Is the Post-Memorial Day Rate Shift Significant in 2026? Today’s 7:00 AM News Update

As the sun rises on the morning after Memorial Day 2026, the mortgage industry is closely monitoring a subtle but notable shift in consumer behavior and pricing trends. Historically, the holiday weekend marks a transition point where the spring home-buying frenzy stabilizes into a more calculated summer market. This year, the focus remains on how affordability levels and inventory constraints interact within our primary markets, spanning from the bustling streets of Chicago to the growing suburbs of Florida and Georgia. For those engaged in real estate transactions, understanding these early morning indicators is essential for making informed moves throughout the week.

Explore the latest trends and data to see how current market conditions align with your personal or professional financial goals. Jump in as we break down the most recent developments in the lending landscape and what they imply for homeowners and investors alike.

Technical Definitions and Practical Applications

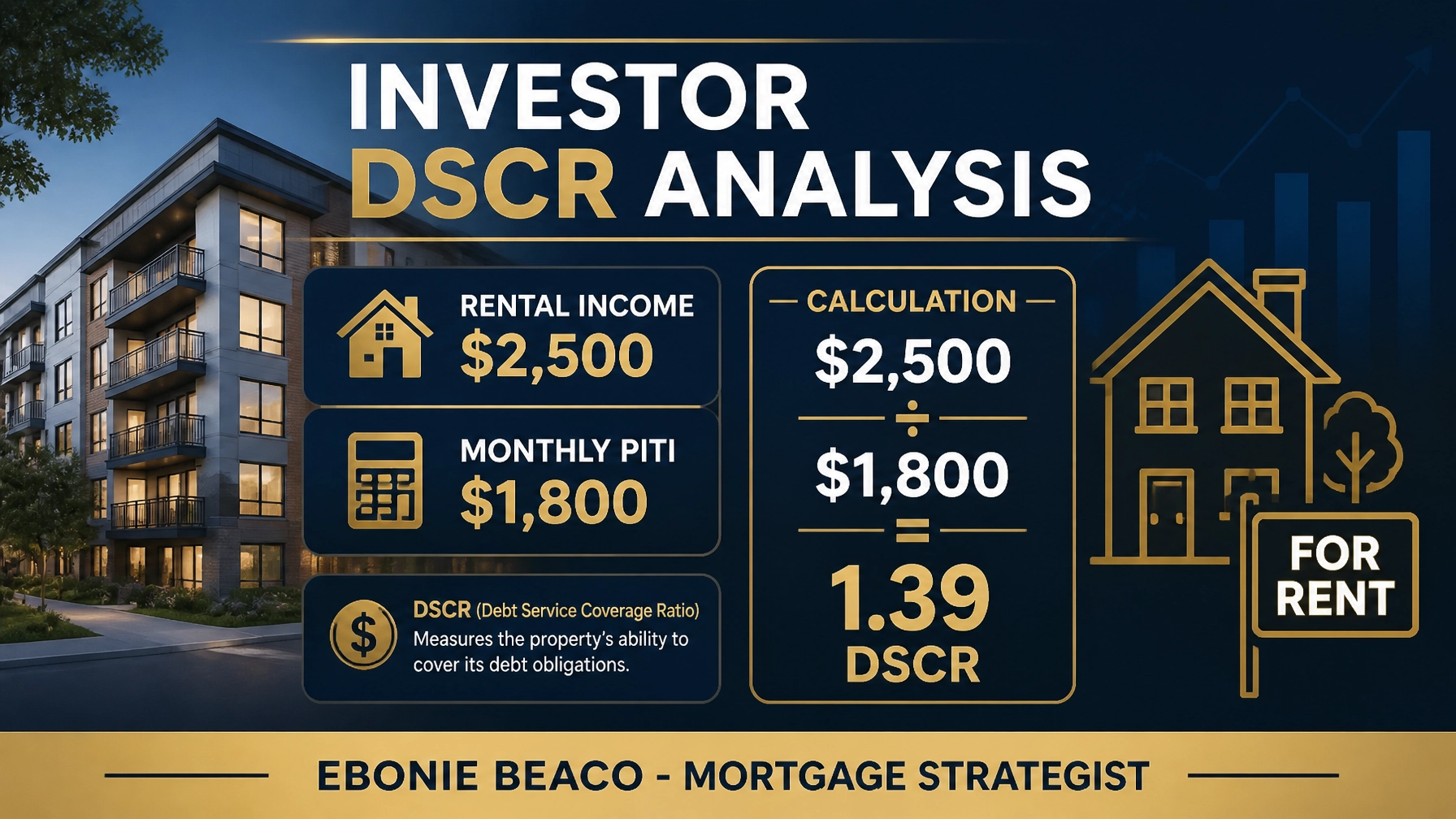

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to evaluate the ability of an investment property to cover its own debt obligations through its generated income.

