Investing in Real Estate with a Low Credit Score

If you have spent any time in the real estate world, you have likely heard the common myth that you need a perfect credit score to buy an investment property. Many aspiring landlords or house flippers in places like Chicago, Florida, or California stop before they even start because they believe their financial past disqualifies them from a successful future.

The truth is much more transparent. While a high credit score certainly opens doors to lower interest rates and conventional financing, a lower score is not a dead end. Real estate investing is a diverse field with dozens of financing pathways tailored to different profiles.

Explore the strategies used by savvy investors to acquire property even when their FICO score is less than ideal. This guide breaks down how you can leverage alternative loan programs and creative structures to build your portfolio today.

Understanding the Landscape of Credit in Real Estate

Before diving into specific loan programs, it is helpful to define what "low credit" actually means in the eyes of a mortgage strategist. Most conventional lenders look for a score of 620 or higher. If your score falls between 500 and 600, you are entering the territory where traditional banks often say "no," but specialized investment lenders start getting creative.

Credit Score (FICO): A three-digit number that represents your creditworthiness based on your credit history. Application: In real estate, this number influences the down payment requirement and the interest rate offered by the lender.

Many investors find themselves with lower scores due to past medical bills, high credit card utilization, or even simple errors on their credit reports. At Home Loans Network, we focus on the potential of the deal and the strategy of the borrower rather than just a single number on a screen.

Leveraging DSCR Loans for Rental Properties

One of the most powerful tools for an investor with a lower credit score is the Debt Service Coverage Ratio (DSCR) loan. These are categorized as Non-QM Mortgage Loans, meaning they do not follow the strict rules of government-sponsored entities like Fannie Mae or Freddie Mac.

DSCR Loan: A financing option where eligibility is based on the cash flow of the property rather than the personal income of the borrower. Application: If the rental income of a property in a market like Atlanta or Virginia Beach covers the monthly mortgage payment, the lender is much more likely to approve the deal, even if the borrower's credit score is in the 600s.

Because DSCR lenders prioritize the property’s performance, they are often more flexible with credit requirements. You may be required to bring a larger down payment (typically 20% to 25%), but you can bypass the grueling debt-to-income (DTI) checks that sink many traditional applications.

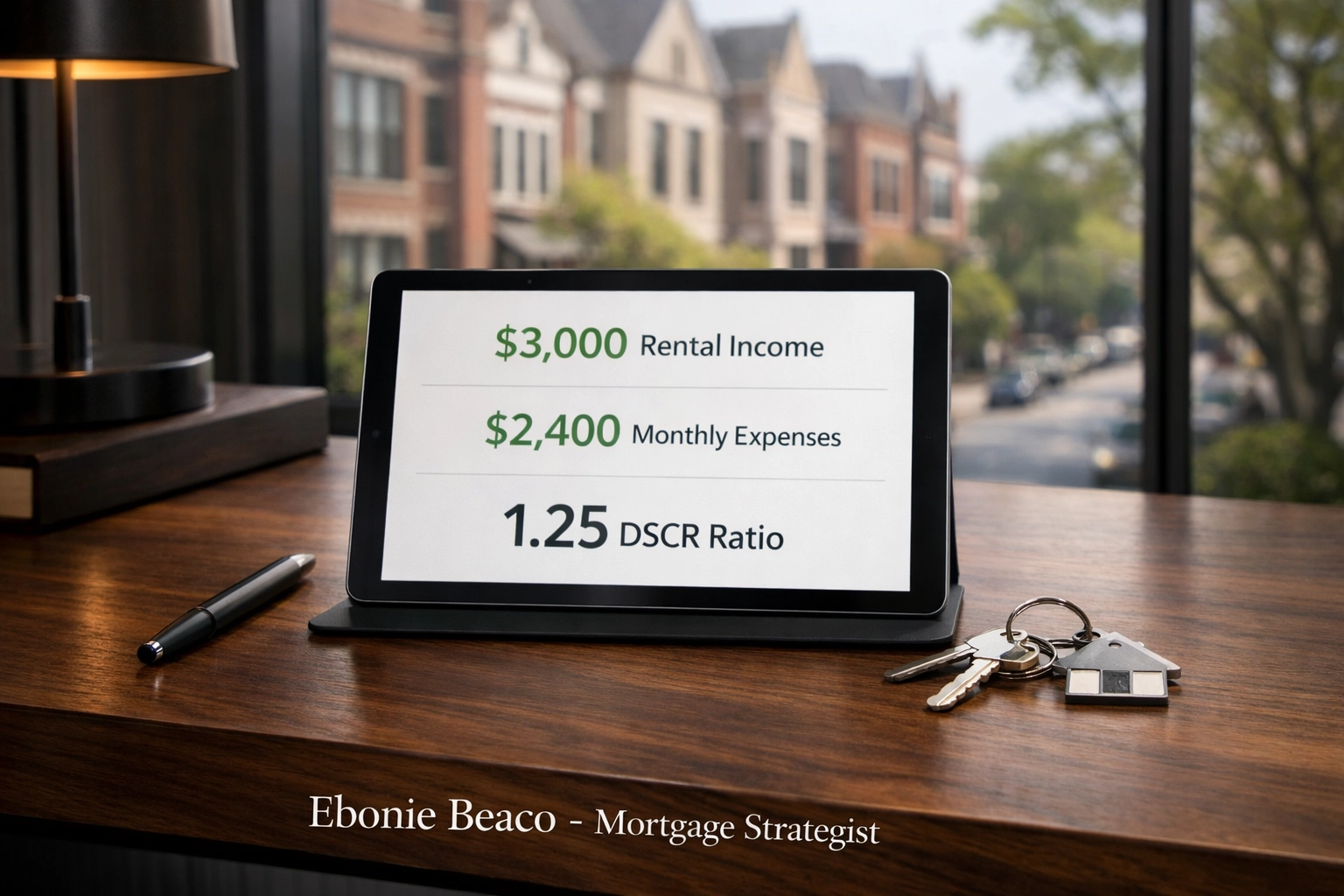

DSCR Calculation Example

Imagine you are looking at a duplex in Michigan. To see if it qualifies for a DSCR loan, you need to look at the numbers.

