Is Wholesaling Still Legal in Alabama? 2026 Regulation Check-In

Friday, March 27, 2026

If you are active in the Birmingham, Mobile, or Huntsville real estate markets, you have likely heard the whispers or seen the headlines about the shifting landscape of wholesaling. Many investors are asking the same question: Is wholesaling still legal in Alabama?

The short answer is yes. However, the way you operate in 2026 is vastly different than it was just a few short years ago. With the full implementation of Senate Bill 246 (SB 246) as of January 1, 2026, the Alabama Real Estate Commission (AREC) has tightened the screws on how "equitable interest" is marketed and sold.

The goal of these changes is transparency. The state wants to ensure that homeowners know exactly who they are dealing with and that unlicensed individuals are not acting as "de facto" real estate brokers. Let's jump in and explore what you need to know to keep your investment business compliant and profitable in this new regulatory era.

Instruction: Professional real estate theme showing a modern Alabama home exterior with a clean, blue sky. No cash or money visuals. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Instruction: Professional real estate theme showing a modern Alabama home exterior with a clean, blue sky. No cash or money visuals. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Understanding the 2026 Regulatory Landscape

The primary shift in 2026 revolves around the definition of a "broker." Historically, wholesalers operated in a gray area, claiming they were simply "assigning a contract." While that remains a legal practice, the state now looks closely at how you market that contract.

If you are out here acting like a real estate agent, listing properties you don’t own on the MLS without a license or representing yourself as the owner when you only hold a contract, you are stepping into a legal minefield. SB 246 was designed to eliminate "unlicensed brokerage" by requiring specific, written disclosures at every stage of the transaction.

Key Definitions for the 2026 Market

To navigate these waters, you need to understand the technical terms that AREC and Alabama law now emphasize.

- Equitable Interest: The legal right to obtain full ownership of a property through a signed purchase agreement. In Alabama, as a wholesaler, this is the only thing you are legally allowed to sell without a real estate license.

- Assignment of Contract: A legal transaction where one party passes their rights and obligations under a contract to another party. This remains the primary vehicle for wholesaling deals in 2026.

- Unlicensed Brokerage: Engaging in real estate activities that require a license, such as negotiating for others or marketing property you do not own. The state has increased penalties for this activity to protect consumers from non-transparent deal-making.

- Disclosure of Interest: A mandatory written statement informing a seller that the buyer is an investor who intends to sell their contract rights for a profit. This is now a non-negotiable requirement for every wholesale deal in Alabama.

The Disclosure Requirement: Transparency is Mandatory

In 2026, transparency is the name of the game. You can no longer hide your intentions from the seller. Under the current Alabama regulations, you must provide a clear, written disclosure that states:

- You are not the owner of the property.

- You hold an "equitable interest" via a purchase agreement.

- You intend to assign that agreement to a third party for a fee.

- You are not acting as a licensed real estate agent or broker.

Failure to provide this disclosure can lead to heavy fines from AREC and can make your contracts voidable. This means a seller could potentially back out of a deal at the last minute if they weren't properly informed of your role as a wholesaler. You can find more about the foundational elements of real estate transactions at https://www.homeloansnetwork.com/mortgage-basics.

Instruction: A professional close-up of a person’s hand holding a pen over a legal document with the word "DISCLOSURE" clearly visible at the top. Professional office setting. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Instruction: A professional close-up of a person’s hand holding a pen over a legal document with the word "DISCLOSURE" clearly visible at the top. Professional office setting. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Avoiding the "Broker" Trap

The most significant change in 2026 is the crackdown on how wholesalers market their deals. In the past, it was common to see "House for Sale" ads from wholesalers. Today, that language can get you in trouble.

To stay compliant, your marketing must focus on the contract, not the house.

- Incorrect Marketing: "3-bed, 2-bath home for sale in Montgomery for $150k. Call me to buy it."

- Correct Marketing: "Assignment of contract available for a 3-bed, 2-bath property in Montgomery. Equitable interest for sale at $10,000."

By shifting your language, you clarify that you are selling your legal position in a deal, not the real estate itself. This distinction is what keeps you on the right side of the "unlicensed brokerage" laws. If you are looking to transition from wholesaling to actually owning properties, exploring https://www.homeloansnetwork.com/home-purchase can help you understand the financing side of things.