Application: Investors use this to qualify for loans based on the property’s rental income rather than their personal tax returns or W-2 income.

HELOC (Home Equity Line of Credit): A revolving credit line that allows homeowners to borrow against the equity they have built in their primary residence.

Application: You can access funds as needed for home improvements, debt consolidation, or as a down payment for an additional investment property.

Cash-Out Refinance: A mortgage refinancing option where the new loan is for a larger amount than the existing mortgage, with the difference paid to the borrower in cash.

Application: This strategy is frequently used to extract large sums of liquidity for business expansion or to scale a real estate portfolio.

Non-QM (Non-Qualified Mortgage): A category of loans designed for borrowers who do not meet the traditional criteria of government-backed mortgage programs.

Application: This provides a path for self-employed individuals or foreign nationals to secure financing using alternative documentation such as bank statements.

Analyzing the Post-Holiday Equity Landscape

Homeowners in states like California and Virginia are finding themselves in a unique position this May. While the seasonal shift often brings a slight uptick in inventory, property values have remained resilient, providing a significant cushion of tappable equity. Accessing this equity through a structured financing plan can be a powerful tool for wealth preservation and growth. By leveraging a HELOC, you can secure a flexible source of capital that reacts to your specific needs without disturbing the favorable terms of your existing primary mortgage.

Consider a real-world scenario for a homeowner in a high-growth market. Imagine a property valued at $600,000 with an existing mortgage balance of $350,000. If the lender allows for an 85% Loan-to-Value (LTV) limit, the maximum total debt allowed would be $510,000. After subtracting the existing $350,000 mortgage, the homeowner successfully unlocks $160,000 in available funds. This liquidity can be used to fund renovations or even serve as a substantial down payment for a second property, effectively turning a primary residence into a wealth-building engine.

Strategies for Real Estate Portfolio Scaling

For real estate investors operating in competitive regions like Illinois and Indiana, the post-Memorial Day period is an ideal time to evaluate the performance of rental portfolios. The ability to acquire new assets without the burden of personal income verification is a hallmark of the DSCR Investor Loan. This program prioritizes the cash flow of the asset itself, which is particularly useful for Airbnb operators and long-term landlords looking to move quickly on new opportunities. Comparing current rental rates against projected mortgage payments allows for a clear view of potential cash-on-cash returns.

To understand how this functions, look at a standard deal analysis. Suppose you are eyeing a rental property that generates a monthly gross rent of $2,500. If the total monthly debt obligation, including Principal, Interest, Taxes, and Insurance (PITI), totals $1,800, the resulting DSCR is 1.39. Most lenders view a ratio above 1.20 as a strong indicator of a healthy investment. This high ratio not only simplifies the approval process but also demonstrates the property’s intrinsic value as a self-sustaining asset within your portfolio.

Regional Market Activity and Opportunities

In the southeastern markets of Alabama and Georgia, we are observing a steady flow of "fix and flip" activity. Investors in these areas often utilize bridge loans or hard money options to close quickly on distressed properties before transitioning into long-term financing. The efficiency of these short-term solutions is critical in markets where inventory is snatched up within days of listing. Home Loans Network remains committed to providing the guidance necessary to navigate these fast-paced environments with confidence.

A typical fix-and-flip calculation helps visualize the potential. An investor might purchase a property for $200,000 and allocate $50,000 for high-quality renovations. If the After Repair Value (ARV) is conservatively estimated at $350,000, the projected profit before carrying costs stands at $100,000. Utilizing a tailored fix and flip loan allows the investor to preserve their own capital while the project is underway. This strategic use of leverage is how modern investors scale from single projects to multiple simultaneous developments.

Navigating the Summer Market with Expert Guidance

As we move deeper into 2026, the importance of a clear mortgage strategy cannot be overstated. Whether you are a first-time homebuyer in Michigan or an experienced investor managing units in Missouri and Kentucky, the lending environment requires a proactive approach. Understanding how to align your financing with your long-term wealth goals is the difference between a simple transaction and a strategic investment. We encourage you to review your current equity position and explore how different loan programs can be integrated into your financial roadmap.

The housing market continues to evolve, but the fundamentals of smart financing remain constant. By focusing on education and transparency, you can navigate interest rate shifts and inventory challenges with a sense of control. Our team is here to help you compare options, analyze scenarios, and execute on the strategies that best serve your unique profile. Access the resources and expertise needed to turn today’s market headlines into tomorrow’s financial milestones.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664