Investing with Less: Low Down Payment Strategies for Real Estate

Many people assume that stepping into the world of real estate requires a massive mountain of savings. The "20% down payment" rule has been repeated so often that it feels like a law. For a $400,000 home, that would mean coming up with $80,000 before you even step foot in the door. For most aspiring investors or first-time buyers in markets like Chicago, Atlanta, or Virginia Beach, that figure feels out of reach.

The reality is quite different. You do not need a fortune to start building a real estate portfolio. By understanding modern mortgage basics, you can leverage low down payment strategies to acquire property, build equity, and generate rental income much sooner than you think.

Whether you are looking for your first home in Michigan or trying to scale a rental portfolio in Florida, low-barrier entry points exist.

The Low Down Payment Entry: FHA and Conventional 3%

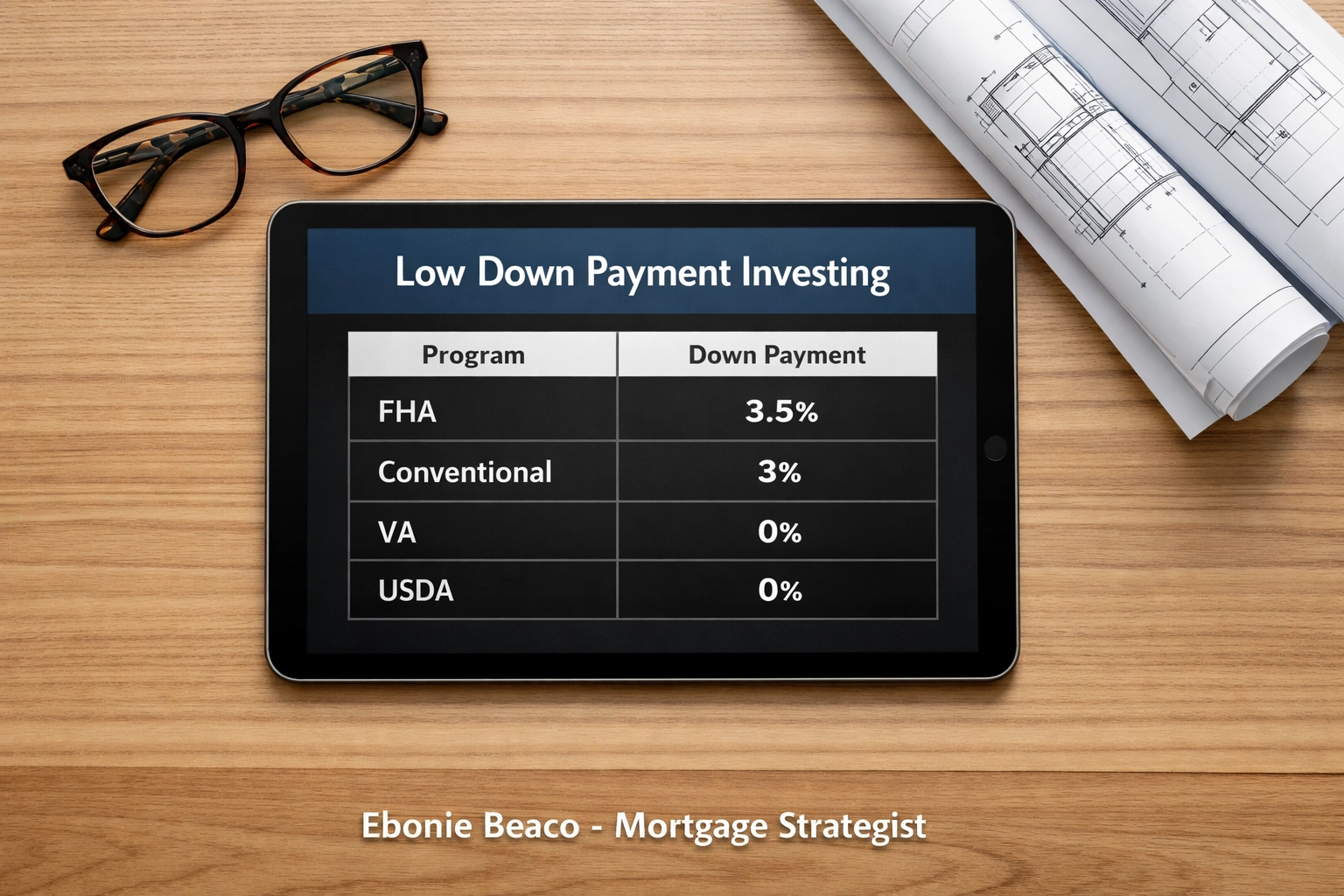

The most accessible path for many is the FHA Loan. Backed by the Federal Housing Administration, these loans are designed to help people become homeowners with as little as 3.5% down. This program is popular because it has flexible credit requirements and allows for higher debt-to-income (DTI) ratios.

If you have a stronger credit profile, you might qualify for a Conventional 97 loan. This allows for a down payment of just 3%. While these are primarily for primary residences, they serve as the ultimate "launchpad" for new investors.

