ITIN Mortgages: How to Buy Property in Indiana

Buying a home or an investment property is a major milestone, but for those without a Social Security Number (SSN), the process can feel out of reach.

If you live in Indiana and pay taxes using an Individual Taxpayer Identification Number (ITIN), you have options to enter the real estate market.

ITIN mortgages are specialized home loans designed specifically for individuals who are not eligible for an SSN but still want to build wealth through property ownership.

Whether you are looking for a primary residence in Indianapolis or a rental property in Fort Wayne, understanding how these loans work is the first step toward your goal.

Understanding the ITIN Mortgage

An ITIN mortgage is a type of Non-QM (Non-Qualified Mortgage) loan.

Traditional lenders often require an SSN for standard conventional or FHA loans.

Non-QM lenders, however, use different criteria to evaluate your ability to repay a loan, making it possible to use your ITIN for the application.

This path allows foreign nationals, resident aliens, and self-employed individuals to participate in the American dream of property ownership.

You can explore more about these specialized programs by visiting our mortgage basics page.

Who Can Use an ITIN Loan?

These loans are not just for one specific group of people.

They serve a wide range of individuals who contribute to the economy and pay taxes but lack a traditional social security status.

Foreign Nationals

If you are a citizen of another country looking to invest in Indiana real estate, an ITIN loan provides the necessary framework.

Non-Resident and Resident Aliens

Individuals living in the U.S. for work or family reasons who do not yet have an SSN can qualify using their tax identification number.

Self-Employed Individuals

Many people working as independent contractors find that an ITIN loan offers the flexibility they need when traditional banks turn them away.

Key Requirements for Indiana ITIN Mortgages

The requirements for an ITIN loan are different from standard mortgages, often requiring more documentation and a larger initial investment.

Credit Score Expectations

Lenders typically look for a minimum FICO score of 600 to 620.

While some programs allow for "alternative credit" like utility bills or rent payments, having a traditional credit score usually results in better interest rates.

The Down Payment

Expect to put more money down than you would with an FHA loan.

Most ITIN mortgage programs require a minimum of 20% down.

In some cases, if your credit score is lower, a lender might ask for 25% or even 30% to offset the risk.

Debt-to-Income (DTI) Ratio

Your DTI is a comparison of your monthly debt payments to your gross monthly income.

For ITIN loans, lenders often allow a DTI of up to 50%, though keeping it lower helps ensure you can comfortably afford the home.

Income Documentation and Stability

To qualify, you must show that you have a stable financial history.

Lenders generally require at least 12 months of consistent employment history.

You will also need to provide two years of tax returns filed with your ITIN.

This proves to the lender that you are a consistent taxpayer and have a reliable stream of income to cover the mortgage payments.

The Role of Cash Reserves

Lenders want to see that you have a "safety net" in place.

It is common for ITIN loan programs to require up to 12 months of PITI (Principal, Interest, Taxes, and Insurance) in reserves.

This means if your monthly payment is $1,500, you might need $18,000 sitting in a bank account that has been "seasoned" for 60 to 90 days.

