ITIN Loans

Post Description

Buying a home is a core part of the American dream, but for many hardworking individuals without a Social Security Number, the path to ownership often feels blocked. ITIN loans change that narrative by allowing you to use your Individual Taxpayer Identification Number to secure a mortgage. Whether you are a resident alien, a foreign national, or an investor looking to scale a portfolio in markets like Chicago, Florida, or California, ITIN lending provides a transparent bridge to property ownership. These programs focus on your ability to repay rather than just a nine-digit government ID. At Home Loans Network, we believe your financial footprint should speak louder than your residency status. Explore how you can transition from renting to owning today. Book an appointment to discuss your specific scenario.

Understanding the ITIN Mortgage Landscape

The mortgage industry is vast, but traditional lending often leaves a gap for those who contribute to the economy but lack a Social Security Number (SSN).

ITIN Loan: A specialized mortgage program designed for individuals who have an Individual Taxpayer Identification Number issued by the IRS.

Practical Application: This allows non-SSN holders to qualify for home financing for primary residences or investment properties.

Many people assume that without an SSN, buying a house is impossible.

This is a common misconception.

ITIN loans fall under the Non-QM (Non-Qualified Mortgage) umbrella, meaning they do not follow the rigid rules of government-backed entities like Fannie Mae or Freddie Mac.

Instead, these loans focus on your tax history, income stability, and overall financial health.

If you live in states like Illinois, Georgia, or Virginia, you have likely seen vibrant communities where ITIN holders are active participants in the local real estate market.

Explore the mortgage basics to see how these programs differ from standard lending.

Who Qualifies for an ITIN Loan?

These programs target a specific group of borrowers who have established roots in the United States.

Typically, you are an ideal candidate if you are a non-U.S. citizen, a resident alien, or an individual ineligible for an SSN.

Lenders look for consistency.

They want to see that you have been working, paying taxes, and managing your finances responsibly.

Whether you are a self-employed contractor in Michigan or a business owner in Arkansas, your income counts.

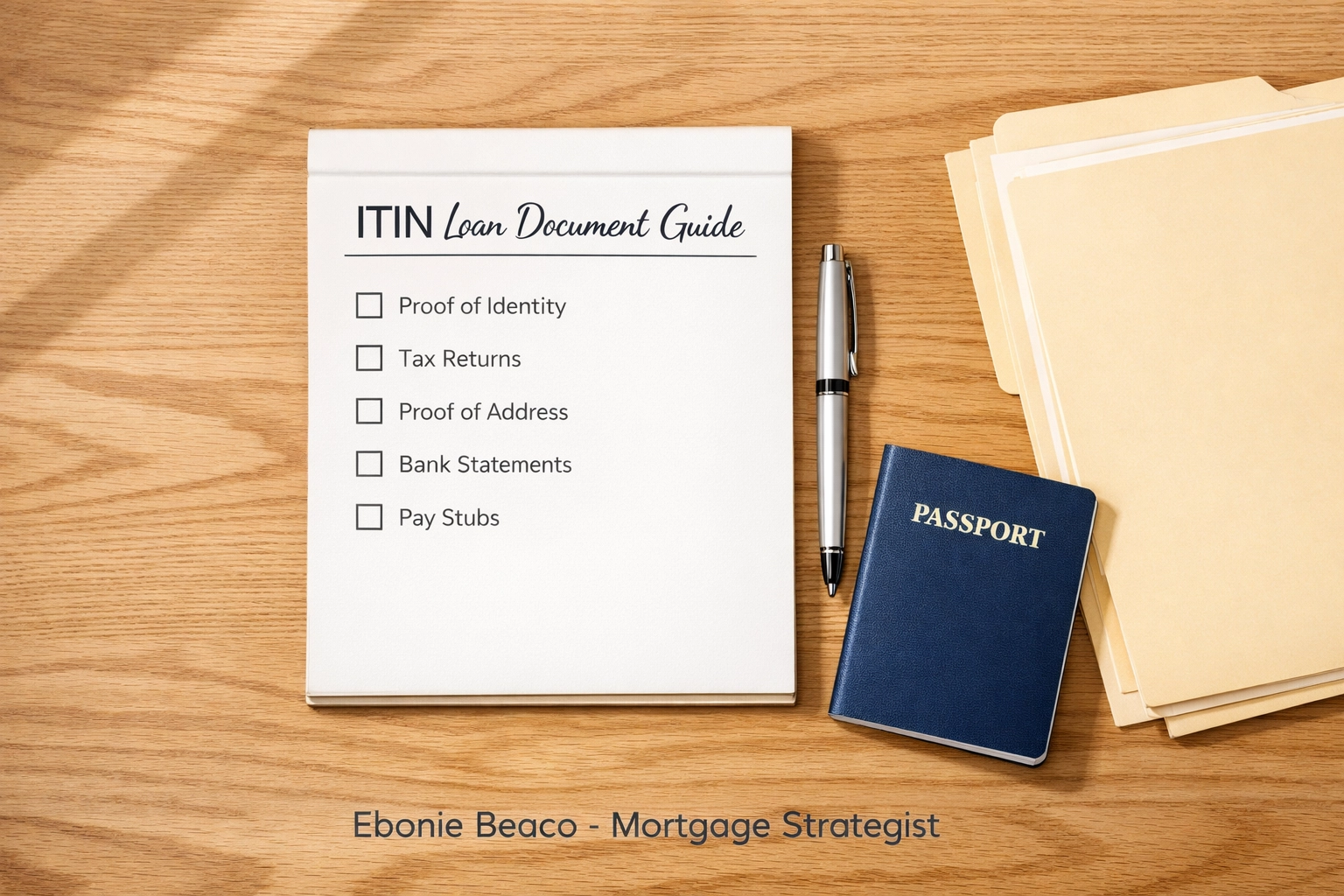

Accessing a home purchase loan through an ITIN program requires specific documentation that replaces the standard SSN requirement.