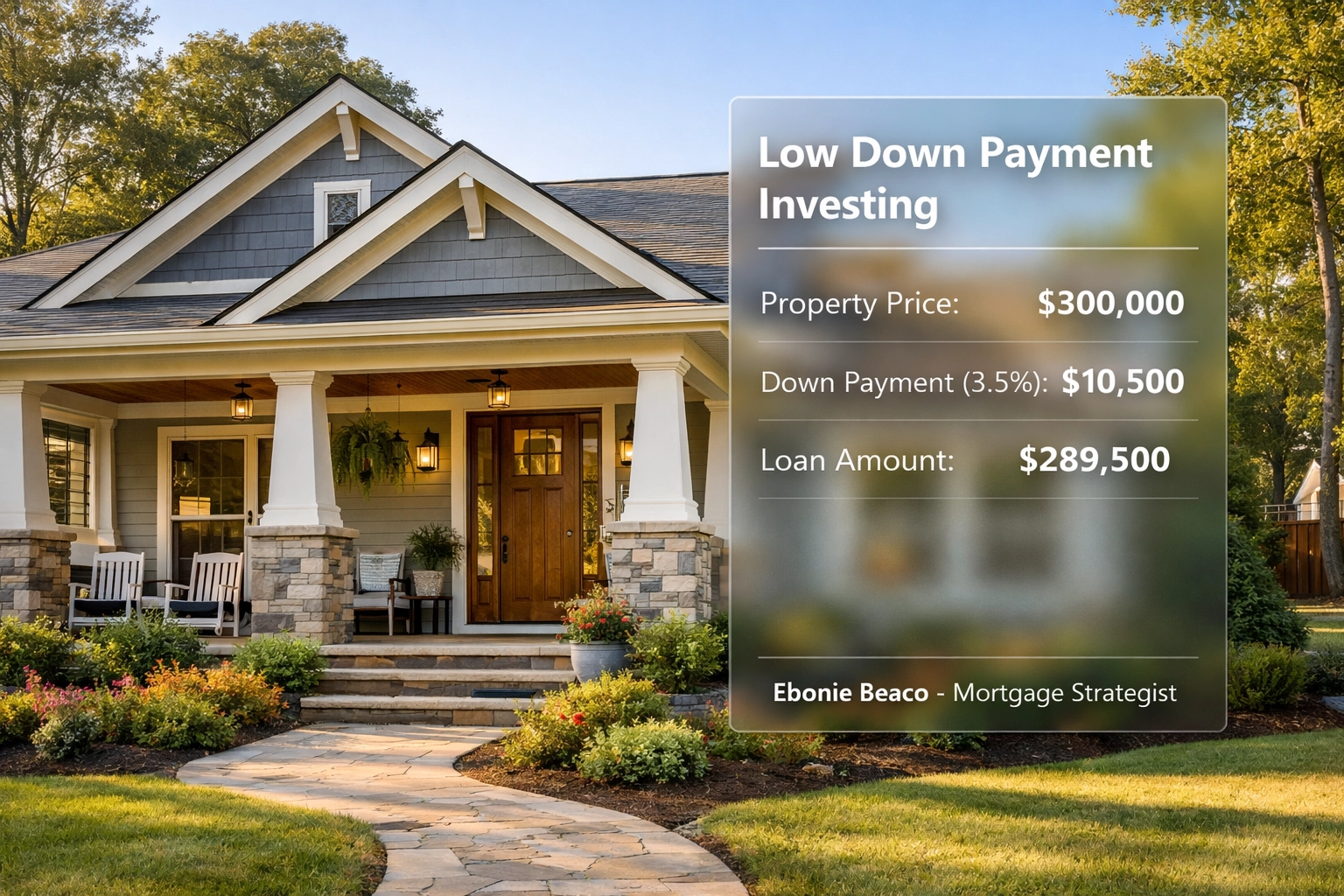

Let’s look at the math on a typical entry-level property:

Suppose you find a solid property in an area like Indianapolis or Little Rock priced at $300,000.

- Property Price: $300,000

- Down Payment (3.5%): $10,500

- Loan Amount: $289,500

By coming up with just $10,500, you control a $300,000 asset. This is the power of leverage. If the property appreciates by just 3% in a year, you have gained $9,000 in equity: nearly a 90% return on your initial $10,500 investment.

Image Description: A professional financial breakdown graphic. Title: "Low Down Payment Investing". At the bottom: "Ebonie Beaco - Mortgage Loan Officer". The graphic shows: Property Price: $300,000 | Down Payment (3.5%): $10,500 | Loan Amount: $289,500. No money or cash symbols used.

Image Description: A professional financial breakdown graphic. Title: "Low Down Payment Investing". At the bottom: "Ebonie Beaco - Mortgage Loan Officer". The graphic shows: Property Price: $300,000 | Down Payment (3.5%): $10,500 | Loan Amount: $289,500. No money or cash symbols used.