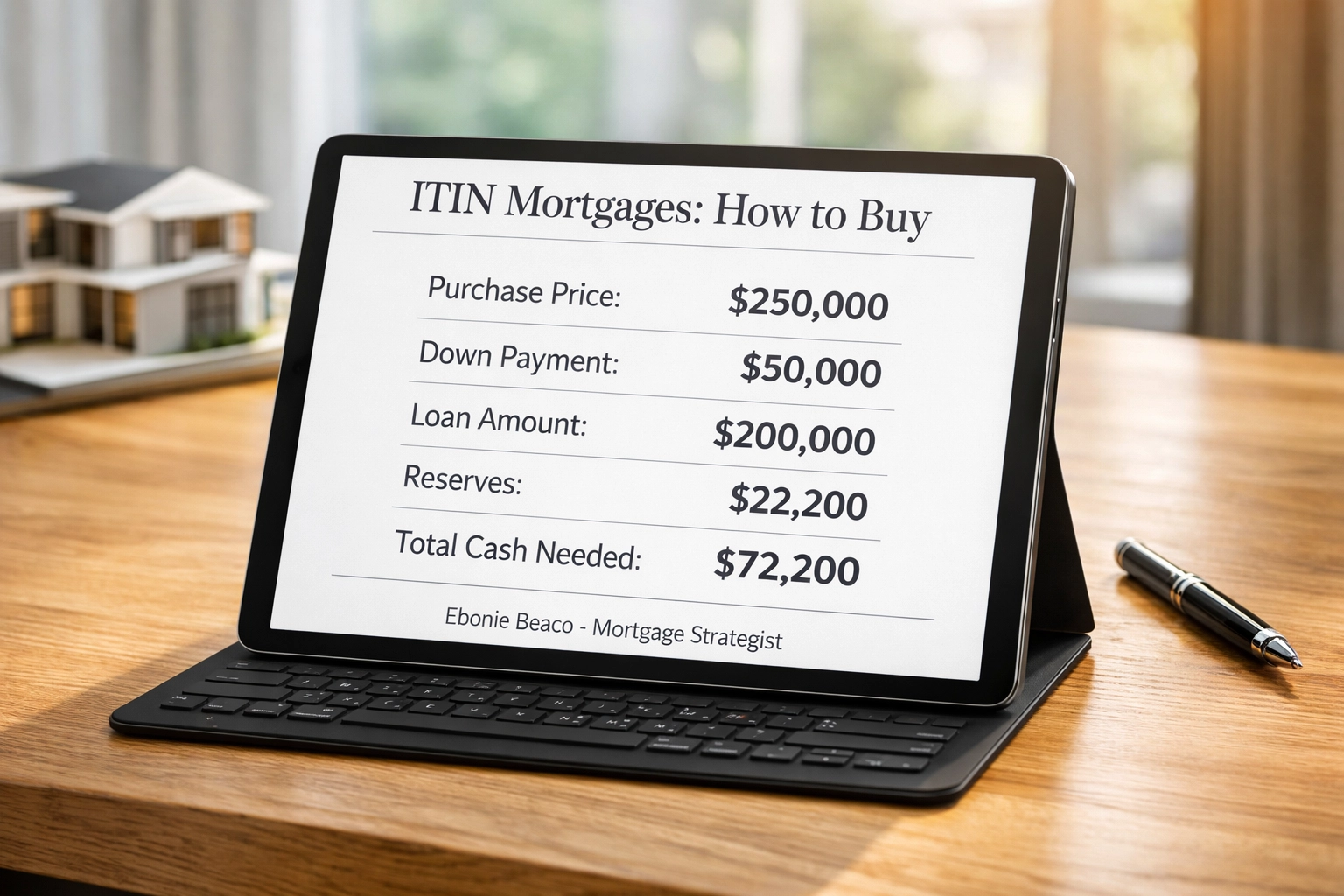

Real-World Calculation: Buying in Indiana

Let's look at a practical example of how the numbers work for an ITIN purchase.

Imagine you are buying a single-family home in a growing Indiana neighborhood for $250,000.

Purchase Price: $250,000

Down Payment (20%): $50,000

Loan Amount: $200,000

Interest Rate (Estimated): 7.5%

Monthly PITI (Estimated): $1,850

Required Reserves (12 Months): $22,200

Total Cash Needed (Excluding Closing Costs): $72,200

Title: ITIN Mortgages: How to Buy

Calculation Breakdown: Price $250k, Down Payment $50k, Loan $200k, Reserves $22,200, Total Cash $72,200

Ebonie Beaco - Mortgage Loan Officer

Title: ITIN Mortgages: How to Buy

Calculation Breakdown: Price $250k, Down Payment $50k, Loan $200k, Reserves $22,200, Total Cash $72,200

Ebonie Beaco - Mortgage Loan Officer

Steps to Apply for an ITIN Mortgage

The process moves quickly if you are prepared with the right paperwork.

1. Organize Your Documents

Collect your ITIN card or the authorization letter from the IRS.

Gather your last two years of tax returns and at least 12 months of bank statements.

2. Verify Your Residency

Provide proof of where you have been living, such as a rental agreement or utility bills in your name.

3. Consult a Specialist

Work with a mortgage strategist who understands the ITIN landscape.

You can start this journey by reviewing our loan process guide.

4. Submit Your Application

Once your documents are in order, your lender will process the file, verify your assets, and move you toward the closing table.

ITIN Mortgages for Real Estate Investors

Many people use ITIN loans to start or grow a rental portfolio.

Indiana is a popular market for investors because of its relatively affordable housing and steady rental demand.

As an investor, you can use these loans to purchase property even if you do not plan to live there.

If you are interested in more advanced strategies, you might also want to look into DSCR investor loans, which focus on the income the property generates rather than your personal income.

Navigating the Indiana Market

The Indiana real estate market is diverse.

From the urban pulse of Indianapolis to the suburban appeal of Carmel or the industrial growth in Gary, there are many opportunities.

Because ITIN loans are a niche product, it is vital to work with someone who can navigate the specific state regulations and lender requirements.

Transparency is key in these transactions to ensure there are no surprises during the underwriting process.

Common Questions About ITIN Loans

Can I use gift funds for the down payment?

Some lenders allow a portion of the down payment to be a gift from a family member, but they usually require that at least 10% of the purchase price comes from your own funds.

What is the maximum loan amount?

Many ITIN programs offer financing up to $1.5 million for primary residences, though this varies by lender and your specific financial profile.

Do I need a specific type of property?

Generally, you can use ITIN loans for single-family homes, townhomes, and even small multi-family units (2-4 units) if you plan to live in one of them.

Preparing for Success

Before you start looking at houses, use a mortgage calculator to see what your monthly payments might look like.

Having a clear picture of your budget ensures you are searching for properties within your financial reach.

Education is the best tool you have in the real estate world.

By learning the rules of ITIN financing, you position yourself as a savvy buyer or investor ready to take action.

Why Work with a Mortgage Strategist?

The path to homeownership using an ITIN can be complex, but it does not have to be overwhelming.

A mortgage strategist helps you compare different loan terms, explains the fine print, and guides you through the documentation requirements.

Whether you are a first-time buyer or a seasoned landlord looking to expand, having an expert in your corner can save you time and help you avoid common pitfalls.

If you have questions about your specific situation or want to see if you qualify, reaching out for a personalized consultation is the best next step.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664