Is Your Credit Score Still the Deciding Factor in 2026? Today’s Mortgage News for Self-Employed Borrowers

The mortgage landscape in May 2026 continues to evolve as lenders balance risk with the growing needs of a diverse workforce. For self-employed entrepreneurs, freelancers, and small business owners, the question of financial qualification remains a top priority. While traditional banks often rely heavily on tax returns that may show significant write-offs, the alternative lending market has expanded its reach significantly. We are seeing a more disciplined expansion where documentation flexibility is paired with clear credit expectations to ensure long-term stability. Understanding where you stand in today's market is the first step toward securing the financing you need for your next primary residence or investment property.

The Shift in Credit Score Expectations

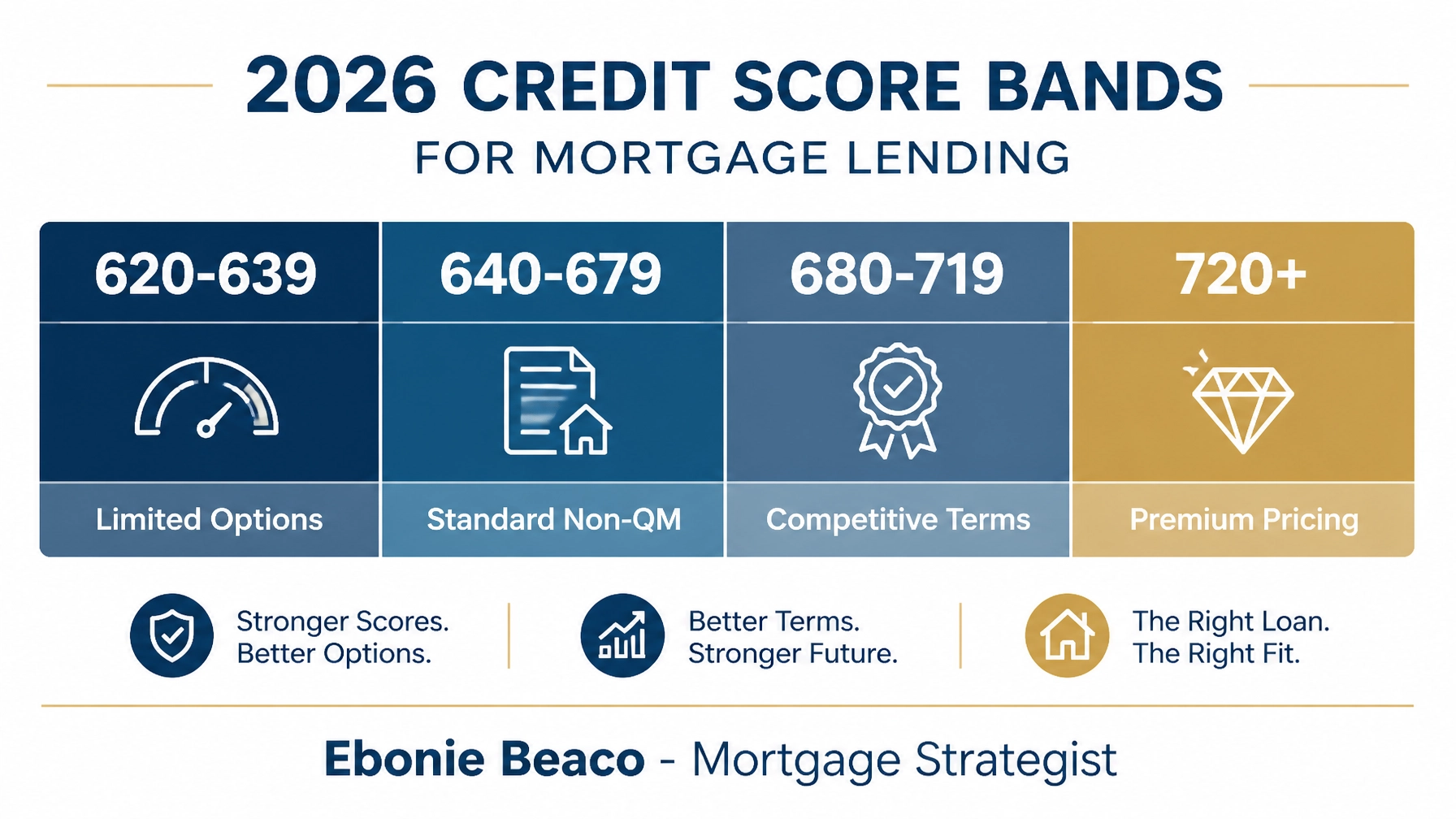

As we navigate through 2026, the weight placed on a FICO score has shifted from a "pass-fail" metric to a tier-based system that determines your overall loan terms. Lenders in the non-QM space now clearly define benefits based on specific credit bands, allowing for more transparency during the pre-approval process. For instance, a score between 620 and 639 may still secure a loan, but it often requires a larger down payment, typically around 20% to 25%. Conversely, reaching the 720 or 760+ threshold opens doors to premium pricing and lower down payment options, sometimes as low as 10% for well-qualified self-employed individuals. You can explore these different tiers by reviewing our comprehensive loan programs designed for non-traditional borrowers.

