often be the difference between winning and losing a deal in a tight inventory market. By leveraging bridge loans, you can move quickly on an opportunity and then restructure your debt once the property’s value has increased.

Analyzing Home Equity Access in a High-Rate Environment

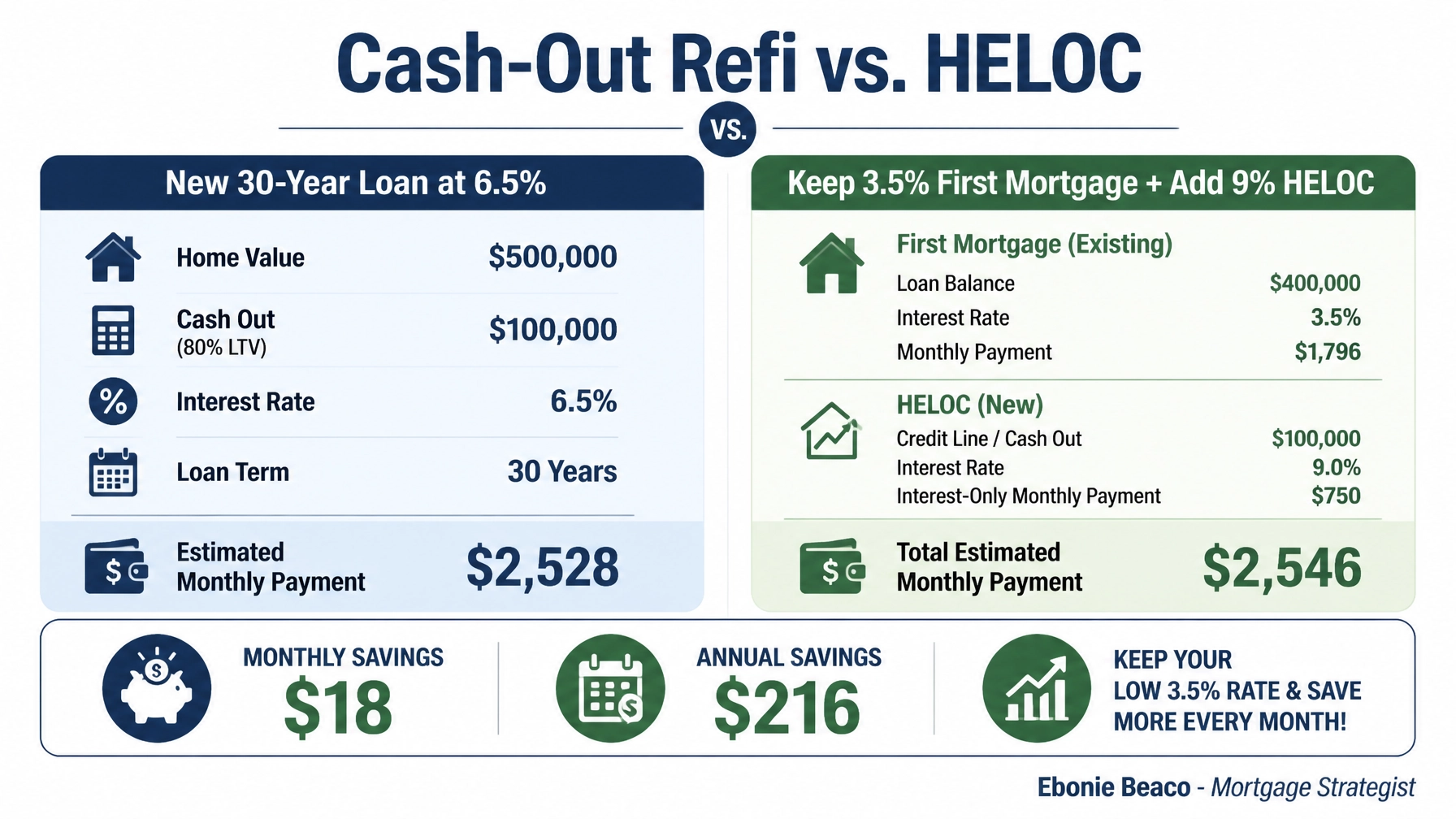

Many homeowners today are sitting on significant equity but are hesitant to move because they currently hold a primary mortgage rate between 3% and 4%. A full cash-out refinance would require replacing that entire low-rate loan with a new loan at today’s 6.5% rate, which often results in a much higher monthly commitment. To avoid this, a Home Equity Line of Credit (HELOC) or a fixed-rate second mortgage can be a more surgical way to access capital for home improvements or debt consolidation. This allows you to keep your primary low rate untouched while only paying the current market rate on the smaller amount you actually borrow.

Consider a practical example of a homeowner in California with a property valued at $800,000 and an existing loan balance of $400,000 at 3.25%. If they need $150,000 for a renovation project, they have two main paths to consider:

- Full Cash-Out Refinance: They take a new $550,000 loan at a 6.5% interest rate. Their monthly principal and interest payment would jump significantly because the entire $550,000 is now at the higher rate.

- The HELOC Strategy: They keep their $400,000 loan at 3.25% and take out a separate $150,000 HELOC at a variable rate (currently around 9%).

In this scenario, the "Blended Rate": the average interest rate paid across both loans: is often much lower than the 6.5% they would get on a total refinance. You can use our mortgage calculators to run these numbers for your own home and see which path saves you more money over the long term. This strategic approach ensures that you are utilizing your home's equity without unnecessary financial waste.

Looking Ahead: What to Expect in the Coming Weeks

As we move deeper into June, the market will be hyper-focused on upcoming Consumer Price Index (CPI) reports and the Fed's commentary. Experts surveyed by Bankrate suggest that we are in a period of "stability," meaning we shouldn't expect the 30-year fixed rate to drop to 5% or spike to 8% overnight. Instead, we are looking at a series of small, incremental moves that favor the prepared borrower who has their documentation ready and their credit score optimized. If you are an investor looking to scale or a homeowner looking to tap into your property's value, the best strategy is to stay informed and act when the numbers align with your investment criteria.

Navigating the mortgage landscape in 2026 requires more than just looking at a daily rate sheet; it requires a comprehensive strategy that accounts for your entire financial profile. Whether you are interested in home equity made easy or sophisticated investor loans, I am here to guide you through every step of the process. The market shifts daily, but your long-term goal of building wealth through real estate remains a constant priority that we can achieve together through education and transparent guidance.

Jump in and explore your options today to see how the current market can work in your favor.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664