- Monthly Rental Income: $3,000

- Monthly Principal, Interest, Taxes, Insurance, and HOA (PITI): $2,400

- Calculation: $3,000 / $2,400 = 1.25 DSCR

A ratio of 1.25 is generally considered strong by most lenders. Even with a lower credit score, showing a deal with this level of coverage makes you a much more attractive borrower.

Visual: DSCR Calculation Breakdowns - Rental Income: $3,000 | PITI: $2,400 | DSCR Ratio: 1.25 | Property Value: $350,000 | Loan Amount: $262,500.

Visual: DSCR Calculation Breakdowns - Rental Income: $3,000 | PITI: $2,400 | DSCR Ratio: 1.25 | Property Value: $350,000 | Loan Amount: $262,500.

Hard Money and Bridge Loans for Quick Turnarounds

If your goal is to buy a distressed property, fix it up, and sell it (the classic fix and flip), credit scores become even less significant. Hard Money Loans are the primary vehicle for this strategy.

Hard Money Loan: A short-term, asset-based loan secured by real estate. Application: These lenders care primarily about the After Repair Value (ARV) of the home. If you find a great deal in a hot market like Tampa or Birmingham, the hard money lender provides the funds based on the property’s equity.

Hard money is expensive. You will pay higher interest rates and points upfront. However, these loans are designed to be paid off quickly. They provide the "bridge" you need to acquire the property and renovate it. Once the home is renovated and its value has increased, you can sell it or move into a long-term Landlord Loan once your credit score has had time to recover.

Explore more about these options on our mortgage basics page.

House Hacking with Government-Backed Loans

If you are a first-time investor, you might consider "house hacking." This involves buying a multi-unit property (up to four units), living in one unit, and renting out the others.

FHA Loan: A mortgage insured by the Federal Housing Administration that allows for down payments as low as 3.5%. VA Loan: A zero-down payment mortgage option available to veterans and active-duty service members.

Both FHA and VA loans have much more lenient credit score requirements than conventional loans. In many cases, you can qualify with a score as low as 580. By using these programs, you are not just buying a home; you are acquiring an income-producing asset. The rental income from the other units can often cover your entire mortgage payment, allowing you to build equity for free.

Compare your potential savings and payments using our mortgage calculators.

Creative Investment Strategies

When traditional financing feels out of reach, successful investors turn to creative deal-making. These strategies rely on your ability to find deals and build relationships rather than your credit report.

1. Seller Financing

In a seller financing arrangement, the person selling the home acts as the bank. You make monthly payments directly to them. Because there is no traditional bank involved, your credit score is only as important as the seller wants it to be. This is a common strategy in markets with older owners who want a steady stream of income without the headaches of property management.

2. Real Estate Partnerships

If you have a talent for finding deeply discounted properties but your credit is holding you back, find a partner. You provide the "sweat equity" (finding the deal, managing the renovation, finding tenants), and they provide the "financial equity" (the credit score and down payment).

3. Real Estate Wholesaling

Wholesaling is a way to get into the real estate game with zero credit and almost no money. You find a great deal, get it under contract, and then sell that contract to another investor for a "wholesale fee." It is a fast-paced way to build up the cash reserves needed for your own future down payments while learning the market inside and out.

Visual: Real Estate Partnership Structure - Partner A (Sweat Equity): Sourcing, Management, Reno | Partner B (Financial Equity): Credit Score, Down Payment | Result: 50/50 Profit Split.

Visual: Real Estate Partnership Structure - Partner A (Sweat Equity): Sourcing, Management, Reno | Partner B (Financial Equity): Credit Score, Down Payment | Result: 50/50 Profit Split.

Strategic Steps to Improve Your Credit While Investing

While you can invest with low credit, your long-term goal should always be to improve your score to access better rates. Lower interest rates mean higher monthly cash flow.

- Review Your Reports: Look for errors. Removing one incorrect late payment can jump your score significantly.

- Lower Credit Utilization: Try to keep your credit card balances below 30% of their limits.

- Consistent Payments: Set up autopay for everything. One late payment can set your progress back by months.

- Access Mentoring: Sometimes you just need a roadmap. Connecting with a professional can help you prioritize which debts to pay down first to see the fastest score increase.

Check out our FAQ page for more answers to common credit and lending questions.

Financing Scenarios in Different Markets

The strategy you choose often depends on where you are buying.

- Chicago, IL: With a robust inventory of 2-4 unit buildings, house hacking with an FHA loan is a popular way to enter the market.

- Florida Cities: The high demand for short-term rentals (Airbnb) makes DSCR loans a favorite for investors looking to buy near the coast.

- California: Given the high property values, many investors use Bridge Loans to secure properties quickly before refinancing into long-term debt once the property value has appreciated.

Conclusion

Investing in real estate with a low credit score is entirely possible if you are willing to look beyond traditional bank products. Whether you utilize the income-based qualification of a DSCR loan, the asset-based approach of hard money, or the low-down-payment benefits of government-backed loans, there is a path forward.

Do not let a number on a piece of paper stop you from building wealth. The significance of your strategy far outweighs the significance of a temporary credit dip.

Jump in and explore your options today.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664