The Essential Documentation Checklist

Preparation is the key to a smooth closing.

Because ITIN loans are a niche product, the documentation requirements are often more detailed than a standard conventional loan.

- ITIN Authorization Letter: This is the official document from the IRS assigning your number.

- Proof of Identity: A valid passport or a government-issued photo ID from your country of origin.

- Tax Returns: Usually, two years of federal tax returns to show a consistent history of filing.

- Income Verification: W-2s or 1099s, along with recent pay stubs.

- Bank Statements: Usually 12 to 24 months of statements to verify down payment funds and reserves.

If you are curious about the timeline, you can review our loan process to understand each step.

Description: A checklist graphic titled "ITIN Loan Document Guide" showing a list: ITIN Letter, Passport/ID, 2 Years Tax Returns, and 12 Months Bank Statements. Footer: Ebonie Beaco - Mortgage Strategist.

Financial Requirements and Expectations

Transparency is vital when discussing ITIN loans.

Because these loans carry a perceived higher risk for lenders, the terms differ from standard FHA or Conventional loans.

Down Payment: The portion of the home price paid upfront by the borrower.

Practical Application: For ITIN loans, expect to put down between 15% and 20% of the purchase price.

Interest Rates: The cost of borrowing money, expressed as a percentage.

Practical Application: ITIN mortgage rates are typically higher than traditional rates due to the specialized nature of the program.

While the down payment might be higher, these loans offer a path to build equity in markets like California and Florida where property values have historically increased.

You are not just paying a mortgage; you are investing in an asset.

ITIN Loans for Real Estate Investors

The ITIN program is not limited to primary residences.

Many real estate investors use ITIN financing to build rental portfolios.

If you are a landlord in Chicago or looking at vacation rentals in Florida, this program allows you to scale.

Investors often use ITIN loans to execute the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat).

By purchasing a property with an ITIN loan, renovating it, and then performing a cash-out refinance, you can pull out equity to fund your next deal.

This strategy is particularly effective for those who may not have a traditional credit score but have the capital and the tax history to prove their reliability.

A Real-World Financing Example

Let’s look at a scenario for a buyer in the Chicago, Illinois area.

Imagine an individual who has been working as a self-employed contractor for three years and wants to purchase a single-family home.

- Purchase Price: $350,000

- Down Payment (20%): $70,000

- Loan Amount: $280,000

- Property Type: Single-family residence

In this case, the borrower provides two years of tax returns showing a steady net income.

They show 12 months of bank statements to prove they have the $70,000 plus closing costs.

Even without a traditional Social Security Number, they successfully close on the home and begin building wealth.

Description: A financial chart titled "ITIN Loan Breakdown - Chicago Property". Figures: Purchase Price $350k, Down Payment $70k, Loan Amount $280k, Estimated Monthly Payment. Footer: Ebonie Beaco - Mortgage Strategist.

Credit and Alternative Credit Scores

One of the biggest hurdles for ITIN borrowers is the lack of a traditional FICO score.

However, many ITIN lenders are willing to look at "alternative credit."

Alternative Credit: A way of measuring creditworthiness using non-traditional data like rent payments or utility bills.

Practical Application: You can use 12 months of on-time rent or cell phone bill history to prove you are a reliable borrower.

This flexibility is why it is important to work with a Mortgage Strategist who understands the nuances of ITIN lending.

If you need help understanding your current standing, check our FAQ for more details.

Why ITIN Lending is Expanding

The demand for these loans is growing in states like Georgia, Virginia, and Indiana.

As communities grow, the need for inclusive financing becomes more apparent.

Lenders are recognizing that ITIN holders are often some of the most dedicated homeowners and investors.

By utilizing these programs, you are contributing to the stability of your local housing market.

Whether you are buying a duplex in Alabama or a condo in Florida, ITIN loans provide the leverage you need.

Jump in and see how your tax ID can work for you.

The first step is always education.

You can download your ebook to learn more about various specialized lending strategies.

Navigating the ITIN Application Process

The process starts with ensuring your ITIN is active.

If you haven't used it for several years, it may have expired.

Check with the IRS or a tax professional first.

Once your ITIN is ready, the next step is a pre-approval.

This gives you the confidence to shop for homes in competitive markets like California or Florida.

Knowing exactly what you can afford prevents wasted time and potential heartbreak.

Compare your options carefully.

Every lender has slightly different requirements for ITIN programs.

Some might require more "reserves" (money left in the bank after closing), while others might be more flexible with the down payment.

Description: An infographic titled "ITIN Loan Steps to Success". Steps: 1. Confirm ITIN Status. 2. Get Pre-Approved. 3. Find Your Property. 4. Submit Documentation. 5. Close Your Loan. Footer: Ebonie Beaco - Mortgage Strategist.

Taking the Next Step Toward Ownership

Owning real estate is one of the most effective ways to build long-term security.

An ITIN number should not be a barrier to your goals.

By focusing on your tax history and financial stability, Home Loans Network helps bridge the gap between where you are and where you want to be.

If you are ready to see if you qualify, or if you just want to talk through a scenario, we are here to guide you clearly and confidently.

Your journey doesn't have to be complicated when you have the right information.

Explore your ITIN loan options and start your homeownership journey today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664