Credit scores continue to be a primary tool for risk assessment, but they are no longer the only factor considered in a holistic mortgage review. Many lenders now look at the "why" behind the score, offering more leniency for past credit events like a bankruptcy or foreclosure if the recent payment history is strong. This shift is particularly beneficial for investors in states like Florida and California, where market volatility in previous years may have impacted personal finances. If you are curious about your current standing, a soft pull credit request is an excellent way to check your score without impacting your credit history. Keeping a close eye on your score ensures you are positioned to grab the best rates as they fluctuate throughout the year.

Mortgage Solutions Tailored for the Self-Employed

The traditional mortgage process often feels like a mismatch for the modern entrepreneur whose income fluctuates or is shielded by legal tax deductions. In response, the industry has solidified Bank Statement Loans as a premier solution for those who cannot qualify using standard W-2 logic. These programs allow you to use 12 to 24 months of personal or business bank deposits to calculate a qualifying monthly income. This method provides a much more accurate reflection of your actual cash flow and purchasing power in competitive markets like Chicago or Atlanta. By focusing on your gross deposits rather than your net taxable income, you can often qualify for a much higher loan amount than you previously thought possible.

DSCR (Debt Service Coverage Ratio): A metric used primarily for investment property loans that compares the property's annual net operating income to its annual debt service. This allows investors to qualify based on the property’s performance rather than their personal income.

LTV (Loan-to-Value): The ratio of a loan to the value of an asset purchased, expressed as a percentage. In 2026, LTV limits are strictly tied to credit scores, with higher scores allowing for higher leverage.

Non-QM (Non-Qualified Mortgage): A type of loan that does not conform to the standard federal guidelines for mortgages. These loans are essential for borrowers with unique financial situations, such as the self-employed or those with high net worth but low taxable income.

Real-World Scenario: The Chicago Self-Employed Purchase

To understand how these numbers translate into real action, let's look at a recent scenario for a business owner in Chicago, Illinois. Imagine you are purchasing a $800,000 single-family home and your tax returns show minimal income due to aggressive business reinvestment. With a credit score of 680, you fall into a competitive tier that allows for a 20% down payment, which equals $160,000. Using a 12-month bank statement program, the lender analyzes your total deposits to establish a qualifying monthly income that supports the $640,000 loan amount. This approach bypasses the limitations of tax returns and focuses on your actual ability to manage the monthly mortgage payment.

This strategy is not just limited to Illinois; it is a vital tool for borrowers across the country, from the suburbs of Virginia to the growing tech hubs in Missouri and Kentucky. By structuring the deal this way, the borrower avoids the need for a co-signer and maintains full ownership of the asset while leveraging their business success. The loan process for these types of mortgages is streamlined to be as efficient as a traditional loan, provided the documentation is organized and ready for review. It is a powerful example of how modern financing can be customized to fit your specific professional profile and long-term wealth goals.

Navigating Local Markets Across the U.S.

The mortgage trends of May 2026 are not uniform, as each state presents its own set of opportunities and challenges for borrowers. In Florida and Georgia, we are seeing a surge in DSCR loans for short-term rental properties as tourism demand remains high. Meanwhile, in Michigan and Indiana, first-time homebuyers are increasingly looking at down payment assistance programs to bridge the gap in affordability. California and Virginia continue to see high demand for jumbo non-QM products, where credit scores above 740 are highly rewarded with lower margins. No matter where you are located, from Alabama to Arkansas, having a local strategy is essential for navigating the current interest rate environment.

Current data suggests that while rates have stabilized, the inventory remains tight in major metropolitan areas, making a strong pre-approval more important than ever. If you are an investor looking to scale your portfolio or a homeowner looking to tap into your equity, understanding these regional nuances can save you thousands over the life of your loan. For more detailed insights into specific lending requirements, you can refer to established industry resources like Deephaven Mortgage or stay updated with general non-QM news from Bankrate. We are here to help you navigate these complexities and find the right path forward in your real estate journey.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664