House Hacking: The Ultimate Investor Shortcut

House hacking is a strategy where you purchase a multi-unit property (up to 4 units), live in one unit, and rent out the others. In the eyes of a lender, this is still a primary residence purchase, which means you can use those low down payment programs.

Imagine buying a triplex in a growing neighborhood in Georgia or Virginia. You live in Unit A. Units B and C are occupied by tenants whose rent covers the majority (or all) of your mortgage payment.

- FHA Multi-Unit: You can buy a 2-4 unit property with only 3.5% down.

- VA Multi-Unit: Eligible veterans can buy a 2-4 unit property with 0% down.

This strategy allows you to learn the ropes of being a landlord while significantly reducing your living expenses. It is one of the fastest ways to build a portfolio because, after living there for a year, you can often move out, turn your unit into a rental, and use a new low down payment loan to buy your next property. You can explore more about this through our home purchase resources.

VA and USDA: The Zero-Down Advantage

For those who qualify, zero-down payment options are the gold standard of real estate entry.

VA Loans are available to active-duty service members, veterans, and surviving spouses. There is no down payment required, and there is no monthly private mortgage insurance (PMI). In military-heavy markets like those in Virginia or California, the VA loan is a massive competitive advantage for building long-term wealth.

USDA Loans target rural and suburban areas. If you are looking at properties on the outskirts of major hubs in Arkansas or Kentucky, you might find homes that qualify for 100% financing. These loans are designed to encourage homeownership in less dense areas and offer very competitive interest rates.

Leveraging Your Current Equity

If you already own a home, you might be sitting on a "hidden" down payment for your next investment. As home values have climbed in states like California and Florida, many homeowners have significant equity that isn't doing anything for them.

You can access this through a HELOC (Home Equity Line of Credit) or a Cash-Out Refinance.

- HELOC: This works like a credit card tied to your home's equity. You only pay interest on what you use. You can use the HELOC funds to cover the down payment on a rental property in a high-demand area.

- Cash-Out Refinance: You replace your current mortgage with a new, larger loan and take the difference in cash. This is a common strategy for investors looking to execute the "Refinance" step of the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat).

Check out our home refinance page to see how these numbers might work for your specific situation.

Image Description: A clean, structured flowchart showing the process of moving from "Current Home Equity" to "New Investment Property". Title: "Low Down Payment Investing". At the bottom: "Ebonie Beaco - Mortgage Loan Officer". No money or cash depicted.

Image Description: A clean, structured flowchart showing the process of moving from "Current Home Equity" to "New Investment Property". Title: "Low Down Payment Investing". At the bottom: "Ebonie Beaco - Mortgage Loan Officer". No money or cash depicted.

The Trade-Off: Private Mortgage Insurance (PMI)

When you put down less than 20%, lenders usually require Private Mortgage Insurance (PMI). It is important to be transparent about this: PMI is an extra monthly cost. However, for most investors, the cost of PMI is a small price to pay for the ability to enter the market years earlier than they otherwise could.

In many cases, as the property appreciates or you pay down the balance, you can request to remove PMI once you reach 20% equity. This effectively gives you a "raise" in your monthly cash flow once that requirement is met.

Strategies for Closing Costs

A down payment isn't the only upfront cost. You also have closing costs, which typically range from 2% to 5% of the loan amount. If you are short on funds, you can utilize Seller Concessions.

In a balanced or buyer-friendly market, you can negotiate for the seller to pay a portion of your closing costs. This means you only need to bring your 3% or 3.5% down payment to the table, making the entry even more affordable.

Why This Works in Today's Market

Market conditions in places like Chicago or the suburbs of Michigan are constantly shifting. Waiting to save 20% often means watching home prices rise faster than you can save. By using a low down payment strategy, you lock in today’s price and start benefiting from appreciation and principal reduction immediately.

For landlords and investors, these residential-style loans are the foundation. Once you have built equity through these programs, you can eventually transition into more advanced options like DSCR investor loans, which qualify you based on the property’s income rather than your personal debt-to-income ratio.

Next Steps for Your Investment Journey

Starting with a low down payment is about getting your foot in the door. It is about moving from the sidelines into the game. Whether you are looking at a fixer-upper in Alabama or a turnkey condo in Florida, the strategy remains the same: use the minimum amount of capital necessary to control the maximum amount of real estate.

If you have questions about which program fits your credit profile or the specific market you are targeting, we are here to help. You can contact us or look through our testimonials to see how others have successfully navigated these waters.

Image Description: A professional comparison table listing FHA (3.5%), Conventional (3%), VA (0%), and USDA (0%). Title: "Low Down Payment Investing". At the bottom: "Ebonie Beaco - Mortgage Loan Officer". No money or cash shown.

Image Description: A professional comparison table listing FHA (3.5%), Conventional (3%), VA (0%), and USDA (0%). Title: "Low Down Payment Investing". At the bottom: "Ebonie Beaco - Mortgage Loan Officer". No money or cash shown.

Don't have a huge down payment? Contact Ebonie Beaco for low down payment mortgage options.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664