Financing and Wholesaling in 2026

As a mortgage strategist, I often see wholesalers who want to evolve into "Wholetailing" or "Fix and Flip" investing. While wholesaling is a great way to build capital, the 2026 regulations make it even more important to have a solid financing partner.

If a deal is too good to assign, or if the new regulations make an assignment too complex for a specific seller, you might choose to perform a Double Closing. This is where you actually buy the property and sell it to your end buyer on the same day (or shortly after).

For a double closing, you’ll often need:

- Transactional Funding: Short-term loans used specifically for double closings.

- Bridge Loans: Short-term financing to bridge the gap between purchase and resale.

- Hard Money: Loans based on the property value rather than your personal credit.

Compare your options and access our team's guidance on https://www.homeloansnetwork.com/loan-process to see which path fits your current deal structure.

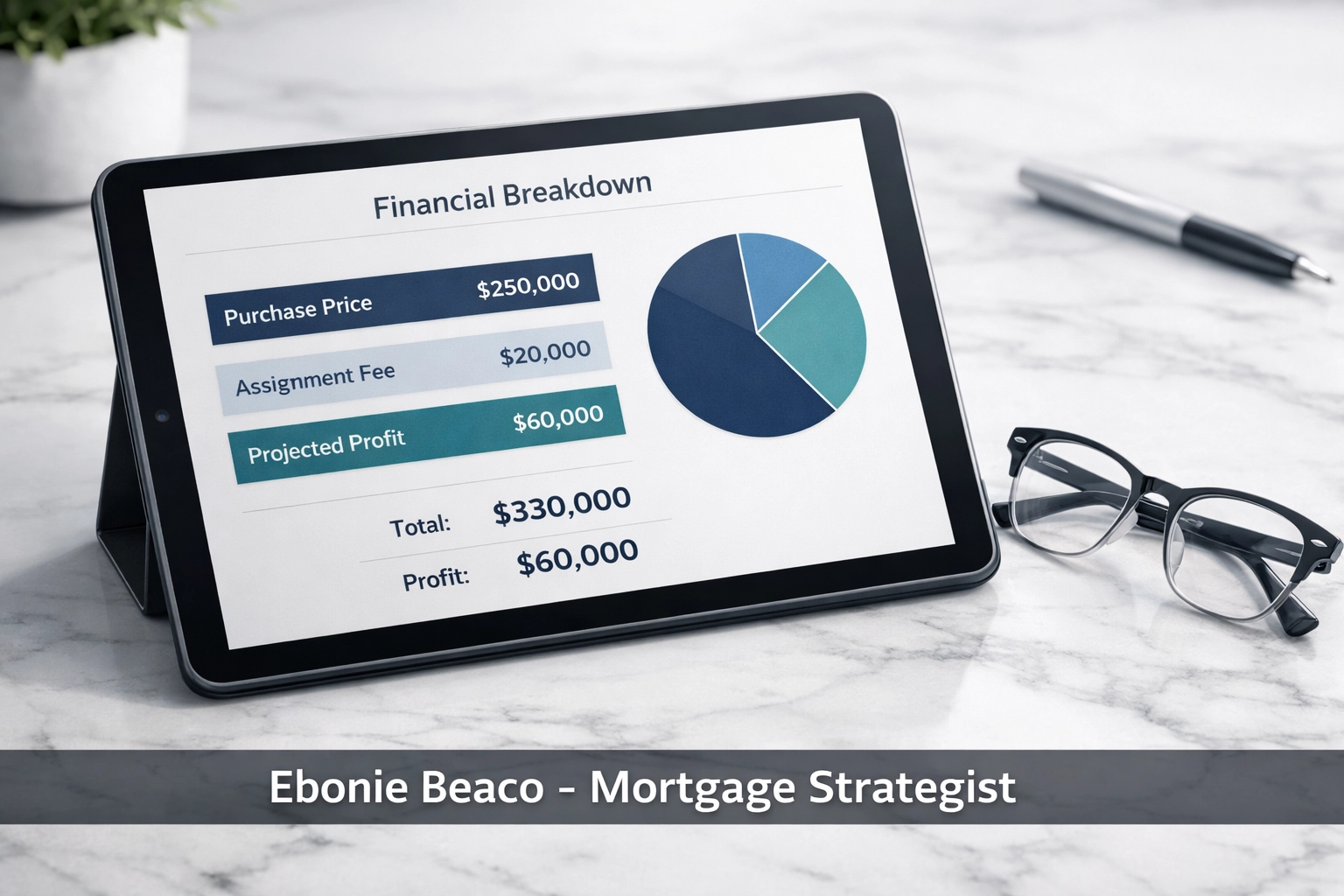

Real-World Example: A Compliant 2026 Wholesale Deal

Let's look at how the numbers and the process work under the new Alabama rules. Imagine you find a distressed property in Birmingham.

| Item | Amount |

|---|---|

| Agreed Purchase Price with Seller | $180,000 |

| Wholesaler’s Equitable Interest Fee | $15,000 |

| Total Price to End Investor | $195,000 |

| End Investor’s Estimated Repair Cost | $40,000 |

| After Repair Value (ARV) | $310,000 |

In this scenario, you must provide the seller with a written disclosure at the time of the $180,000 offer, stating that you are an investor and intend to assign the contract. When you market the deal to your cash buyers, you are marketing the assignment for $15,000.

Instruction: A clean, professional financial table or chart showing the breakdown of a real estate deal: Purchase Price, Assignment Fee, and ARV. Clear and easy to read. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Instruction: A clean, professional financial table or chart showing the breakdown of a real estate deal: Purchase Price, Assignment Fee, and ARV. Clear and easy to read. Text overlay: "Ebonie Beaco - Mortgage Strategist"

How to Stay Legal and Profitable

If you want to thrive as a wholesaler in Alabama through 2026 and beyond, follow these steps:

- Use State-Specific Contracts: Do not use generic contracts found online. Ensure your purchase agreements include the mandatory Alabama disclosures.

- Build a Relationship with a Title Company: Work with a title company that understands wholesaling and the 2026 SB 246 requirements.

- Be Honest with Sellers: Transparency builds trust and prevents legal headaches. Explain that you are an investor who helps solve property problems by connecting sellers with cash buyers.

- Keep Your Marketing Precise: Always mention that you are selling an "assignment of contract" or "equitable interest."

- Consult with Professionals: Before signing contracts, have them reviewed by a real estate attorney who is well-versed in the latest AREC guidelines.

Beyond Wholesaling: Scaling Your Business

Many wholesalers eventually grow tired of the constant "hustle" of finding deals only to give them away for a fee. If you are ready to start building long-term wealth, you might consider the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) or purchasing rental properties using DSCR Loans.

DSCR (Debt Service Coverage Ratio) loans are perfect for investors because they qualify the loan based on the property's rental income rather than your personal debt-to-income ratio. This allows you to scale your portfolio much faster than traditional financing. Explore our DSCR Investor Loans to see how you can transition from wholesaling to landlording.

Whether you are wholesaling in Mobile or looking for a cash-out refinance on a rental in Huntsville, the key is having a strategy that accounts for the current regulatory and financial environment.

Instruction: A professional image of a group of diverse real estate professionals in a bright, modern office discussing plans over a large table. No money shown. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Instruction: A professional image of a group of diverse real estate professionals in a bright, modern office discussing plans over a large table. No money shown. Text overlay: "Ebonie Beaco - Mortgage Strategist"

Frequently Asked Questions

Do I need a real estate license to wholesale in Alabama in 2026? No, you do not need a license as long as you are selling your "equitable interest" in a contract and providing all required disclosures. If you represent yourself as an agent or market the physical property without a license, you are violating the law.

Can I list my wholesale deals on the MLS? Generally, no. The MLS is for licensed brokers. Without a license, you cannot list a property you do not own. Some "flat fee" MLS services exist, but in 2026, AREC is very strict about unlicensed individuals using these platforms to market equitable interests.

What are the penalties for non-compliance? AREC can issue cease and desist orders, impose heavy administrative fines, and refer cases for criminal prosecution if they believe you are practicing real estate without a license.

Final Thoughts

Wholesaling is still a viable and legal strategy in Alabama. The 2026 regulations aren't here to kill your business; they are here to ensure the market remains transparent and fair for all parties. By embracing these changes and focusing on clear disclosures, you can build a reputable investment business that stands the test of time.

If you have questions about how to finance your next big deal or how to move from wholesaling into full-time investing, let's talk.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664